Question: make assumptions if needed (like the par value is $100) Consider the following riskless bonds which can be bought or sold at the following prices/yields:

make assumptions if needed (like the par value is $100)

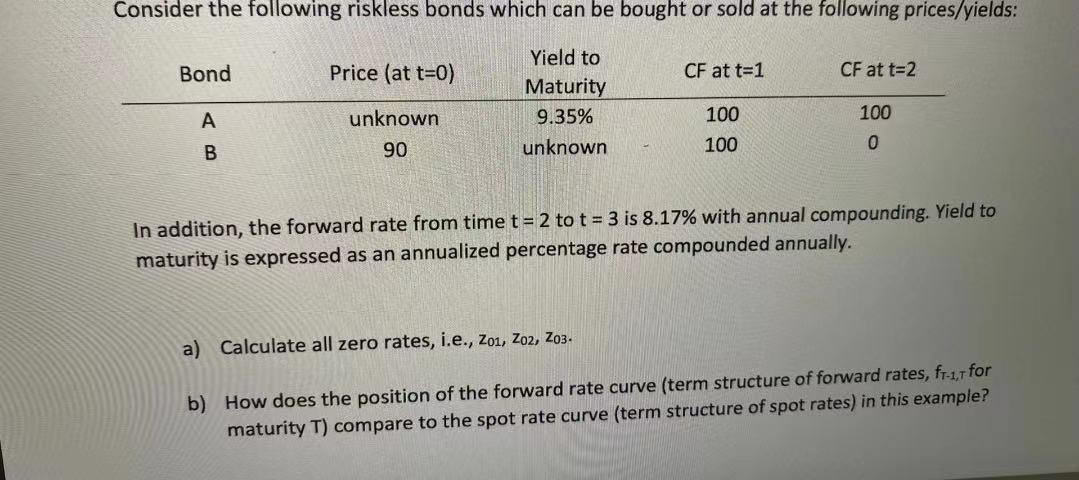

Consider the following riskless bonds which can be bought or sold at the following prices/yields: Bond Price (at t=0) CF at t=1 CF at t=2 Yield to Maturity 9.35% unknown 100 unknown 90 100 0 100 B In addition, the forward rate from time t = 2 to t = 3 is 8.17% with annual compounding. Yield to maturity is expressed as an annualized percentage rate compounded annually. a) Calculate all zero rates, i.e., 201, 202, 203. b) How does the position of the forward rate curve (term structure of forward rates, fr-1,7 for maturity T) compare to the spot rate curve (term structure of spot rates) in this example? Consider the following riskless bonds which can be bought or sold at the following prices/yields: Bond Price (at t=0) CF at t=1 CF at t=2 Yield to Maturity 9.35% unknown 100 unknown 90 100 0 100 B In addition, the forward rate from time t = 2 to t = 3 is 8.17% with annual compounding. Yield to maturity is expressed as an annualized percentage rate compounded annually. a) Calculate all zero rates, i.e., 201, 202, 203. b) How does the position of the forward rate curve (term structure of forward rates, fr-1,7 for maturity T) compare to the spot rate curve (term structure of spot rates) in this example

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts