Question: Mark an analyst, analyzes two corporate bonds callable at par and having the same characteristics in terms of maturity, coupon rates, as well as

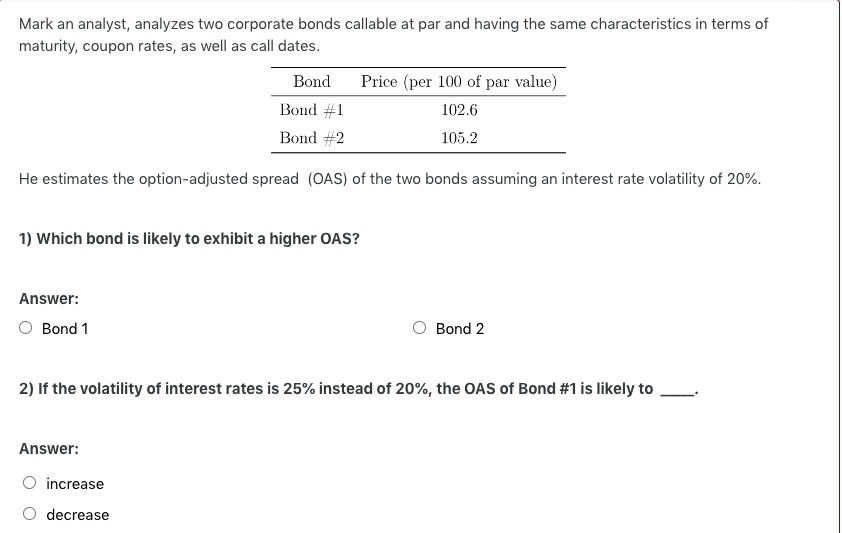

Mark an analyst, analyzes two corporate bonds callable at par and having the same characteristics in terms of maturity, coupon rates, as well as call dates. Bond Bond #1 Bond #2 Price (per 100 of par value) 102.6 105.2 He estimates the option-adjusted spread (OAS) of the two bonds assuming an interest rate volatility of 20%. 1) Which bond is likely to exhibit a higher OAS? Answer: Bond 1 Bond 2 2) If the volatility of interest rates is 25% instead of 20%, the OAS of Bond #1 is likely to Answer: increase decrease

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock