Question: Let R, and Rg be random variables representing the annual returns for Stock A and Stock B. You are given the following information: 04 =

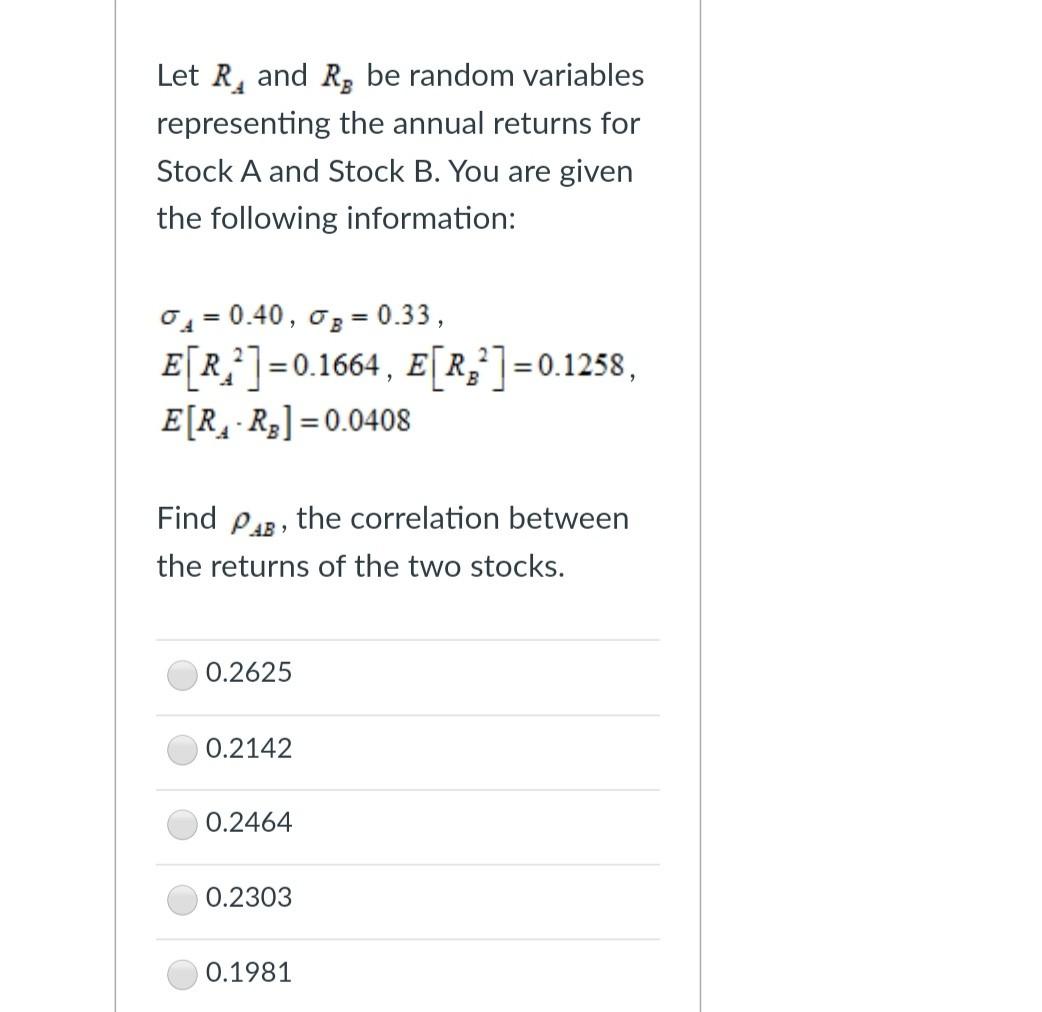

Let R, and Rg be random variables representing the annual returns for Stock A and Stock B. You are given the following information: 04 = 0.40, 08 = 0.33, E[R,?] = 0.1664, E[R,?] = 0.1258, E[R, Ry] =0.0408 Find Pag, the correlation between the returns of the two stocks. 0.2625 0.2142 0.2464 0.2303 0.1981

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock