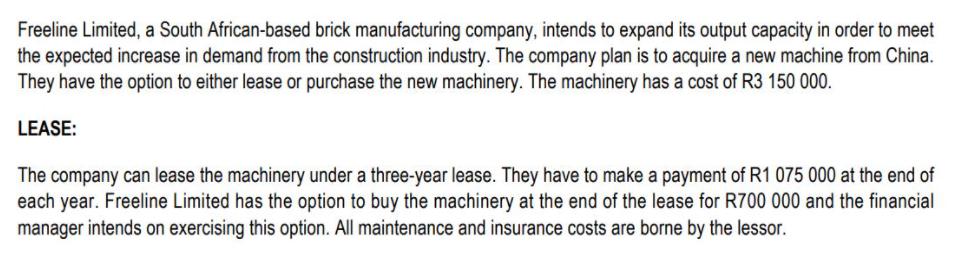

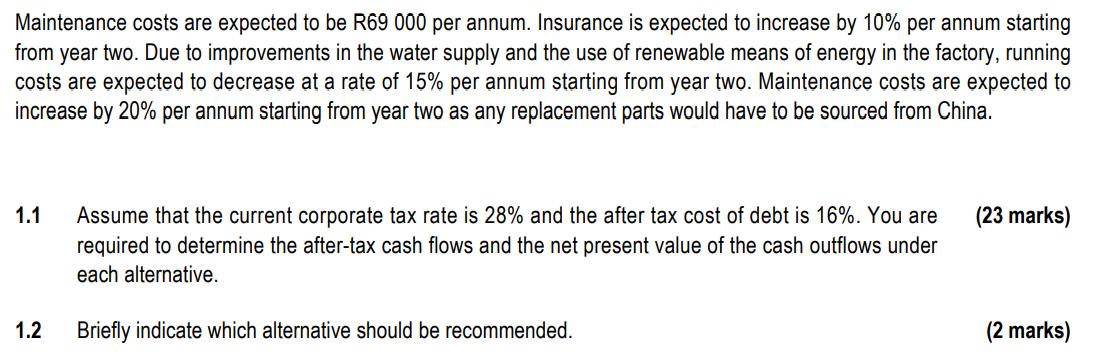

Freeline Limited, a South African-based brick manufacturing company, intends to expand its output capacity in order...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

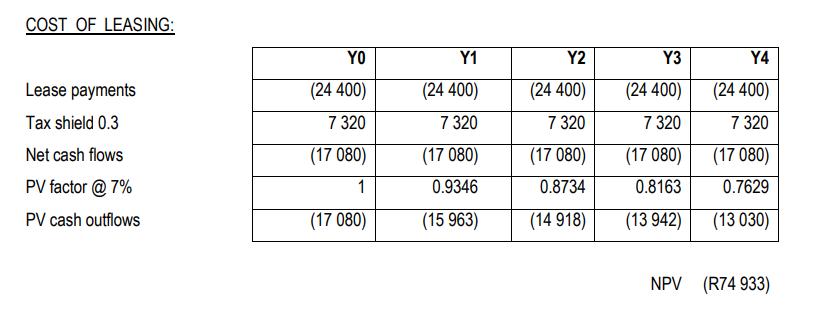

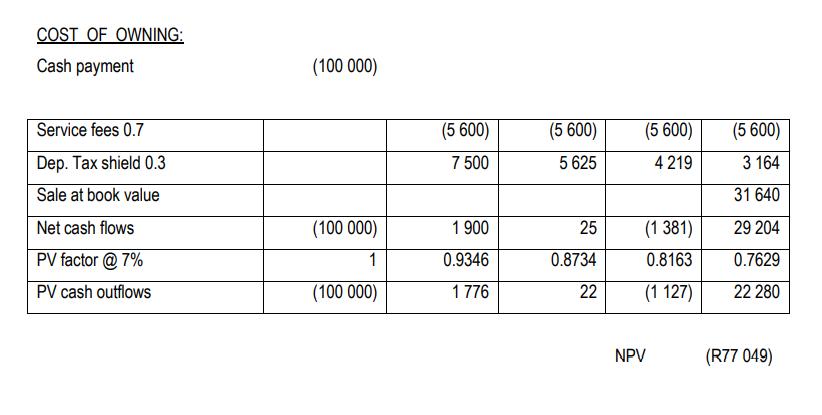

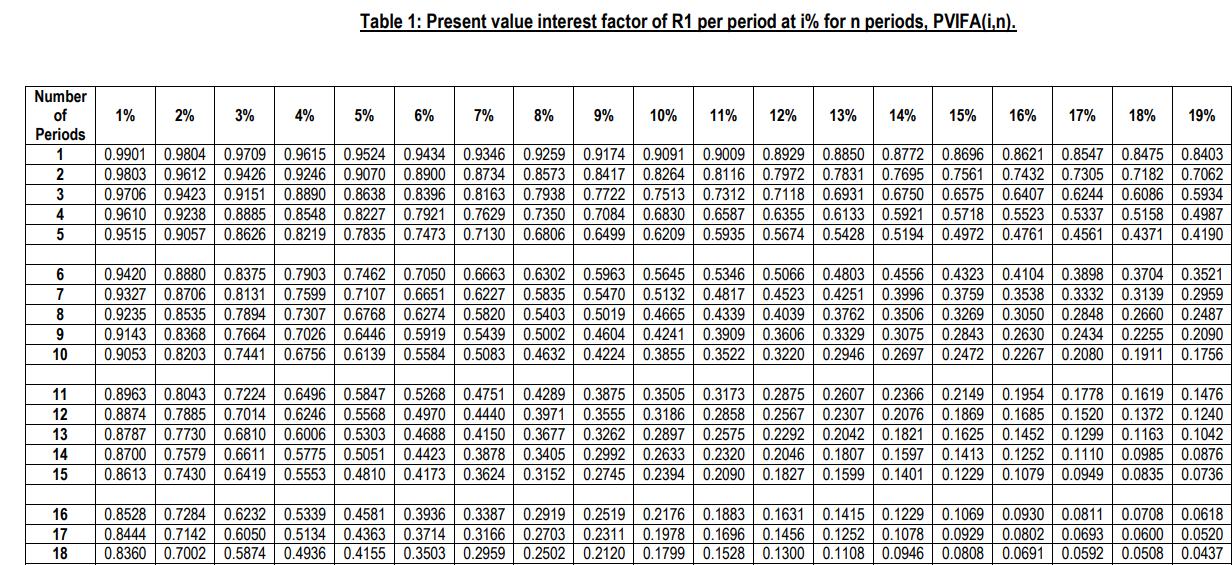

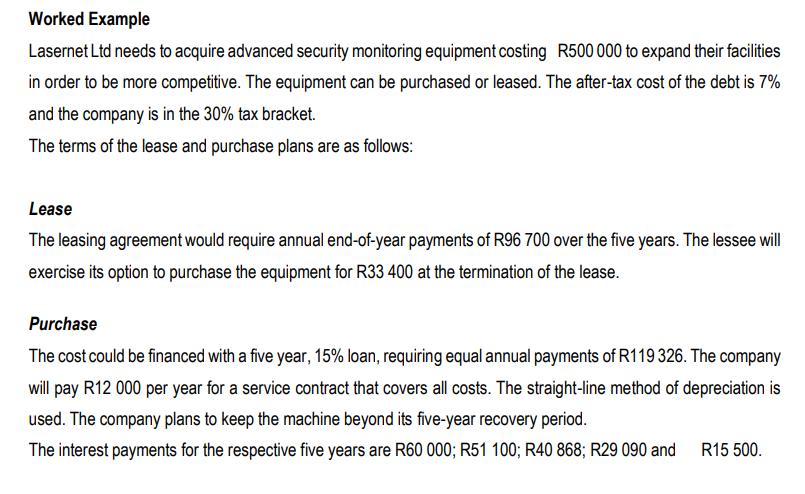

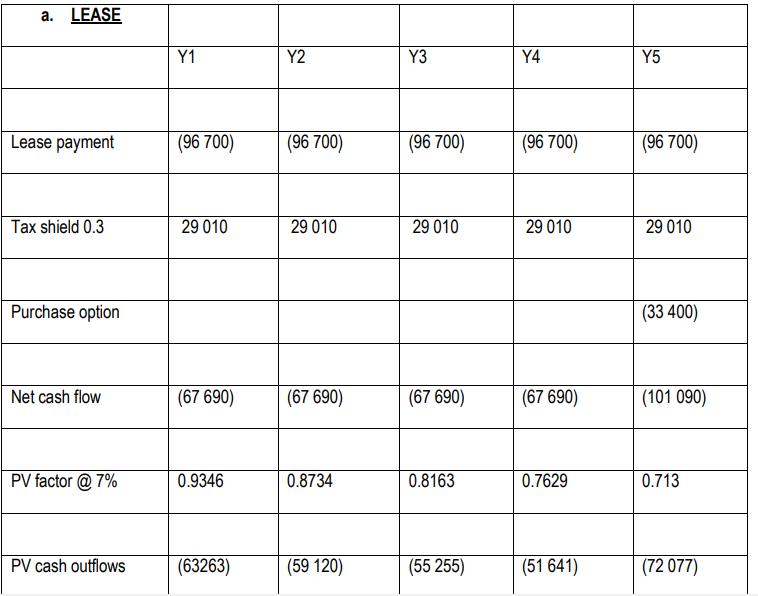

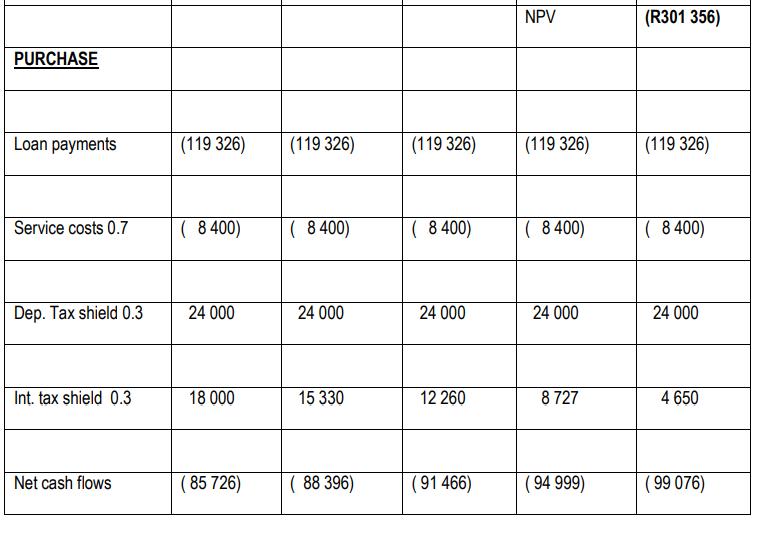

Freeline Limited, a South African-based brick manufacturing company, intends to expand its output capacity in order to meet the expected increase in demand from the construction industry. The company plan is to acquire a new machine from China. They have the option to either lease or purchase the new machinery. The machinery has a cost of R3 150 000. LEASE: The company can lease the machinery under a three-year lease. They have to make a payment of R1 075 000 at the end of each year. Freeline Limited has the option to buy the machinery at the end of the lease for R700 000 and the financial manager intends on exercising this option. All maintenance and insurance costs are borne by the lessor. Maintenance costs are expected to be R69 000 per annum. Insurance is expected to increase by 10% per annum starting from year two. Due to improvements in the water supply and the use of renewable means of energy in the factory, running costs are expected to decrease at a rate of 15% per annum starting from year two. Maintenance costs are expected to increase by 20% per annum starting from year two as any replacement parts would have to be sourced from China. 1.1 (23 marks) Assume that the current corporate tax rate is 28% and the after tax cost of debt is 16%. You are required to determine the after-tax cash flows and the net present value of the cash outflows under each alternative. 1.2 Briefly indicate which alternative should be recommended. (2 marks) COST OF LEASING: YO Y1 Y2 Y3 Y4 Lease payments (24 400) (24 400) (24 400) (24 400) (24 400) Tax shield 0.3 7 320 7 320 7 320 7 320 7 320 Net cash flows (17 080) (17 080) (17 080) (17 080) (17 080) PV factor @ 7% 1 0.9346 0.8734 0.8163 0.7629 PV cash outflows (17 080) (15 963) (14 918) (13 942) (13 030) NPV (R74 933) COST OF OWNING: Cash payment (100 000) Service fees 0.7 (5 600) (5 600) (5 600) (5 600) Dep. Tax shield 0.3 7 500 5 625 4 219 3 164 Sale at book value 31 640 Net cash flows (100 000) 1 900 25 (1 381) 29 204 PV factor @ 7% 1 0.9346 0.8734 0.8163 0.7629 PV cash outflows (100 000) 1776 22 (1 127) 22 280 NPV (R77 049) Table 1: Present value interest factor of R1 per period at i% forn periods, PVIFA(i.n). Number of 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19% Periods 0.9901 0.9804 0.9709 0.9615 0.9524 0.9434 0.9346 0.9259 0.9174 0.9091 0.9009 0.8573 0.8417 0.8264 0.8116 0.7722 0.7513 0.7312 0.6830 0.6587 0.8929 0.8850 0.8772 0.8696 0.8621 0.7972 0.7831 0.7695 0.7561 0.6931 0.8547 0.8475 0.8403 0.7432 0.7305 0.7182 0.7062 0.6575 0.6407 0.6244 0.6086 0.5934 0.5718 0.5523 | 0.5337 0.5158 0.4987 0.4561 0.4371 0.4190 1 0.9803 0.9612 0.9706 0.9423 0.9151 0.9426 0.9246 0.9070 0.8900 0.8890 0.8638 0.8396 0.9610 | 0.9238 0.8885 0.8548 0.8227 0.7921 0.7629 0.7350 0.7084 0.8626 0.8219 0.7835 0.7473 0.7130 2 0.8734 0.6750 0.6355 0.6133 0.5921 3 0.8163 0.7938 0.7118 4 0.9515 0.9057 0.6806 0.6499 0.6209 0.5935 0.5674 0.5428 0.5194 0.4972 0.4761 0.9420 | 0.8880 0.8375 0.7903 0.7462 0.7050 0.6663 0.9327 0.8706 | 0.8131 0.5963 0.5645 0.5346 0.5132 0.4817 0.9235 0.8535 0.7894 0.7307 0.6768 0.6274 0.5820 0.5403 0.5019 0.4665 0.4339 0.4039 0.3762 0.3506 0.3269 0.3050 0.2848 0.2660 0.2487 0.4803 0.4556 0.4323 0.4104 0.3898 0.3704 0.3521 0.3759 0.3538 0.3332 0.3139 0.2959 6 0.6302 0.5066 7 0.7599 0.7107 0.6651 0.6227 0.5835 0.5470 0.4523 0.4251 0.3996 8 0.9143 0.8368 0.7664 0.7026 0.6446 0.5919 0.9053 0.8203 0.5439 0.5002 0.4604 0.4241 0.3909 0.3606 0.3329 0.3075 0.2843 0.2630 0.2434 0.2255 0.2090 0.3522 0.3220 0.2946 | 0.2697 9 10 0.7441 0.6756 0.6139 0.5584 0.5083 0.4632 0.4224 0.3855 0.2472 0.2267 0.2080 0.1911 0.1756 0.8963 0.8043 0.7224 0.6496 0.5847 0.5268 0.8874 0.7885 0.8787 0.7730 0.8700 0.7579 0.6611 0.5775 0.5051 0.4423 0.3878 0.3405 0.2992 0.2633 0.2320 0.2046 | 0.1807 0.1597 0.8613 0.7430 0.6419 0.5553 0.4810 0.4173 0.3624 0.3152 0.2745 0.2394 0.2090 0.1827 0.1599 0.1401 0.1229 0.1079 0.0949 0.0835 0.0736 0.3505 0.3173 0.2875 0.2607 0.2366 0.2149 0.1954 0.1778 0.1619 0.1476 0.4289 0.3971 0.3555 0.3186| 0.2858 0.2567 0.2307 0.2076 0.1869 0.1685 0.1520 0.1372 0.1240 0.3677 0.3262 0.2897 0.2575 0.2292 11 0.4751 0.3875 0.7014 0.6246 0.5568 0.4970 0.4440 0.6810 | 0.6006 0.5303 0.4688 12 0.2042 0.1821 0.1625 0.1452 0.1299 0.1163 0.1413 0.1252 0.1110 0.0985 0.0876 13 0.4150 0.1042 14 15 0.4581 0.3936 0.3387 0.2919 0.2519 0.2176 0.1883 0.1631 0.1415 0.1229 0.1069 0.0930 0.0811 0.0708 0.0618 0.8528 0.7284 0.6232 0.5339 0.8444 0.7142 0.6050 0.5134 0.4363 0.3714 0.3166 0.2703 0.2311 0.1978 0.1696 0.1456 0.1252 0.1078 0.0929 0.0802 0.0693 0.0600 0.0520 0.8360 0.7002 0.5874 0.4936 0.4155 0.3503 0.2959 0.2502 0.2120 0.1799 0.1528 0.1300 0.1108 0.0946 0.0808 0.0691 0.0592 0.0508 0.0437 16 17 18 Worked Example Lasernet Ltd needs to acquire advanced security monitoring equipment costing R500 000 to expand their facilities in order to be more competitive. The equipment can be purchased or leased. The after-tax cost of the debt is 7% and the company is in the 30% tax bracket. The terms of the lease and purchase plans are as follows: Lease The leasing agreement would require annual end-of-year payments of R96 700 over the five years. The lessee will exercise its option to purchase the equipment for R33 400 at the termination of the lease. Purchase The cost could be financed with a five year, 15% loan, requiring equal annual payments of R119 326. The company will pay R12 000 per year for a service contract that covers all costs. The straight-line method of depreciation is used. The company plans to keep the machine beyond its five-year recovery period. The interest payments for the respective five years are R60 000; R51 100; R40 868; R29 090 and R15 500. a. LEASE Y1 Y2 Y3 Y4 Y5 Lease payment (96 700) (96 700) (96 700) (96 700) (96 700) Tax shield 0.3 29 010 29 010 29 010 29 010 29 010 Purchase option (33 400) Net cash flow (67 690) (67 690) (67 690) (67 690) (101 090) PV factor @ 7% 0.9346 0.8734 0.8163 0.7629 0.713 PV cash outflows (63263) (59 120) (55 255) (51 641) (72 077) NPV (R301 356) PURCHASE Loan payments (119 326) (119 326) (119 326) (119 326) (119 326) Service costs 0.7 ( 8400) ( 8400) ( 8 400) ( 8400) ( 8400) Dep. Tax shield 0.3 24 000 24 000 24 000 24 000 24 000 Int. tax shield 0.3 18 000 15 330 12 260 8 727 4 650 Net cash flows ( 85 726) ( 88 396) (91 466) ( 94 999) (99 076) PV factor @ 7% 0.9346 0.8734 0.8163 0.7629 0.713 PV cash outflows ( 80 120) ( 77 205) ( 74 664) ( 72 475) ( 70 641) NPV (R375 105) Freeline Limited, a South African-based brick manufacturing company, intends to expand its output capacity in order to meet the expected increase in demand from the construction industry. The company plan is to acquire a new machine from China. They have the option to either lease or purchase the new machinery. The machinery has a cost of R3 150 000. LEASE: The company can lease the machinery under a three-year lease. They have to make a payment of R1 075 000 at the end of each year. Freeline Limited has the option to buy the machinery at the end of the lease for R700 000 and the financial manager intends on exercising this option. All maintenance and insurance costs are borne by the lessor. Maintenance costs are expected to be R69 000 per annum. Insurance is expected to increase by 10% per annum starting from year two. Due to improvements in the water supply and the use of renewable means of energy in the factory, running costs are expected to decrease at a rate of 15% per annum starting from year two. Maintenance costs are expected to increase by 20% per annum starting from year two as any replacement parts would have to be sourced from China. 1.1 (23 marks) Assume that the current corporate tax rate is 28% and the after tax cost of debt is 16%. You are required to determine the after-tax cash flows and the net present value of the cash outflows under each alternative. 1.2 Briefly indicate which alternative should be recommended. (2 marks) COST OF LEASING: YO Y1 Y2 Y3 Y4 Lease payments (24 400) (24 400) (24 400) (24 400) (24 400) Tax shield 0.3 7 320 7 320 7 320 7 320 7 320 Net cash flows (17 080) (17 080) (17 080) (17 080) (17 080) PV factor @ 7% 1 0.9346 0.8734 0.8163 0.7629 PV cash outflows (17 080) (15 963) (14 918) (13 942) (13 030) NPV (R74 933) COST OF OWNING: Cash payment (100 000) Service fees 0.7 (5 600) (5 600) (5 600) (5 600) Dep. Tax shield 0.3 7 500 5 625 4 219 3 164 Sale at book value 31 640 Net cash flows (100 000) 1 900 25 (1 381) 29 204 PV factor @ 7% 1 0.9346 0.8734 0.8163 0.7629 PV cash outflows (100 000) 1776 22 (1 127) 22 280 NPV (R77 049) Table 1: Present value interest factor of R1 per period at i% forn periods, PVIFA(i.n). Number of 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19% Periods 0.9901 0.9804 0.9709 0.9615 0.9524 0.9434 0.9346 0.9259 0.9174 0.9091 0.9009 0.8573 0.8417 0.8264 0.8116 0.7722 0.7513 0.7312 0.6830 0.6587 0.8929 0.8850 0.8772 0.8696 0.8621 0.7972 0.7831 0.7695 0.7561 0.6931 0.8547 0.8475 0.8403 0.7432 0.7305 0.7182 0.7062 0.6575 0.6407 0.6244 0.6086 0.5934 0.5718 0.5523 | 0.5337 0.5158 0.4987 0.4561 0.4371 0.4190 1 0.9803 0.9612 0.9706 0.9423 0.9151 0.9426 0.9246 0.9070 0.8900 0.8890 0.8638 0.8396 0.9610 | 0.9238 0.8885 0.8548 0.8227 0.7921 0.7629 0.7350 0.7084 0.8626 0.8219 0.7835 0.7473 0.7130 2 0.8734 0.6750 0.6355 0.6133 0.5921 3 0.8163 0.7938 0.7118 4 0.9515 0.9057 0.6806 0.6499 0.6209 0.5935 0.5674 0.5428 0.5194 0.4972 0.4761 0.9420 | 0.8880 0.8375 0.7903 0.7462 0.7050 0.6663 0.9327 0.8706 | 0.8131 0.5963 0.5645 0.5346 0.5132 0.4817 0.9235 0.8535 0.7894 0.7307 0.6768 0.6274 0.5820 0.5403 0.5019 0.4665 0.4339 0.4039 0.3762 0.3506 0.3269 0.3050 0.2848 0.2660 0.2487 0.4803 0.4556 0.4323 0.4104 0.3898 0.3704 0.3521 0.3759 0.3538 0.3332 0.3139 0.2959 6 0.6302 0.5066 7 0.7599 0.7107 0.6651 0.6227 0.5835 0.5470 0.4523 0.4251 0.3996 8 0.9143 0.8368 0.7664 0.7026 0.6446 0.5919 0.9053 0.8203 0.5439 0.5002 0.4604 0.4241 0.3909 0.3606 0.3329 0.3075 0.2843 0.2630 0.2434 0.2255 0.2090 0.3522 0.3220 0.2946 | 0.2697 9 10 0.7441 0.6756 0.6139 0.5584 0.5083 0.4632 0.4224 0.3855 0.2472 0.2267 0.2080 0.1911 0.1756 0.8963 0.8043 0.7224 0.6496 0.5847 0.5268 0.8874 0.7885 0.8787 0.7730 0.8700 0.7579 0.6611 0.5775 0.5051 0.4423 0.3878 0.3405 0.2992 0.2633 0.2320 0.2046 | 0.1807 0.1597 0.8613 0.7430 0.6419 0.5553 0.4810 0.4173 0.3624 0.3152 0.2745 0.2394 0.2090 0.1827 0.1599 0.1401 0.1229 0.1079 0.0949 0.0835 0.0736 0.3505 0.3173 0.2875 0.2607 0.2366 0.2149 0.1954 0.1778 0.1619 0.1476 0.4289 0.3971 0.3555 0.3186| 0.2858 0.2567 0.2307 0.2076 0.1869 0.1685 0.1520 0.1372 0.1240 0.3677 0.3262 0.2897 0.2575 0.2292 11 0.4751 0.3875 0.7014 0.6246 0.5568 0.4970 0.4440 0.6810 | 0.6006 0.5303 0.4688 12 0.2042 0.1821 0.1625 0.1452 0.1299 0.1163 0.1413 0.1252 0.1110 0.0985 0.0876 13 0.4150 0.1042 14 15 0.4581 0.3936 0.3387 0.2919 0.2519 0.2176 0.1883 0.1631 0.1415 0.1229 0.1069 0.0930 0.0811 0.0708 0.0618 0.8528 0.7284 0.6232 0.5339 0.8444 0.7142 0.6050 0.5134 0.4363 0.3714 0.3166 0.2703 0.2311 0.1978 0.1696 0.1456 0.1252 0.1078 0.0929 0.0802 0.0693 0.0600 0.0520 0.8360 0.7002 0.5874 0.4936 0.4155 0.3503 0.2959 0.2502 0.2120 0.1799 0.1528 0.1300 0.1108 0.0946 0.0808 0.0691 0.0592 0.0508 0.0437 16 17 18 Worked Example Lasernet Ltd needs to acquire advanced security monitoring equipment costing R500 000 to expand their facilities in order to be more competitive. The equipment can be purchased or leased. The after-tax cost of the debt is 7% and the company is in the 30% tax bracket. The terms of the lease and purchase plans are as follows: Lease The leasing agreement would require annual end-of-year payments of R96 700 over the five years. The lessee will exercise its option to purchase the equipment for R33 400 at the termination of the lease. Purchase The cost could be financed with a five year, 15% loan, requiring equal annual payments of R119 326. The company will pay R12 000 per year for a service contract that covers all costs. The straight-line method of depreciation is used. The company plans to keep the machine beyond its five-year recovery period. The interest payments for the respective five years are R60 000; R51 100; R40 868; R29 090 and R15 500. a. LEASE Y1 Y2 Y3 Y4 Y5 Lease payment (96 700) (96 700) (96 700) (96 700) (96 700) Tax shield 0.3 29 010 29 010 29 010 29 010 29 010 Purchase option (33 400) Net cash flow (67 690) (67 690) (67 690) (67 690) (101 090) PV factor @ 7% 0.9346 0.8734 0.8163 0.7629 0.713 PV cash outflows (63263) (59 120) (55 255) (51 641) (72 077) NPV (R301 356) PURCHASE Loan payments (119 326) (119 326) (119 326) (119 326) (119 326) Service costs 0.7 ( 8400) ( 8400) ( 8 400) ( 8400) ( 8400) Dep. Tax shield 0.3 24 000 24 000 24 000 24 000 24 000 Int. tax shield 0.3 18 000 15 330 12 260 8 727 4 650 Net cash flows ( 85 726) ( 88 396) (91 466) ( 94 999) (99 076) PV factor @ 7% 0.9346 0.8734 0.8163 0.7629 0.713 PV cash outflows ( 80 120) ( 77 205) ( 74 664) ( 72 475) ( 70 641) NPV (R375 105)

Expert Answer:

Answer rating: 100% (QA)

Answer The company shall choose the LEASE alternative as the cost of leasing it at their present value is only 218689338 compared to the cost of purchase which is 25228543 The company can save33596092 ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The estimated medical costs are expected to be $7,500 during an employee's retirement. The retiree is expected to pay 30% of the cost and Medicare is expected to pay 50% of the cost. What is the...

-

Omega Processors, Inc., a relatively new high growing graphics chip manufacturer, has decided it needs to raise needed operational capital, expand into developing markets, fund their pension plan,...

-

Next year's sales for Cumberland Mfg. are expected to be $22 million. Current sales are $18 million, based on current assets of $5 million and fixed assets of $5 million. The firm's net profit margin...

-

In Problems 1158, perform the indicated operation, and write each expression in the standard form a + bi. 2 + i i

-

Management games are fun, but you dont really learn anything from them. Discuss.

-

Franklin Training Services (FTS) provides instruction on the use of computer software for the Employees of its corporate clients. It offers courses in the clients offices on the clients equipment....

-

A difference between the innate immune system and the acquired immune system is (a) the innate immune system includes many more different types of receptors than the acquired immune system. (b) the...

-

1. What did Donahoos balance sheet look like at the outset of the firms life? 2. What did the firms balance sheet look like after each transaction? 3. Ignoring taxes, determine how much income...

-

In managing conflict in projects, it is prudent to identify the stakeholders and thereafter to analyse them. By referring to a project that you are familiar with, use an appropriate tool to analyse...

-

Tilger Farm Supply Company manufactures and sells a fertilizer called Snare. The following data are available for preparing budgets for Snare for the first two quarters of 2016. 1. Sales: Quarter 1,...

-

6. Consider the function f(2) = |2| = x +y , z = x+iy. The function f can also be thought of as a function from R2 to R mapping (x, y) to x2 +y. Moreover, since the partial derivatives of f are...

-

Are there certain types of IG Reels that tend to perform better than others? What is the insights regarding the use of hashtags?

-

In the class, they hold opposing views on an emotionally charged political or social issue, for example, private medical clinics, mandatory retirement, legalization of marijuana, or patients' right...

-

Stock A beta = 1,25 and Stock B beta = 0.75. CAPM applies. Expected Return on market portfolio = 10% and Risk free rate of return = 3% 1. What is the expected return of the portfolio consisting of...

-

Amazon has reinvented itself again and again and thrived on organizational change. Since the company went online in 1995, the e-commerce giant has evolved under the leadership of one personJeff...

-

Consider a certain type of machinery that you can buy in the USA for $60,000 and in Japan for 6,780,000 yen. The current exchange rate is 0.01 dollar per yen. Carefully following all numeric...

-

3. Bank Y with this condition, Deposit $10 Million, Capital $10 Million, Reserve $10 Million (Ignore Required Reserve). Securities $5 Million, Mortgage $5 Million. Bank Y wants to add their...

-

The 2017 financial statements of the U.S. government are available at: https://www.fiscal.treasury.gov/fsreports/rpt/finrep/fr/fr_index.htm Use these to answer the following questions: a. Statement...

-

Kate Warner, a senior loan officer with Citybank in Cleveland, Ohio, has both corporate and personal lending customers. On average, the profit contribution margin or interest rate spread is 1.5...

-

A. What firm-specific and industry-specific factors might be used to explain differences among giant corporations in the amount of revenue per employee and profit per employee? B. A multiple...

-

For smaller firms managed by their owners in competitive markets, profit considerations are apt to dominate almost all decisions. However, managers of giant corporations have little contact with...

-

True or False: If indivisible investment 2 is contingent on indivisible investment 1 being funded, then X 2 - X 1 < 0 is added as a constraint to the BLP formulation.

-

Consider a capital budgeting formulation where the binary variables \(x_{1}\) and \(x_{2}\) are used to represent the acceptance \(\left(x_{i}=1 ight)\) or rejection \(\left(x_{i}=0 ight)\) of each...

-

True or False: When multiple independent, divisible investments are available, form the investment portfolio so that the internal rate of return is maximized.

Study smarter with the SolutionInn App