Question: Long Question 3 ( 2 5 points total, 5 points each ) Let R A and R B denote the returns on securities A and

Long Question points total, points each

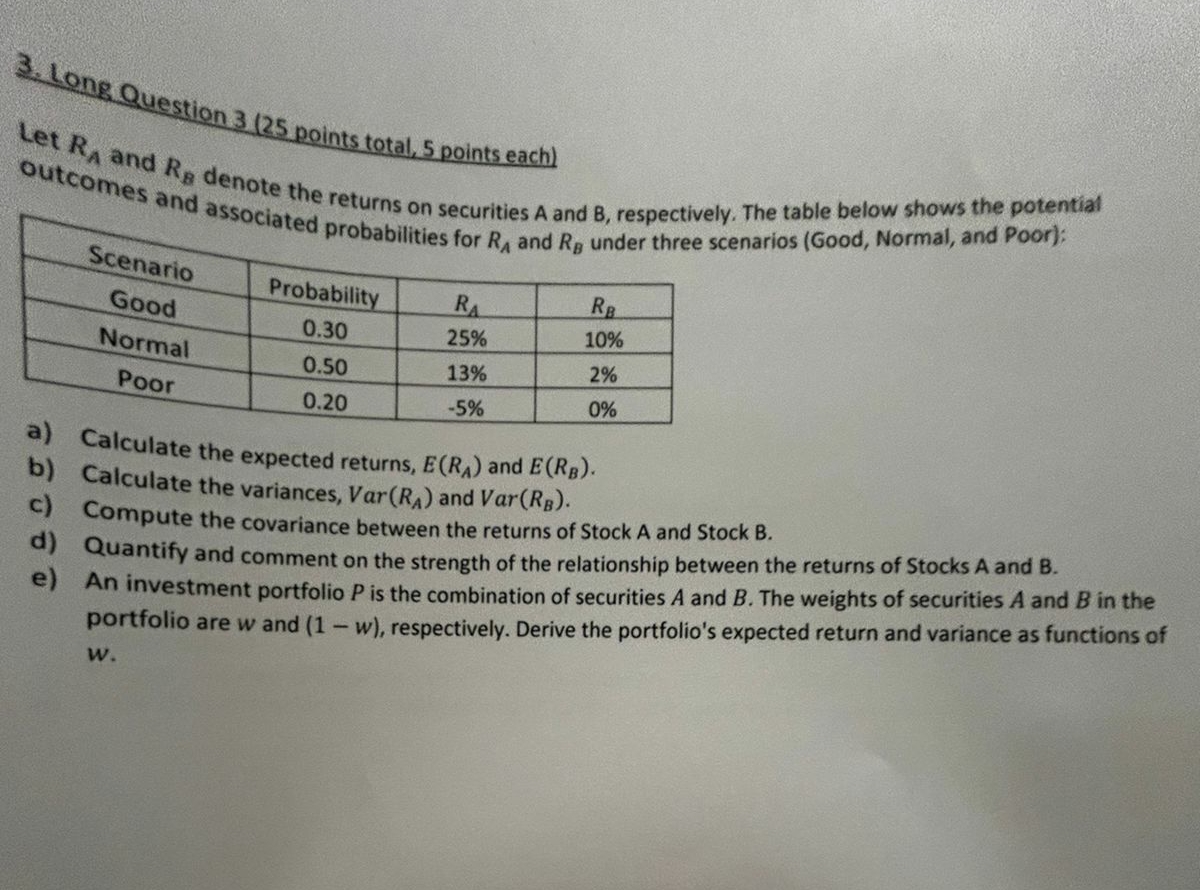

Let and denote the returns on securities A and respectively. The table below shows the potential outcomes and associated probabilities for and under three scenarios Good Normal, and Poor:

a Calculate the expected returns, and

b Calculate the variances, Var and Var

c Compute the covariance between the returns of Stock A and Stock B

d Quantify and comment on the strength of the relationship between the returns of Stocks A and

e An investment portfolio is the combination of securities A and The weights of securities A and in the portfolio are and respectively. Derive the portfolio's expected return and variance as functions of

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock