Question: Let Xt be a moving average process of order q (a) [10 marks] Let {Xi} be a moving average process of order q (MA(q)), let

Let Xt be a moving average process of order q

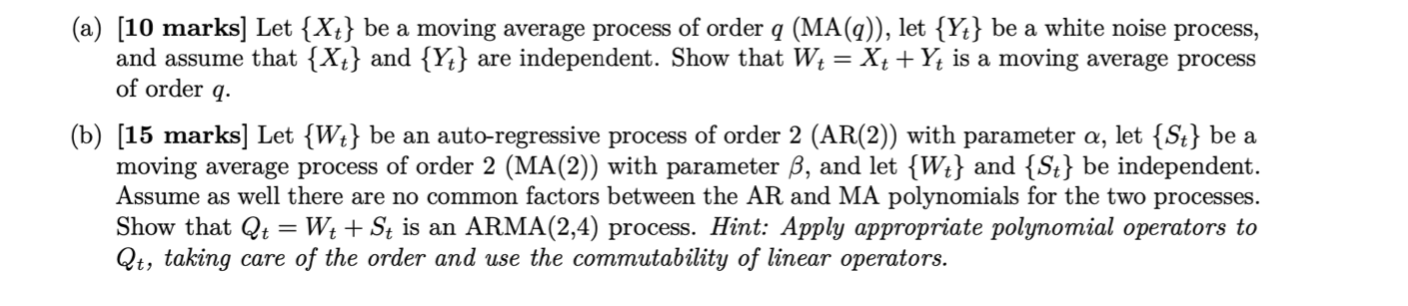

(a) [10 marks] Let {Xi} be a moving average process of order q (MA(q)), let {E} be a white noise process, and assume that {Xt} and {Yd are independent. Show that W, = X: + Y; is a moving average process of order q. (b) [15 marks] Let {Wt} be an auto-regressive process of order 2 (ARQD with parameter a, let {3;} be a moving average process of order 2 (MA(2)) with parameter , and let {Wt} and {3;} be independent. Assume as well there are no common factors between the AR and MA polynomials for the two processes. Show that Q; = W: + S; is an ARMA(2,4) process. Hint: Apply appropriate polynomial operators to Qt, taking care of the order and use the commutabity of linear operators

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts