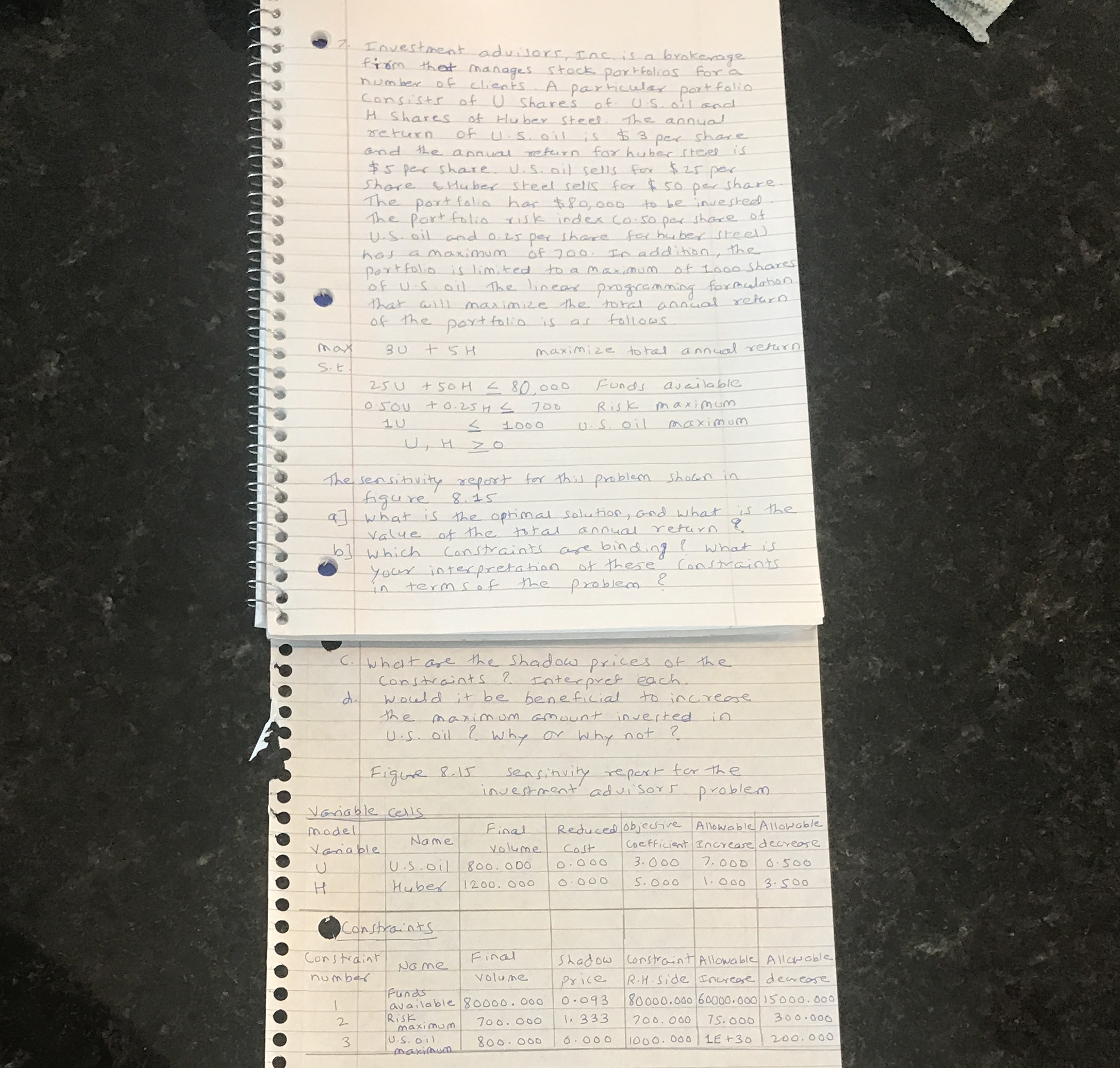

Question: Linear programming : sensitivity analysis and interpretation of solution ( please answer the question a,b,c,d using figure 8.15, please draw graph wherever needed, thank you.

Linear programming : sensitivity analysis and interpretation of solution ( please answer the question a,b,c,d using figure 8.15, please draw graph wherever needed, thank you.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock