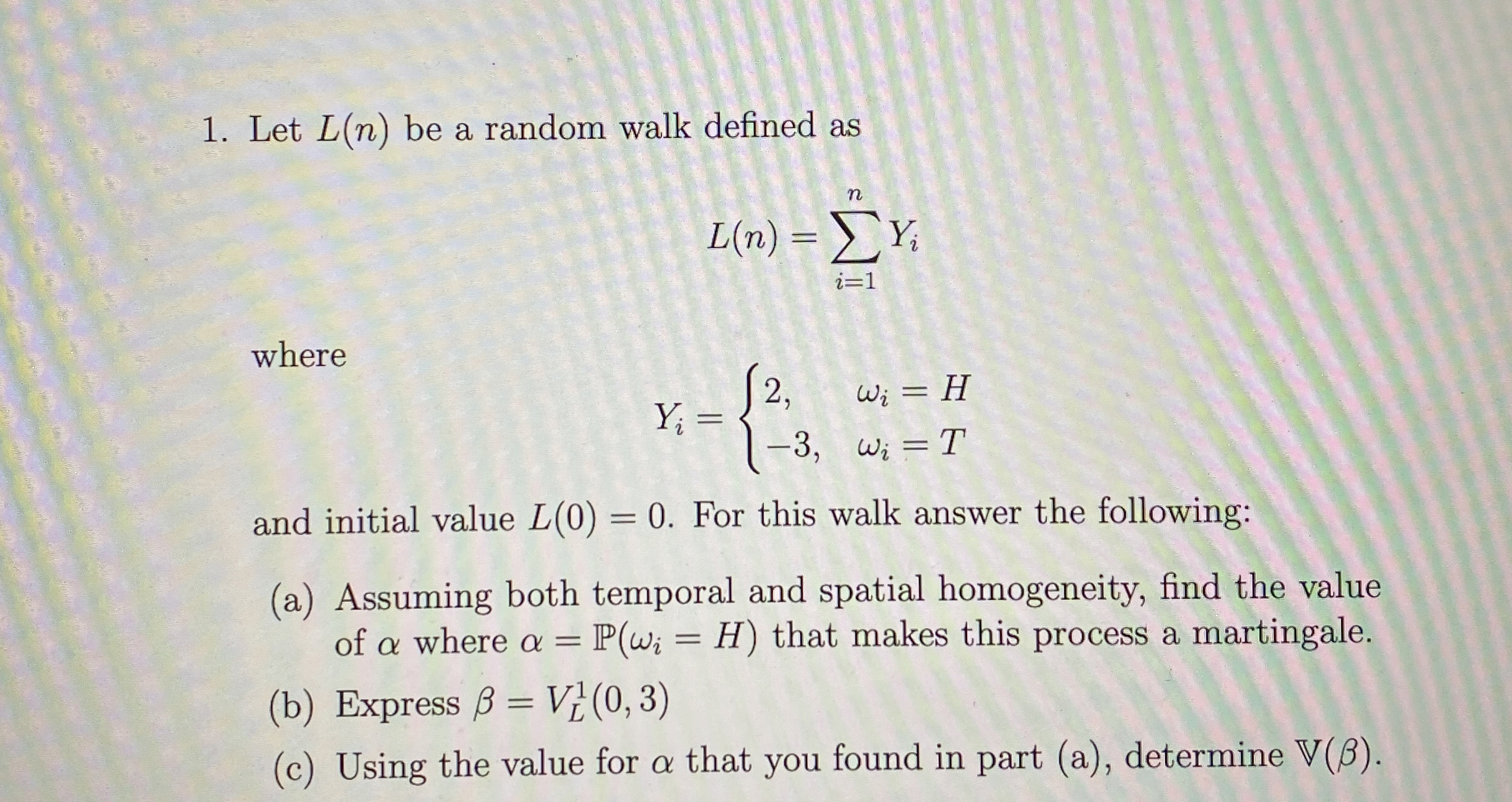

Question: Let L ( n ) be a random walk defined as L ( n ) = i = 1 n Y i where Y i

Let be a random walk defined as

where

and initial value For this walk answer the following:

a Assuming both temporal and spatial homogeneity, find the value of where that makes this process a martingale.

b Express

c Using the value for that you found in part a determine

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock