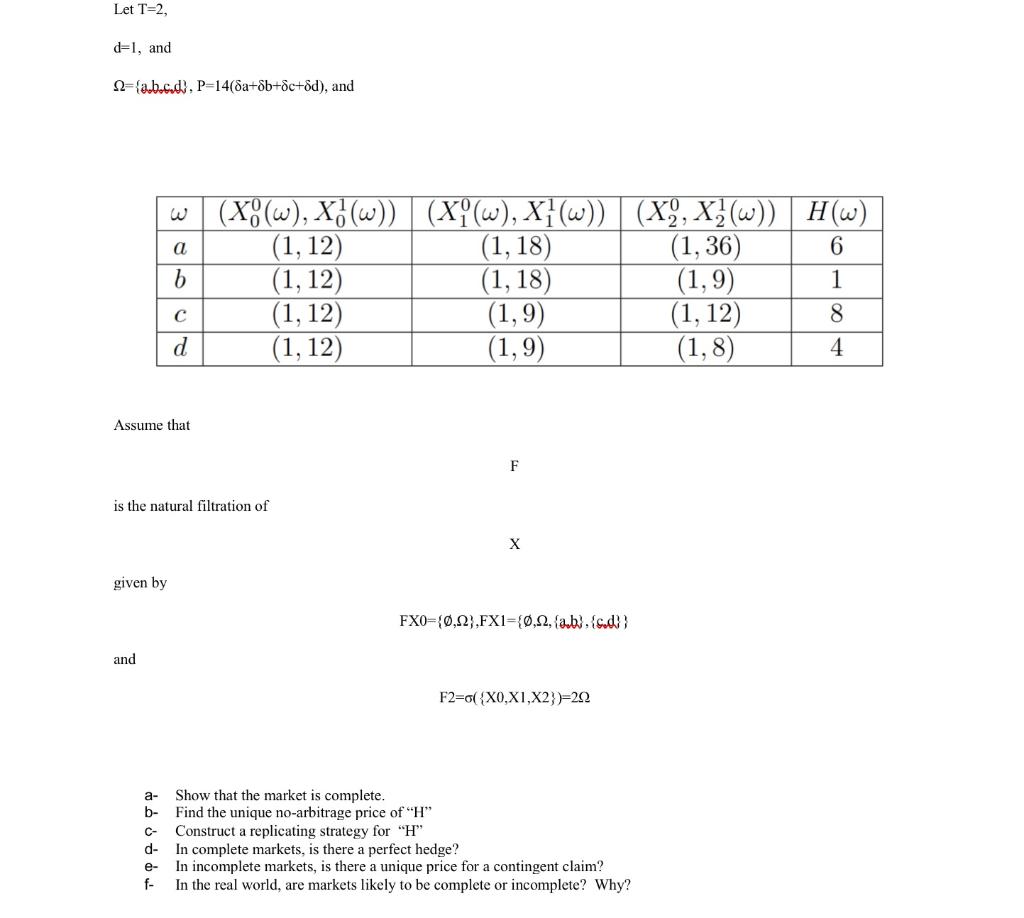

Question: Let T-2, d=1, and 12={abc.d), P=14(da+8b+c+8d), and w a b (X:(w), X7(W)) (X?(w), X](w)) (1,12) (1,18) (1, 12) (1,18) (1, 12) (1,9) (1,12) (1,9) (X9,

Let T-2, d=1, and 12={abc.d), P=14(da+8b+c+8d), and w a b (X:(w), X7(W)) (X?(w), X](w)) (1,12) (1,18) (1, 12) (1,18) (1, 12) (1,9) (1,12) (1,9) (X9, X](w)) H(W) (1,36) 6 (1,9) 1 (1, 12) 8 (1,8) 4 d Assume that F is the natural filtration of X given by FX0={0,22).FX1={0.12. (a.b), (s.d!! and F2=of {X0,XI,X2})=20 a- b- 6 Show that the market is complete. Find the unique no-arbitrage price of "H" Construct a replicating strategy for "H" d- In complete markets, is there a perfect hedge? e- In incomplete markets, is there a unique price for a contingent claim? f- In the real world, are markets likely to be complete or incomplete? Why? Let T-2, d=1, and 12={abc.d), P=14(da+8b+c+8d), and w a b (X:(w), X7(W)) (X?(w), X](w)) (1,12) (1,18) (1, 12) (1,18) (1, 12) (1,9) (1,12) (1,9) (X9, X](w)) H(W) (1,36) 6 (1,9) 1 (1, 12) 8 (1,8) 4 d Assume that F is the natural filtration of X given by FX0={0,22).FX1={0.12. (a.b), (s.d!! and F2=of {X0,XI,X2})=20 a- b- 6 Show that the market is complete. Find the unique no-arbitrage price of "H" Construct a replicating strategy for "H" d- In complete markets, is there a perfect hedge? e- In incomplete markets, is there a unique price for a contingent claim? f- In the real world, are markets likely to be complete or incomplete? Why

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts