Logistical Logistics Inc. (Logistical Logistics or the Company) provides transportation and logistics services to customers throughout...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

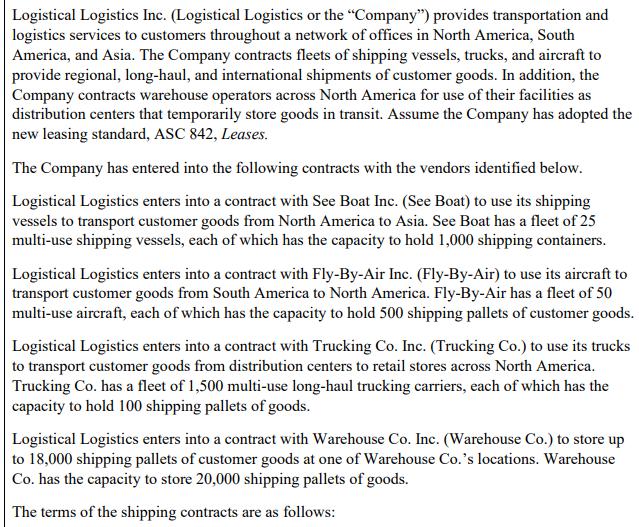

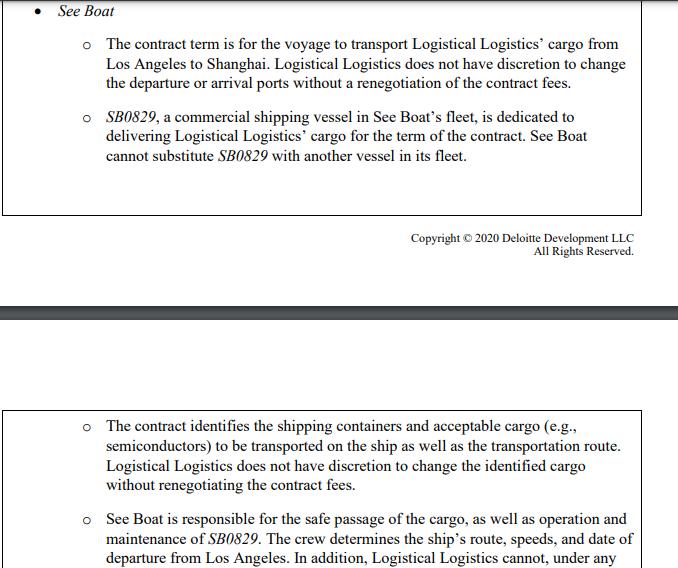

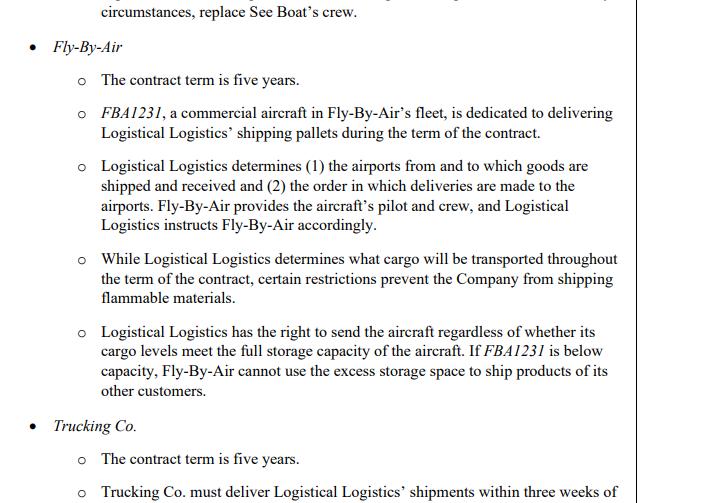

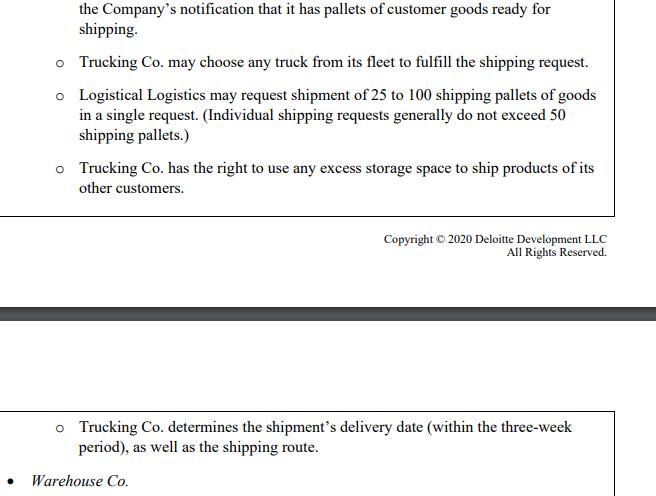

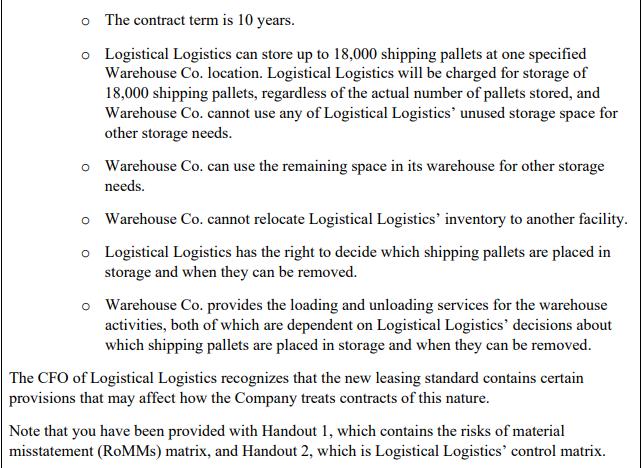

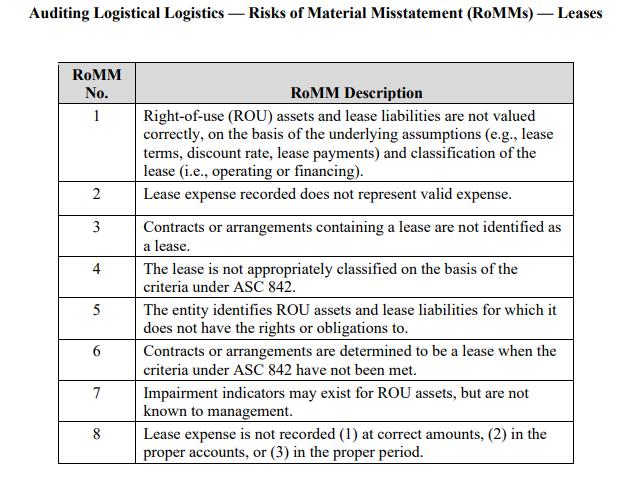

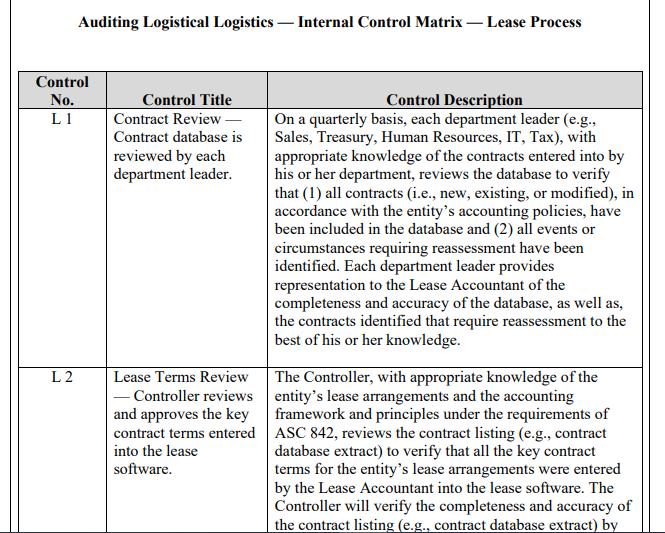

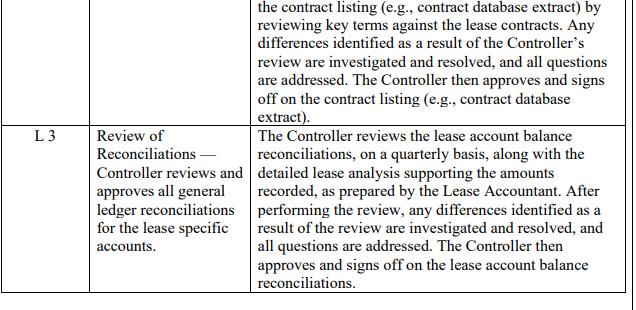

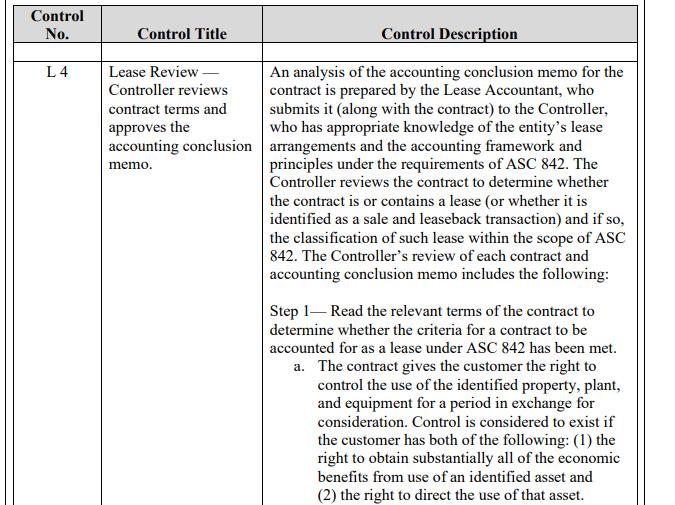

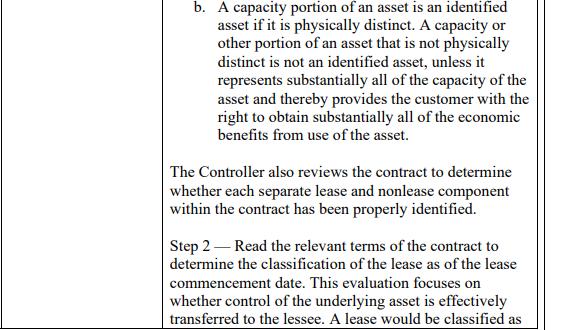

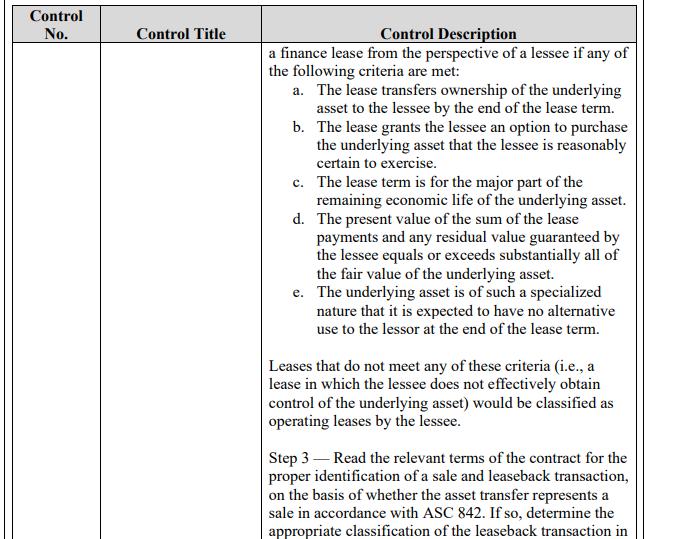

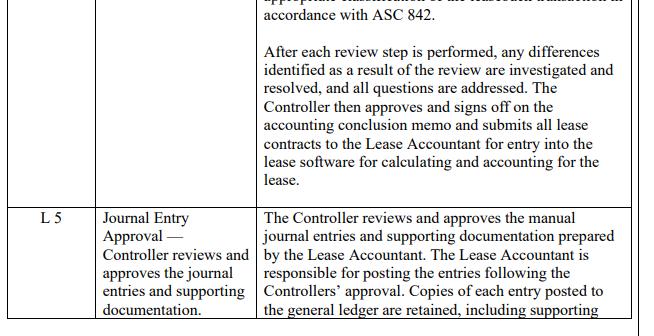

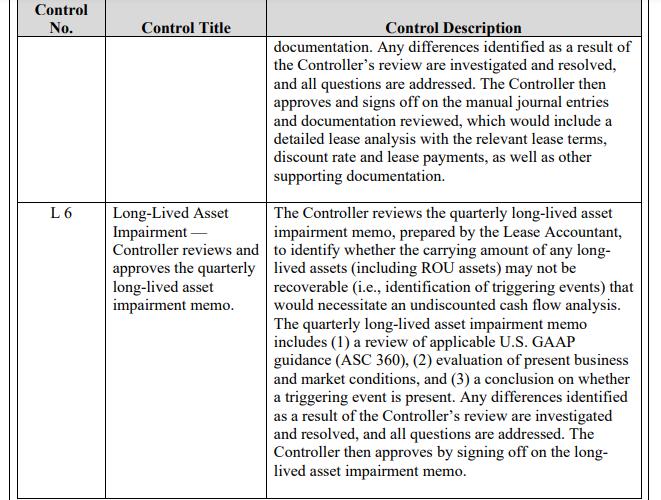

Logistical Logistics Inc. (Logistical Logistics or the "Company") provides transportation and logistics services to customers throughout a network of offices in North America, South America, and Asia. The Company contracts fleets of shipping vessels, trucks, and aircraft to provide regional, long-haul, and international shipments of customer goods. In addition, the Company contracts warehouse operators across North America for use of their facilities as distribution centers that temporarily store goods in transit. Assume the Company has adopted the new leasing standard, ASC 842, Leases. The Company has entered into the following contracts with the vendors identified below. Logistical Logistics enters into a contract with See Boat Inc. (See Boat) to use its shipping vessels to transport customer goods from North America to Asia. See Boat has a fleet of 25 multi-use shipping vessels, each of which has the capacity to hold 1,000 shipping containers. Logistical Logistics enters into a contract with Fly-By-Air Inc. (Fly-By-Air) to use its aircraft to transport customer goods from South America to North America. Fly-By-Air has a fleet of 50 multi-use aircraft, each of which has the capacity to hold 500 shipping pallets of customer goods. Logistical Logistics enters into a contract with Trucking Co. Inc. (Trucking Co.) to use its trucks to transport customer goods from distribution centers to retail stores across North America. Trucking Co. has a fleet of 1,500 multi-use long-haul trucking carriers, each of which has the capacity to hold 100 shipping pallets of goods. Logistical Logistics enters into a contract with Warehouse Co. Inc. (Warehouse Co.) to store up to 18,000 shipping pallets of customer goods at one of Warehouse Co.'s locations. Warehouse Co. has the capacity to store 20,000 shipping pallets of goods. The terms of the shipping contracts are as follows: See Boat o The contract term is for the voyage to transport Logistical Logistics' cargo from Los Angeles to Shanghai. Logistical Logistics does not have discretion to change the departure or arrival ports without a renegotiation of the contract fees. o SB0829, a commercial shipping vessel in See Boat's fleet, is dedicated to delivering Logistical Logistics' cargo for the term of the contract. See Boat cannot substitute SB0829 with another vessel in its fleet. Copyright © 2020 Deloitte Development LLC All Rights Reserved. o The contract identifies the shipping containers and acceptable cargo (e.g., semiconductors) to be transported on the ship as well as the transportation route. Logistical Logistics does not have discretion to change the identified cargo without renegotiating the contract fees. o See Boat is responsible for the safe passage of the cargo, as well as operation and maintenance of SB0829. The crew determines the ship's route, speeds, and date of departure from Los Angeles. In addition, Logistical Logistics cannot, under any circumstances, replace See Boat's crew. • Fly-By-Air o The contract term is five years. o FBA1231, a commercial aircraft in Fly-By-Air's fleet, is dedicated to delivering Logistical Logistics' shipping pallets during the term of the contract. o Logistical Logistics determines (1) the airports from and to which goods are shipped and received and (2) the order in which deliveries are made to the airports. Fly-By-Air provides the aircraft's pilot and crew, and Logistical Logistics instructs Fly-By-Air accordingly. o While Logistical Logistics determines what cargo will be transported throughout the term of the contract, certain restrictions prevent the Company from shipping flammable materials. o Logistical Logistics has the right to send the aircraft regardless of whether its cargo levels meet the full storage capacity of the aircraft. If FBA1231 is below capacity, Fly-By-Air cannot use the excess storage space to ship products of its other customers. • Trucking Co. o The contract term is five years. o Trucking Co. must deliver Logistical Logistics' shipments within three weeks of the Company's notification that it has pallets of customer goods ready for shipping. o Trucking Co. may choose any truck from its fleet to fulfill the shipping request. o Logistical Logistics may request shipment of 25 to 100 shipping pallets of goods in a single request. (Individual shipping requests generally do not exceed 50 shipping pallets.) o Trucking Co. has the right to use any excess storage space to ship products of its other customers. Copyright © 2020 Deloitte Development LLC All Rights Reserved. o Trucking Co. determines the shipment's delivery date (within the three-week period), as well as the shipping route. Warehouse Co. o The contract term is 10 years. o Logistical Logistics can store up to 18,000 shipping pallets at one specified Warehouse Co. location. Logistical Logistics will be charged for storage of 18,000 shipping pallets, regardless of the actual number of pallets stored, and Warehouse Co. cannot use any of Logistical Logistics' unused storage space for other storage needs. o Warehouse Co. can use the remaining space in its warehouse for other storage needs. o o Warehouse Co. cannot relocate Logistical Logistics' inventory to another facility. Logistical Logistics has the right to decide which shipping pallets are placed in storage and when they can be removed. o Warehouse Co. provides the loading and unloading services for the warehouse activities, both of which are dependent on Logistical Logistics' decisions about which shipping pallets are placed in storage and when they can be removed. The CFO of Logistical Logistics recognizes that the new leasing standard contains certain provisions that may affect how the Company treats contracts of this nature. Note that you have been provided with Handout 1, which contains the risks of material misstatement (RoMMs) matrix, and Handout 2, which is Logistical Logistics' control matrix. Required Activities: 1. On the basis of the facts related to the contracts between the Company and its vendors, what are the RoMMs that we may identify as part of our audit to address the completeness and existence of those contracts that are or contain a lease? Handout 1, the RoMMs matrix, may be used to assist with identifying relevant RoMMs. 2. Tailoring RoMMs to the specific lease contracts and assertions is an important step in designing an audit plan for leases. Now that you have identified the RoMMs that are applicable to the contracts between the Company and its vendors, how might you tailor the RoMMs that you identified in Activity 1 to the facts presented in this case? 3. Identify internal controls that address the tailored RoMMs identified in Activity 2. Handout 2, Logistical Logistics' internal control matrix, may be used to assist with identifying relevant internal controls. 4. Design substantive procedures that address the tailored RoMMs identified in Activity 2. Auditing Logistical Logistics - Risks of Material Misstatement (RoMMs) - Leases ROMM No. 1 2 3 4 5 6 7 8 ROMM Description Right-of-use (ROU) assets and lease liabilities are not valued correctly, on the basis of the underlying assumptions (e.g., lease terms, discount rate, lease payments) and classification of the lease (i.e., operating or financing). Lease expense recorded does not represent valid expense. Contracts or arrangements containing a lease are not identified as a lease. The lease is not appropriately classified on the basis of the criteria under ASC 842. The entity identifies ROU assets and lease liabilities for which it does not have the rights or obligations to. Contracts or arrangements are determined to be a lease when the criteria under ASC 842 have not been met. Impairment indicators may exist for ROU assets, but are not known to management. Lease expense is not recorded (1) at correct amounts, (2) in the proper accounts, or (3) in the proper period. Auditing Logistical Logistics - Internal Control Matrix - Lease Process Control No. L1 L2 Control Title Contract Review - Contract database is reviewed by each department leader. Lease Terms Review Controller reviews and approves the key contract terms entered into the lease software. Control Description On a quarterly basis, each department leader (e.g., Sales, Treasury, Human Resources, IT, Tax), with appropriate knowledge of the contracts entered into by his or her department, reviews the database to verify that (1) all contracts (i.e., new, existing, or modified), in accordance with the entity's accounting policies, have been included in the database and (2) all events or circumstances requiring reassessment have been identified. Each department leader provides representation to the Lease Accountant of the completeness and accuracy of the database, as well as, the contracts identified that require reassessment to the best of his or her knowledge. The Controller, with appropriate knowledge of the entity's lease arrangements and the accounting framework and principles under the requirements of ASC 842, reviews the contract listing (e.g., contract database extract) to verify that all the key contract terms for the entity's lease arrangements were entered by the Lease Accountant into the lease software. The Controller will verify the completeness and accuracy of the contract listing (e.g., contract database extract) by L 3 Review of Reconciliations - Controller reviews and approves all general ledger reconciliations for the lease specific accounts. the contract listing (e.g., contract database extract) by reviewing key terms against the lease contracts. Any differences identified as a result of the Controller's review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the contract listing (e.g., contract database extract). The Controller reviews the lease account balance reconciliations, on a quarterly basis, along with the detailed lease analysis supporting the amounts recorded, as prepared by the Lease Accountant. After performing the review, any differences identified as a result of the review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the lease account balance reconciliations. Control No. L4 Control Title Lease Review - Controller reviews contract terms and approves the accounting conclusion memo. Control Description An analysis of the accounting conclusion memo for the contract is prepared by the Lease Accountant, who submits it (along with the contract) to the Controller, who has appropriate knowledge of the entity's lease arrangements and the accounting framework and principles under the requirements of ASC 842. The Controller reviews the contract to determine whether the contract is or contains a lease (or whether it is identified as a sale and leaseback transaction) and if so, the classification of such lease within the scope of ASC 842. The Controller's review of each contract and accounting conclusion memo includes the following: Step 1- Read the relevant terms of the contract to determine whether the criteria for a contract to be accounted for as a lease under ASC 842 has been met. a. The contract gives the customer the right to control the use of the identified property, plant, and equipment for a period in exchange for consideration. Control is considered to exist if the customer has both of the following: (1) the right to obtain substantially all of the economic benefits from use of an identified asset and (2) the right to direct the use of that asset. b. A capacity portion of an asset is an identified asset if it is physically distinct. A capacity or other portion of an asset that is not physically distinct is not an identified asset, unless it represents substantially all of the capacity of the asset and thereby provides the customer with the right to obtain substantially all of the economic benefits from use of the asset. The Controller also reviews the contract to determine whether each separate lease and nonlease component within the contract has been properly identified. Step 2 - Read the relevant terms of the contract to determine the classification of the lease as of the lease commencement date. This evaluation focuses on whether control of the underlying asset is effectively transferred to the lessee. A lease would be classified as Control No. Control Title Control Description a finance lease from the perspective of a lessee if any of the following criteria are met: a. b. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. c. d. The lease term is for the major part of the remaining economic life of the underlying asset. The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. e. The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. Leases that do not meet any of these criteria (i.e., a lease in which the lessee does not effectively obtain control of the underlying asset) would be classified as operating leases by the lessee. Step 3 Read the relevant terms of the contract for the proper identification of a sale and leaseback transaction, on the basis of whether the asset transfer represents a sale in accordance with ASC 842. If so, determine the appropriate classification of the leaseback transaction in L5 Journal Entry Approval Controller reviews and approves the journal entries and supporting documentation. accordance with ASC 842. After each review step is performed, any differences identified as a result of the review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the accounting conclusion memo and submits all lease contracts to the Lease Accountant for entry into the lease software for calculating and accounting for the lease. The Controller reviews and approves the manual journal entries and supporting documentation prepared by the Lease Accountant. The Lease Accountant is responsible for posting the entries following the Controllers' approval. Copies of each entry posted to the general ledger are retained, including supporting Control No. L6 Control Title Long-Lived Asset Impairment Controller reviews and approves the quarterly long-lived asset impairment memo. Control Description documentation. Any differences identified as a result of the Controller's review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the manual journal entries and documentation reviewed, which would include a detailed lease analysis with the relevant lease terms, discount rate and lease payments, as well as other supporting documentation. The Controller reviews the quarterly long-lived asset impairment memo, prepared by the Lease Accountant, to identify whether the carrying amount of any long- lived assets (including ROU assets) may not be recoverable (i.e., identification of triggering events) that would necessitate an undiscounted cash flow analysis. The quarterly long-lived asset impairment memo includes (1) a review of applicable U.S. GAAP guidance (ASC 360), (2) evaluation of present business and market conditions, and (3) a conclusion on whether a triggering event is present. Any differences identified as a result of the Controller's review are investigated and resolved, and all questions are addressed. The Controller then approves by signing off on the long- lived asset impairment memo. Logistical Logistics Inc. (Logistical Logistics or the "Company") provides transportation and logistics services to customers throughout a network of offices in North America, South America, and Asia. The Company contracts fleets of shipping vessels, trucks, and aircraft to provide regional, long-haul, and international shipments of customer goods. In addition, the Company contracts warehouse operators across North America for use of their facilities as distribution centers that temporarily store goods in transit. Assume the Company has adopted the new leasing standard, ASC 842, Leases. The Company has entered into the following contracts with the vendors identified below. Logistical Logistics enters into a contract with See Boat Inc. (See Boat) to use its shipping vessels to transport customer goods from North America to Asia. See Boat has a fleet of 25 multi-use shipping vessels, each of which has the capacity to hold 1,000 shipping containers. Logistical Logistics enters into a contract with Fly-By-Air Inc. (Fly-By-Air) to use its aircraft to transport customer goods from South America to North America. Fly-By-Air has a fleet of 50 multi-use aircraft, each of which has the capacity to hold 500 shipping pallets of customer goods. Logistical Logistics enters into a contract with Trucking Co. Inc. (Trucking Co.) to use its trucks to transport customer goods from distribution centers to retail stores across North America. Trucking Co. has a fleet of 1,500 multi-use long-haul trucking carriers, each of which has the capacity to hold 100 shipping pallets of goods. Logistical Logistics enters into a contract with Warehouse Co. Inc. (Warehouse Co.) to store up to 18,000 shipping pallets of customer goods at one of Warehouse Co.'s locations. Warehouse Co. has the capacity to store 20,000 shipping pallets of goods. The terms of the shipping contracts are as follows: See Boat o The contract term is for the voyage to transport Logistical Logistics' cargo from Los Angeles to Shanghai. Logistical Logistics does not have discretion to change the departure or arrival ports without a renegotiation of the contract fees. o SB0829, a commercial shipping vessel in See Boat's fleet, is dedicated to delivering Logistical Logistics' cargo for the term of the contract. See Boat cannot substitute SB0829 with another vessel in its fleet. Copyright © 2020 Deloitte Development LLC All Rights Reserved. o The contract identifies the shipping containers and acceptable cargo (e.g., semiconductors) to be transported on the ship as well as the transportation route. Logistical Logistics does not have discretion to change the identified cargo without renegotiating the contract fees. o See Boat is responsible for the safe passage of the cargo, as well as operation and maintenance of SB0829. The crew determines the ship's route, speeds, and date of departure from Los Angeles. In addition, Logistical Logistics cannot, under any circumstances, replace See Boat's crew. • Fly-By-Air o The contract term is five years. o FBA1231, a commercial aircraft in Fly-By-Air's fleet, is dedicated to delivering Logistical Logistics' shipping pallets during the term of the contract. o Logistical Logistics determines (1) the airports from and to which goods are shipped and received and (2) the order in which deliveries are made to the airports. Fly-By-Air provides the aircraft's pilot and crew, and Logistical Logistics instructs Fly-By-Air accordingly. o While Logistical Logistics determines what cargo will be transported throughout the term of the contract, certain restrictions prevent the Company from shipping flammable materials. o Logistical Logistics has the right to send the aircraft regardless of whether its cargo levels meet the full storage capacity of the aircraft. If FBA1231 is below capacity, Fly-By-Air cannot use the excess storage space to ship products of its other customers. • Trucking Co. o The contract term is five years. o Trucking Co. must deliver Logistical Logistics' shipments within three weeks of the Company's notification that it has pallets of customer goods ready for shipping. o Trucking Co. may choose any truck from its fleet to fulfill the shipping request. o Logistical Logistics may request shipment of 25 to 100 shipping pallets of goods in a single request. (Individual shipping requests generally do not exceed 50 shipping pallets.) o Trucking Co. has the right to use any excess storage space to ship products of its other customers. Copyright © 2020 Deloitte Development LLC All Rights Reserved. o Trucking Co. determines the shipment's delivery date (within the three-week period), as well as the shipping route. Warehouse Co. o The contract term is 10 years. o Logistical Logistics can store up to 18,000 shipping pallets at one specified Warehouse Co. location. Logistical Logistics will be charged for storage of 18,000 shipping pallets, regardless of the actual number of pallets stored, and Warehouse Co. cannot use any of Logistical Logistics' unused storage space for other storage needs. o Warehouse Co. can use the remaining space in its warehouse for other storage needs. o o Warehouse Co. cannot relocate Logistical Logistics' inventory to another facility. Logistical Logistics has the right to decide which shipping pallets are placed in storage and when they can be removed. o Warehouse Co. provides the loading and unloading services for the warehouse activities, both of which are dependent on Logistical Logistics' decisions about which shipping pallets are placed in storage and when they can be removed. The CFO of Logistical Logistics recognizes that the new leasing standard contains certain provisions that may affect how the Company treats contracts of this nature. Note that you have been provided with Handout 1, which contains the risks of material misstatement (RoMMs) matrix, and Handout 2, which is Logistical Logistics' control matrix. Required Activities: 1. On the basis of the facts related to the contracts between the Company and its vendors, what are the RoMMs that we may identify as part of our audit to address the completeness and existence of those contracts that are or contain a lease? Handout 1, the RoMMs matrix, may be used to assist with identifying relevant RoMMs. 2. Tailoring RoMMs to the specific lease contracts and assertions is an important step in designing an audit plan for leases. Now that you have identified the RoMMs that are applicable to the contracts between the Company and its vendors, how might you tailor the RoMMs that you identified in Activity 1 to the facts presented in this case? 3. Identify internal controls that address the tailored RoMMs identified in Activity 2. Handout 2, Logistical Logistics' internal control matrix, may be used to assist with identifying relevant internal controls. 4. Design substantive procedures that address the tailored RoMMs identified in Activity 2. Auditing Logistical Logistics - Risks of Material Misstatement (RoMMs) - Leases ROMM No. 1 2 3 4 5 6 7 8 ROMM Description Right-of-use (ROU) assets and lease liabilities are not valued correctly, on the basis of the underlying assumptions (e.g., lease terms, discount rate, lease payments) and classification of the lease (i.e., operating or financing). Lease expense recorded does not represent valid expense. Contracts or arrangements containing a lease are not identified as a lease. The lease is not appropriately classified on the basis of the criteria under ASC 842. The entity identifies ROU assets and lease liabilities for which it does not have the rights or obligations to. Contracts or arrangements are determined to be a lease when the criteria under ASC 842 have not been met. Impairment indicators may exist for ROU assets, but are not known to management. Lease expense is not recorded (1) at correct amounts, (2) in the proper accounts, or (3) in the proper period. Auditing Logistical Logistics - Internal Control Matrix - Lease Process Control No. L1 L2 Control Title Contract Review - Contract database is reviewed by each department leader. Lease Terms Review Controller reviews and approves the key contract terms entered into the lease software. Control Description On a quarterly basis, each department leader (e.g., Sales, Treasury, Human Resources, IT, Tax), with appropriate knowledge of the contracts entered into by his or her department, reviews the database to verify that (1) all contracts (i.e., new, existing, or modified), in accordance with the entity's accounting policies, have been included in the database and (2) all events or circumstances requiring reassessment have been identified. Each department leader provides representation to the Lease Accountant of the completeness and accuracy of the database, as well as, the contracts identified that require reassessment to the best of his or her knowledge. The Controller, with appropriate knowledge of the entity's lease arrangements and the accounting framework and principles under the requirements of ASC 842, reviews the contract listing (e.g., contract database extract) to verify that all the key contract terms for the entity's lease arrangements were entered by the Lease Accountant into the lease software. The Controller will verify the completeness and accuracy of the contract listing (e.g., contract database extract) by L 3 Review of Reconciliations - Controller reviews and approves all general ledger reconciliations for the lease specific accounts. the contract listing (e.g., contract database extract) by reviewing key terms against the lease contracts. Any differences identified as a result of the Controller's review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the contract listing (e.g., contract database extract). The Controller reviews the lease account balance reconciliations, on a quarterly basis, along with the detailed lease analysis supporting the amounts recorded, as prepared by the Lease Accountant. After performing the review, any differences identified as a result of the review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the lease account balance reconciliations. Control No. L4 Control Title Lease Review - Controller reviews contract terms and approves the accounting conclusion memo. Control Description An analysis of the accounting conclusion memo for the contract is prepared by the Lease Accountant, who submits it (along with the contract) to the Controller, who has appropriate knowledge of the entity's lease arrangements and the accounting framework and principles under the requirements of ASC 842. The Controller reviews the contract to determine whether the contract is or contains a lease (or whether it is identified as a sale and leaseback transaction) and if so, the classification of such lease within the scope of ASC 842. The Controller's review of each contract and accounting conclusion memo includes the following: Step 1- Read the relevant terms of the contract to determine whether the criteria for a contract to be accounted for as a lease under ASC 842 has been met. a. The contract gives the customer the right to control the use of the identified property, plant, and equipment for a period in exchange for consideration. Control is considered to exist if the customer has both of the following: (1) the right to obtain substantially all of the economic benefits from use of an identified asset and (2) the right to direct the use of that asset. b. A capacity portion of an asset is an identified asset if it is physically distinct. A capacity or other portion of an asset that is not physically distinct is not an identified asset, unless it represents substantially all of the capacity of the asset and thereby provides the customer with the right to obtain substantially all of the economic benefits from use of the asset. The Controller also reviews the contract to determine whether each separate lease and nonlease component within the contract has been properly identified. Step 2 - Read the relevant terms of the contract to determine the classification of the lease as of the lease commencement date. This evaluation focuses on whether control of the underlying asset is effectively transferred to the lessee. A lease would be classified as Control No. Control Title Control Description a finance lease from the perspective of a lessee if any of the following criteria are met: a. b. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. c. d. The lease term is for the major part of the remaining economic life of the underlying asset. The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. e. The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. Leases that do not meet any of these criteria (i.e., a lease in which the lessee does not effectively obtain control of the underlying asset) would be classified as operating leases by the lessee. Step 3 Read the relevant terms of the contract for the proper identification of a sale and leaseback transaction, on the basis of whether the asset transfer represents a sale in accordance with ASC 842. If so, determine the appropriate classification of the leaseback transaction in L5 Journal Entry Approval Controller reviews and approves the journal entries and supporting documentation. accordance with ASC 842. After each review step is performed, any differences identified as a result of the review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the accounting conclusion memo and submits all lease contracts to the Lease Accountant for entry into the lease software for calculating and accounting for the lease. The Controller reviews and approves the manual journal entries and supporting documentation prepared by the Lease Accountant. The Lease Accountant is responsible for posting the entries following the Controllers' approval. Copies of each entry posted to the general ledger are retained, including supporting Control No. L6 Control Title Long-Lived Asset Impairment Controller reviews and approves the quarterly long-lived asset impairment memo. Control Description documentation. Any differences identified as a result of the Controller's review are investigated and resolved, and all questions are addressed. The Controller then approves and signs off on the manual journal entries and documentation reviewed, which would include a detailed lease analysis with the relevant lease terms, discount rate and lease payments, as well as other supporting documentation. The Controller reviews the quarterly long-lived asset impairment memo, prepared by the Lease Accountant, to identify whether the carrying amount of any long- lived assets (including ROU assets) may not be recoverable (i.e., identification of triggering events) that would necessitate an undiscounted cash flow analysis. The quarterly long-lived asset impairment memo includes (1) a review of applicable U.S. GAAP guidance (ASC 360), (2) evaluation of present business and market conditions, and (3) a conclusion on whether a triggering event is present. Any differences identified as a result of the Controller's review are investigated and resolved, and all questions are addressed. The Controller then approves by signing off on the long- lived asset impairment memo.

Expert Answer:

Answer rating: 100% (QA)

See Boat The voyage to carry Logical Logistics goods from Los Angeles to Shanghai is covered by the contract term Without renegotiating the contract payments Logical Logistics does not have the author... View the full answer

Related Book For

International Business and the New Realities

ISBN: 978-0136090984

2nd Edition

Authors: S. Tamer Cavusgil, Gary Knight, John R. Riesenberger

Posted Date:

Students also viewed these accounting questions

-

Target adopted the new leasing standard for the year ended February 2, 2019, using the modified retrospective approach outlined in ASC Topic 842. All questions relate to the year ended February 2,...

-

The Roadnet Transport Company expanded its shipping capacity by purchasing 90 trailer trucks from a bankrupt competitor. The company subsequently located 30 of the purchased trucks at each of its...

-

The Fly Company provides advertising services for clients across the nation. The Fly Company is presently working on four projects, each for a different client. The Fly Company accumulates costs for...

-

Explain the difference between product placement & branded entertainment . Do you personally notice product placements in television shows or movies? Why or why not? Identify at least two factors...

-

On October 1, 2014, Dejour Energy Inc. issued a $680,000, 7%, seven-year bond. Interest is to be paid annually each October 1. Required a. Calculate the issue price of the bond assuming a market...

-

State and local governments typically offer their employees defined benefit pension plans. Under these plans, employees are promised a fixed monthly payment after they retire. A governments pension...

-

Why does collusion pose unique prevention and detection challenges?

-

Golden Corp., a merchandiser, recently completed its 2013 operations. For the year, (1) all sales are credit sales, (2) all credits to Accounts Receivable reflect cash receipts from customers, (3)...

-

Consider the acceleration of a good sports car in real life . (1) Pick a certain car model, which could be the one you are driving, or the one you wish you were --- and search online for its...

-

The information listed below refers to the employees of Lemonica Company for the year ended December 31, 2016. The wages are separated into the quarters in which they were paid to the individual...

-

Assume each state of nature has an equal probability of occurrence. Holding period returns in percent State of Nature 1 2 3 4 A -10 5 15 20 B 2508 12 -8 a) Calculate the expected rate of return for A...

-

Carla Vista Hot Dog Stand had the following results last month: Sales revenues were $6200, variable costs were $3100, and fixed costs were $1550 per month. If Carla Vista wants to achieve a targeted...

-

A long forward contract on a non - dividend - paying stock was entered into some time ago. It currently has six months to maturity. The risk - free rate of interest ( with continuous compounding ) is...

-

What is your annual NOI? Your property has four units, all occupied. Two rent for $1,200 per month, and two rent for $1,350 per month. Assume Vacancy and Bad Debt (combined) of 4%. Expenses are as...

-

Scott also mentioned the following: The expenses for dues and subscriptions were his country club membership dues for the year. $400 of the charitable contributions were made to a political action...

-

Write a program in MATLAB to find the average of three numbers.

-

Blue Company is a multiproduct firm. Presented below is information concerning one of its products, the Hawkeye. Price/Cost Date 1/1 2/4 2/20 4/2 11/4 Transaction Beginning inventory Purchase Sale...

-

You are thinking of investing in one of two companies. In one annual report, the auditors opinion states that the financial statements were prepared in accordance with generally accepted accounting...

-

Consider Toshibas laptop computer division. In terms of the marketing program elements, what attributes of laptop computers does the firm need to adapt and which attributes can it standardize for...

-

Suppose you get a job at Aoki Corporation, a firm that manufactures glass for industrial and consumer markets. Aoki is a large firm but has little international experience. Senior managers are...

-

Assume you own a company that manufactures medical products in the biotechnology industry. You want to establish a foreign plant to manufacture your products and are seeking countries with a high...

-

Find the input-output differential equation relating \(v_{o}\) and \(v_{i}(t)\) for the circuit shown below. w R R Vo v(t) R L

-

Consider the following circuit where \(i_{i}(t)\) is the input current and \(i_{o}(t)\) is the output current. (a) Obtain the State-Variable Matrix model \((A, B, C, D)\) for the circuit. (b) Obtain...

-

(a) For the following circuit find the State-Variable Matrix model (A, B, C, D) where \(v_{o}\) is the output voltage and \(v_{i}\) is the input voltage. (b) Also, find the input-output differential...

Study smarter with the SolutionInn App