Question: Looking for help for g & h, the last couple pieces of this question. 1. Consider a one-period economy with two times, 0 and T.

Looking for help for g & h, the last couple pieces of this question.

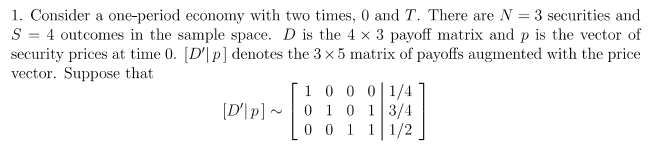

1. Consider a one-period economy with two times, 0 and T. There are N = 3 securities and S = 4 outcomes in the sample space. D is the 4 x 3 payoff matrix and p is the vector of security prices at time 0. (D'|p] denotes the 3 x 5 matrix of payoffs augmented with the price vector. Suppose that 1 0 0 0 1/4 [DP] ~ 010 1 3/4 0 0 1 1 1/2 (g) What is the price of the payoff X = [0,1,1,2]'? (h) Is a risk-free payoff attainable? Explain. 1. Consider a one-period economy with two times, 0 and T. There are N = 3 securities and S = 4 outcomes in the sample space. D is the 4 x 3 payoff matrix and p is the vector of security prices at time 0. (D'|p] denotes the 3 x 5 matrix of payoffs augmented with the price vector. Suppose that 1 0 0 0 1/4 [DP] ~ 010 1 3/4 0 0 1 1 1/2 (g) What is the price of the payoff X = [0,1,1,2]'? (h) Is a risk-free payoff attainable? Explain

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts