Question: Let's assume the provided data (in %) applies to two efficient portfolios. To illustrate the efficient frontier, we'll use three sets of coordinates denoted

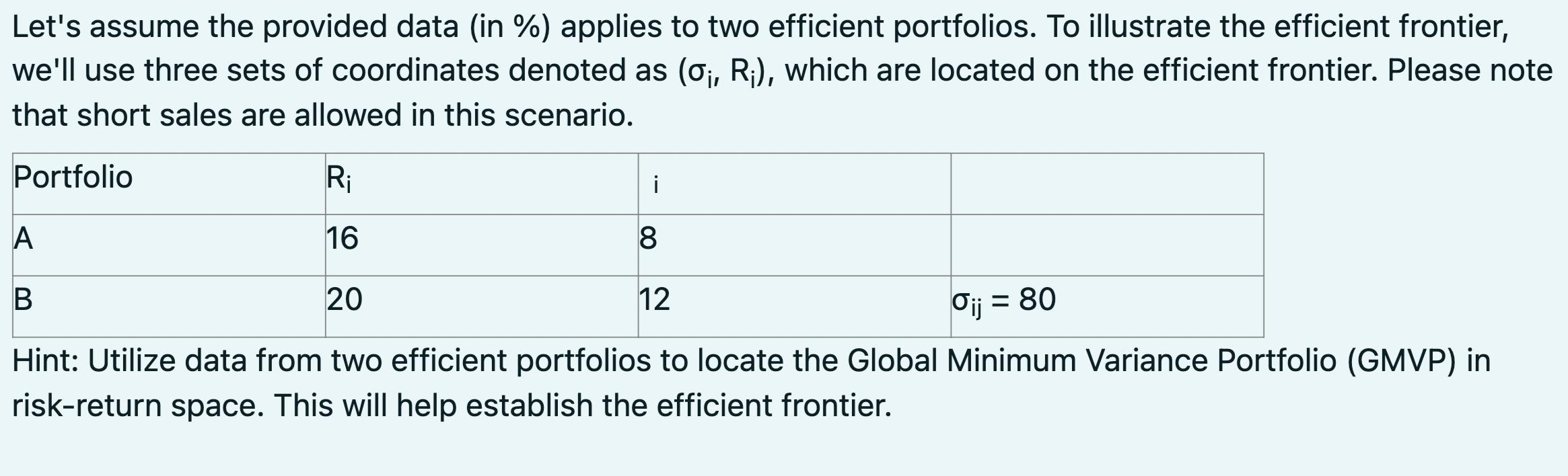

Let's assume the provided data (in %) applies to two efficient portfolios. To illustrate the efficient frontier, we'll use three sets of coordinates denoted as (0, R), which are located on the efficient frontier. Please note that short sales are allowed in this scenario. Portfolio R 16 20 Oij = 80 Hint: Utilize data from two efficient portfolios to locate the Global Minimum Variance Portfolio (GMVP) in risk-return space. This will help establish the efficient frontier. A B i 8 12

Step by Step Solution

3.47 Rating (157 Votes )

There are 3 Steps involved in it

To locate the Global Minimum Variance Portfolio GMVP and establish the efficient frontier we can uti... View full answer

Get step-by-step solutions from verified subject matter experts