Marathon Oil Corporation, a U.S. petroleum and natural gas exploration and production company, is looking into a

Question:

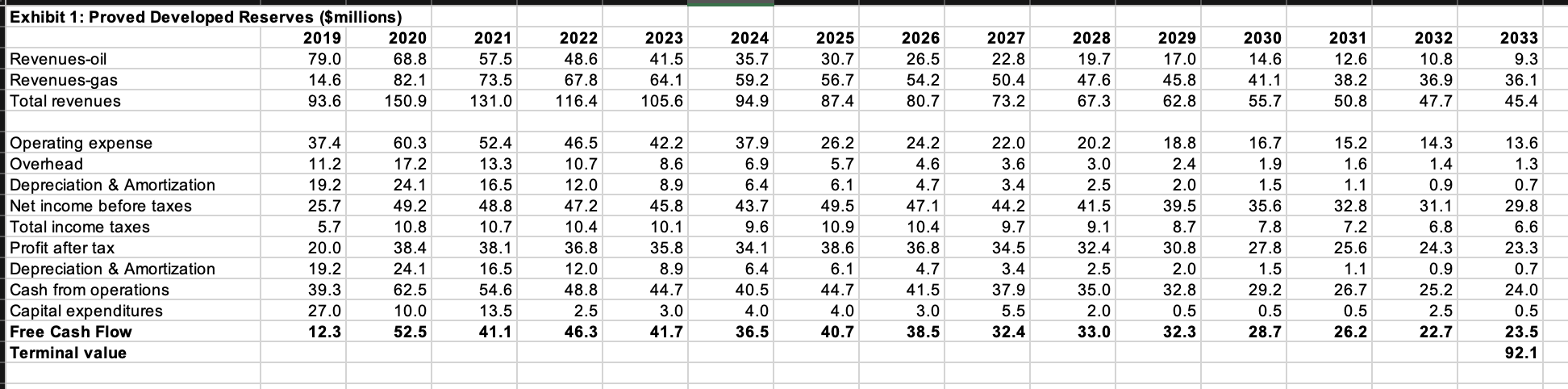

Marathon Oil Corporation, a U.S. petroleum and natural gas exploration and production company, is looking into a possible purchase of a smaller rival Explora Energy. Explora is an owner of oil and gas fields located in Texas and New Mexico. Its wells are currently underperforming relative to the region's benchmarks, and Explora's CEO, Steve Runner, sees an opportunity to sell the wells to Marathon given their interest in acquiring the properties to improve efficiency and increase margins. However, he is unsure about the appropriate sale price. Explora owns both proved developed and proved undeveloped reserves1 Proved developed reserves include mostly producing wells or wells that, while currently non-producing, require only small additional investments to start production. Of course, the production of both oil and gas from these wells would decline over time as the reserves became depleted. Explora also had other reserves that were proved but not developed. To develop these reserves, significant expenditures would be needed to drill new wells, deepen existing wells, or build other infrastructure. Explora estimates that developing these reserves would require additional capital expenditure of about $428 million. Explora does not own all of its fields but leases the mineral rights from their owners. In all cases, the company could wait with developing the fields for at least 5 years without forfeiting these rights. Exhibits 1 and 2 in the attached spreadsheet show projections for the revenues from the proved developed and proved undeveloped reserves and the resulting free cash flows. For simplicity, you can assume that all cash flows occur at the end of the year, and that the current year is 2019, so cash flows in 2019 will not be discounted. Estimates of revenues are based on forecasts of oil and gas prices made by independent economists. Operating expenses and overhead are based on historical costs. Based on the projections in the exhibits, the DCF estimates of the total reserves' value is $385 million. Note that this estimate assumes that the capital expenditures needed to start production are made immediately, i.e. in 2019. If the capital expenditures are postponed, the cash flows from extraction will be postponed too. Your task is to help Mr. Runner to estimate the value of Explora. To value undeveloped reserves, assume that the capital expenditures can be either made immediately (i.e. in 2019) or postponed by 1, 3, or 5 years. For the latter three scenarios, use the Black-Scholes model. To help, you will need to estimate (or assume) S0, X, r, and ?. Please explain how you came up with these estimates. Think about what happens to your option value when you increase T. Does it make sense? (Hint: what happens to S0 when you increase T?). Assume that Explora's WACC is 8.4% and the risk-free rate is 2.5%. Based on historical data in Exhibit 3, the annualized volatility of the percentage changes in oil prices is 39%. The estimate for gas is similar. Decision Time: What is your estimate of the Explora's properties?

Expert Answer:

International Marketing And Export Management

ISBN: 9781292016924

8th Edition

Authors: Gerald Albaum , Alexander Josiassen , Edwin Duerr