Question: List two major characteristics that are useful in predicting the likelihood of fraudulent financial reporting in an audit For each of the characteristics, state two

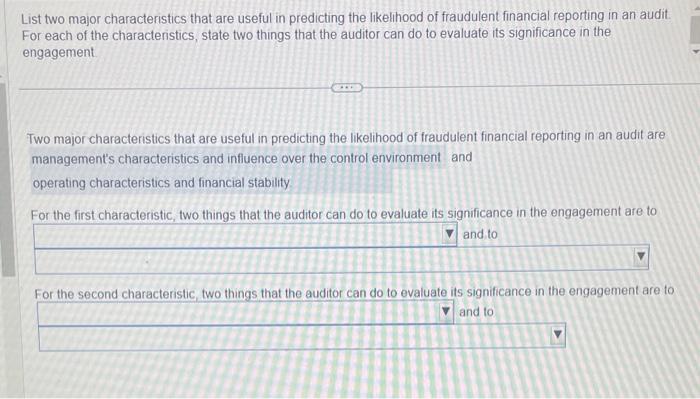

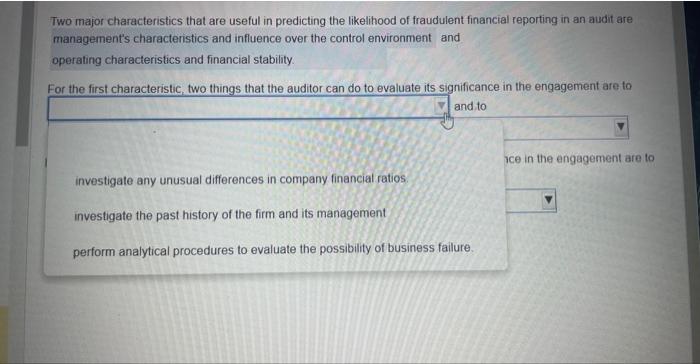

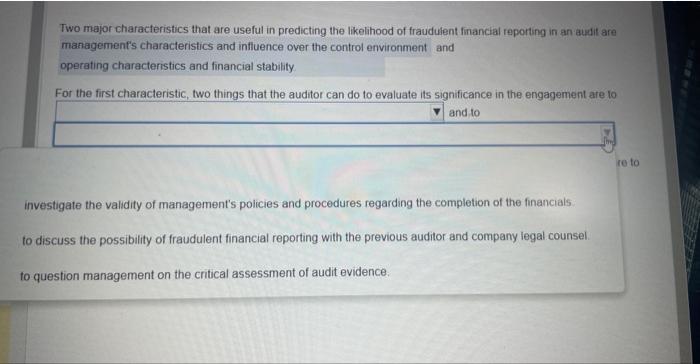

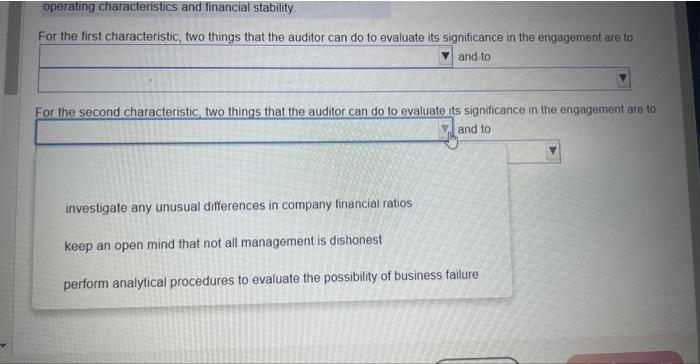

List two major characteristics that are useful in predicting the likelihood of fraudulent financial reporting in an audit For each of the characteristics, state two things that the auditor can do to evaluate its significance in the engagement. Two major characteristics that are useful in predicting the likelihood of fraudulent financial reporting in an audit are management's characteristics and influence over the control environment and operating characteristics and financial stability. For the first characteristic. two things that the auditor can do to evaluate its significance in the engagement are to and to For the second characteristic. two things that the auditor can do to evaluate its significance in the engagement are to nd to Two major characteristics that are useful in predicting the likelihood of fraudulent financial reporting in an audit are management's characteristics and influence over the control environment and operating characteristics and financial stability. Eor the first characteristic. two thinas that the auditor can do to evaluate its significance in the engagement are to Two major characferistics that are useful in predicting the likelihood of fraudulent financial reporting in an audit are managemenf's characteristics and influence over the control environment and operating characteristics and financial stability For the first characteristic. two things that the auditor can do to evaluate its significance in the engagement are io and to investigate the validity of management's policies and procedures regarding the completion of the financials to discuss the possibility of fraudulent financial reporting with the previous auditor and company legal counsel. to question management on the critical assessment of audit evidence. For the first characteristic. two things that the auditor can do to evaluate its significance in the engagement are to and to For the first characteristic two thinas that the auditor can do to evaluate its significance in the engagement are to and to For the second characteristic. two thinas that the auditor can do to evaluate its significance in the engagement are and 10 consider the impact of specific risks that are identified in the AlCPA's "Industry Audit Risk Alert". investigate the past history of the firm and its management retention. investigate whether material transactions occur close to year-end

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts