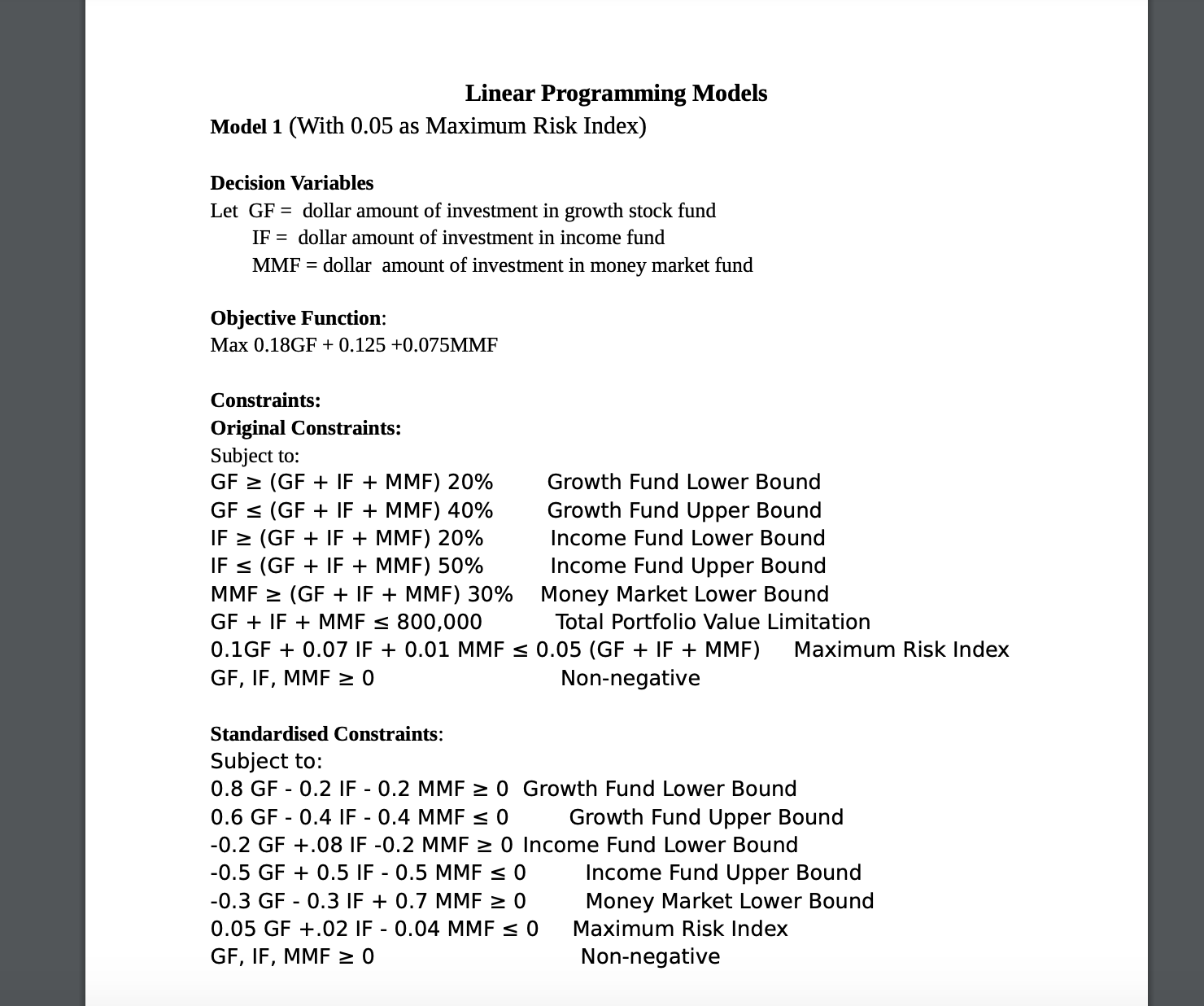

Question: Linear Programming Models Model 1 (With 0.05 as Maximum Risk Index) Decision Variables Let GF = dollar amount of investment in growth stock fund IF

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock