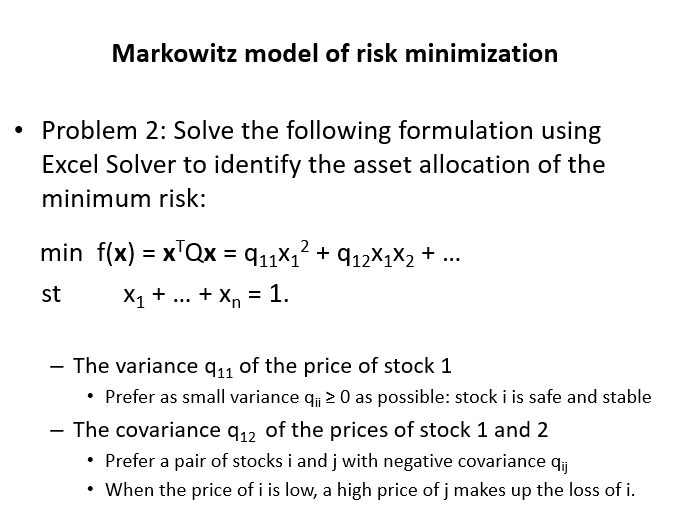

Question: Markowitz model of risk minimization . Problem 2: Solve the following formulation using Excel Solver to identify the asset allocation of the minimum risk: 12

Markowitz model of risk minimization . Problem 2: Solve the following formulation using Excel Solver to identify the asset allocation of the minimum risk: 12 1 2 st x1 + + xn-1. The variance q,11 of the price of stock 1 . Prefer as small variance 0 as possible: stock i is safe and stable - The covariance q12 of the prices of stock 1 and 2 Prefer a pair of stocks i and j with negative covariance q When the price of i is low, a high price of j makes up the loss of i. Markowitz model of risk minimization . Problem 2: Solve the following formulation using Excel Solver to identify the asset allocation of the minimum risk: 12 1 2 st x1 + + xn-1. The variance q,11 of the price of stock 1 . Prefer as small variance 0 as possible: stock i is safe and stable - The covariance q12 of the prices of stock 1 and 2 Prefer a pair of stocks i and j with negative covariance q When the price of i is low, a high price of j makes up the loss of

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts