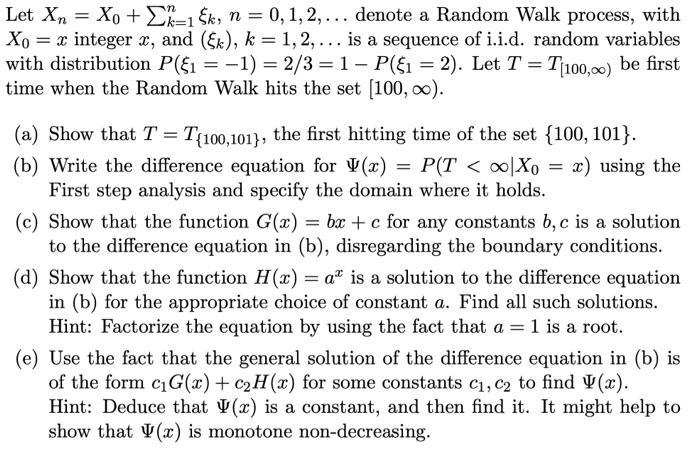

Question: Let Xn=X0+k=1nk,n=0,1,2, denote a Random Walk process, with X0=x integer x, and (k),k=1,2, is a sequence of i.i.d. random variables with distribution P(1=1)=2/3=1P(1=2). Let T=T[100,)

Let Xn=X0+k=1nk,n=0,1,2, denote a Random Walk process, with X0=x integer x, and (k),k=1,2, is a sequence of i.i.d. random variables with distribution P(1=1)=2/3=1P(1=2). Let T=T[100,) be first time when the Random Walk hits the set [100,). (a) Show that T=T{100,101}, the first hitting time of the set {100,101}. (b) Write the difference equation for (x)=P(T

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock