Question: MANAGEMENT; BA(BS)-601 BBA - VII e: July 6, 2017 TRUCTIONS: Max. Time: 2 Hrs Max. Marks: 60 Attempt any 4 questions. Do not write

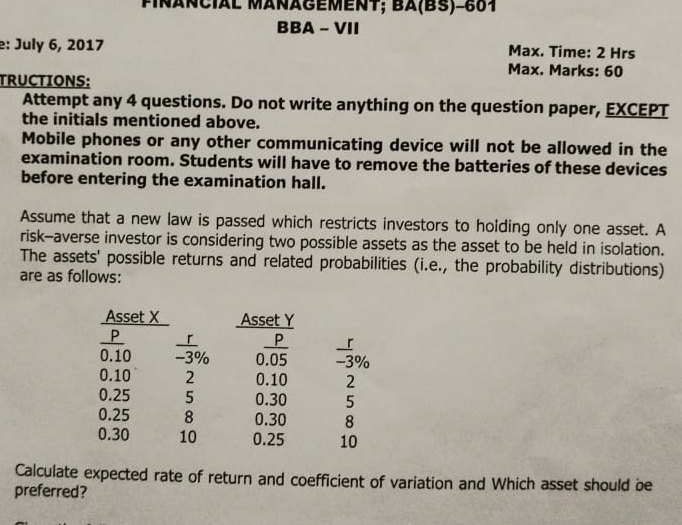

MANAGEMENT; BA(BS)-601 BBA - VII e: July 6, 2017 TRUCTIONS: Max. Time: 2 Hrs Max. Marks: 60 Attempt any 4 questions. Do not write anything on the question paper, EXCEPT the initials mentioned above. Mobile phones or any other communicating device will not be allowed in the examination room. Students will have to remove the batteries of these devices before entering the examination hall. Assume that a new law is passed which restricts investors to holding only one asset. A risk-averse investor is considering two possible assets as the asset to be held in isolation. The assets' possible returns and related probabilities (i.e., the probability distributions) are as follows: Asset X P I Asset Y P 0.10 -3% 0.05 -3% 0.10 2 0.10 2 0.25 5 0.30 5 0.25 8 0.30 8 0.30 10 0.25 10 Calculate expected rate of return and coefficient of variation and Which asset should be preferred?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts