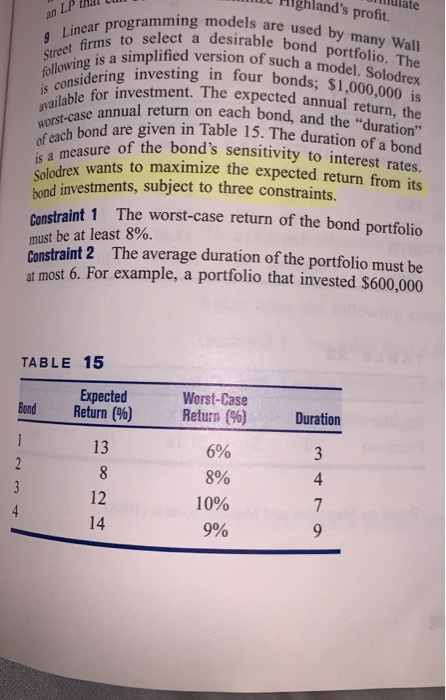

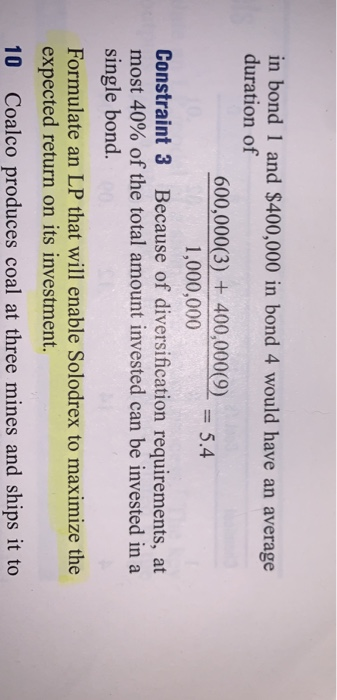

Question: LP the cu wear programming models are used 9 Linear propre Unulate ML Highland's profit. hodels are used by many Wall ect a desirable bond

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock