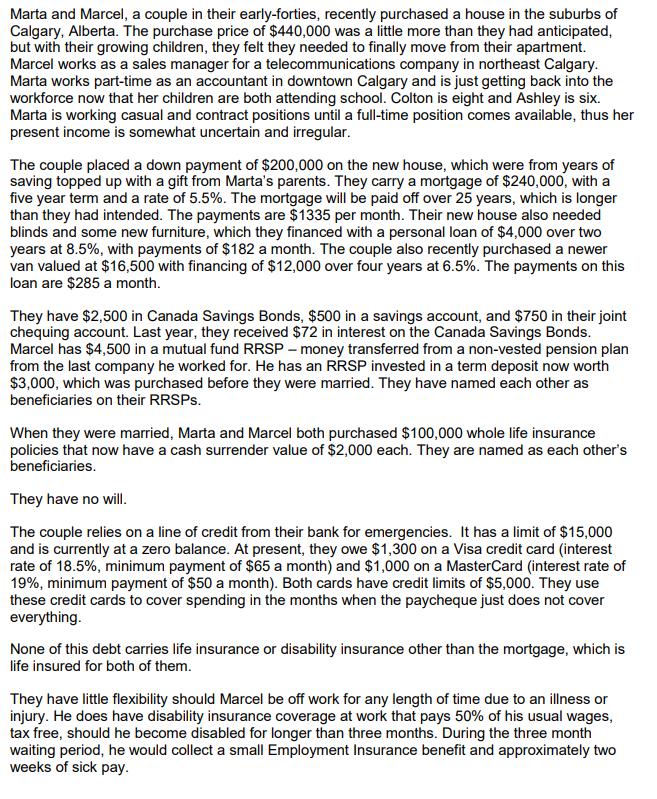

Marta and Marcel, a couple in their early-forties, recently purchased a house in the suburbs of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

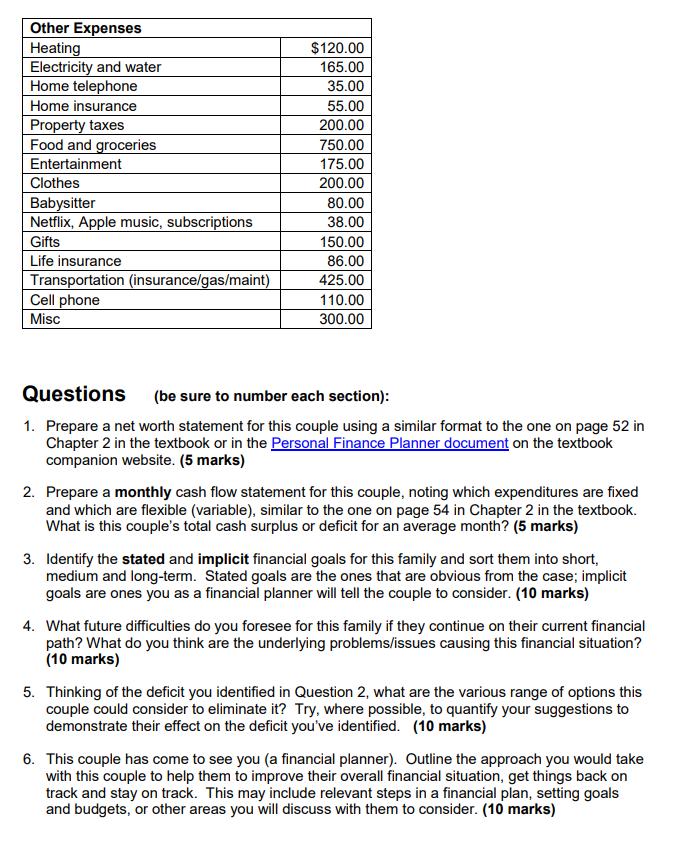

Marta and Marcel, a couple in their early-forties, recently purchased a house in the suburbs of Calgary, Alberta. The purchase price of $440,000 was a little more than they had anticipated, but with their growing children, they felt they needed to finally move from their apartment. Marcel works as a sales manager for a telecommunications company in northeast Calgary. Marta works part-time as an accountant in downtown Calgary and is just getting back into the workforce now that her children are both attending school. Colton is eight and Ashley is six. Marta is working casual and contract positions until a full-time position comes available, thus her present income is somewhat uncertain and irregular. The couple placed a down payment of $200,000 on the new house, which were from years of saving topped up with a gift from Marta's parents. They carry a mortgage of $240,000, with a five year term and a rate of 5.5%. The mortgage will be paid off over 25 years, which is longer than they had intended. The payments are $1335 per month. Their new house also needed blinds and some new furniture, which they financed with a personal loan of $4,000 over two years at 8.5%, with payments of $182 a month. The couple also recently purchased a newer van valued at $16,500 with financing of $12,000 over four years at 6.5%. The payments on this loan are $285 a month. They have $2,500 in Canada Savings Bonds, $500 in a savings account, and $750 in their joint chequing account. Last year, they received $72 in interest on the Canada Savings Bonds. Marcel has $4,500 in a mutual fund RRSP – money transferred from a non-vested pension plan from the last company he worked for. He has an RRSP invested in a term deposit now worth $3,000, which was purchased before they were married. They have named each other as beneficiaries on their RRSPS. When they were married, Marta and Marcel both purchased $100,000 whole life insurance policies that now have a cash surrender value of $2,000 each. They are named as each other's beneficiaries. They have no will. The couple relies on a line of credit from their bank for emergencies. It has a limit of $15,000 and is currently at a zero balance. At present, they owe $1,300 on a Visa credit card (interest rate of 18.5%, minimum payment of $65 a month) and $1,000 on a MasterCard (interest rate of 19%, minimum payment of $50 a month). Both cards have credit limits of $5,000. They use these credit cards to cover spending in the months when the paycheque just does not cover everything. None of this debt carries life insurance or disability insurance other than the mortgage, which is life insured for both of them. They have little flexibility should Marcel be off work for any length of time due to an illness or injury. He does have disability insurance coverage at work that pays 50% of his usual wages, tax free, should he become disabled for longer than three months. During the three month waiting period, he would collect a small Employment Insurance benefit and approximately two weeks of sick pay. Marcel's benefits at work include the use of a leased car and an expense account for entertaining clients. He has a comprehensive dental, drug, and vision care plan as well as a group life insurance policy equaling two times his salary. The company does not have a pension plan but does offer a group RSP, matching each dollar contributed by the employee (up to 5% of their salary). Marcel doesn't feel they have the extra funds right now, so does not currently participate in this plan even though he knows that he is passing up on a substantial contribution by the company by not doing so. Marta does not have any benefits at work, as she is only part-time. Marta and Marcel would like to start renovating the basement of their new home but doubt they can do this until Marta gets a full-time teaching position. The couple rarely takes vacations other than going to Marcel's parent's cabin in British Columbia at a cost of $1,200 each year. They would really like to go to Disneyland next year and figure the trip will cost about $4,000 for all four of them combined. From their view, the only extravagance in their spending is the $2,400 it costs each year to keep the kids in hockey, ballet, and other sports. It seems to Marcel that, with his income of $50,000 a year plus regular commissions of $15,000, they should not be having the money worries they are currently experiencing - but he knows something is not quite right with their financial situation. Before the children were born, the couple spent money quite freely, but with no established management pattern, money now just seems to disappear. They still do not really keep track of their finances or spending – they rarely balance their cheque book and throw all their bills and financial papers on a desk in the den. Many months, they do run out of money in their account before all the bills are paid. They tend to keep their fears and concerns to themselves, rarely communicating their anxieties with each other. Below is a list of monthly net income and expenses that are not already mentioned above. The income figures are net of deductions at source such as income tax, El, and CPP and, in Marcel's case, include his commissions. Income Marcel's monthly take home pay Marta's average monthly net income CSB interest per year $4,050.00 700.00 72.00 Other expenses are provided on the next page. Other Expenses Heating Electricity and water Home telephone $120.00 165.00 35.00 Home insurance 55.00 Property taxes Food and groceries Entertainment Clothes 200.00 750.00 175.00 200.00 Babysitter Netflix, Apple music, subscriptions 80.00 38.00 Gifts 150.00 Life insurance 86.00 Transportation (insurance/gas/maint) Cell phone 425.00 110.00 Misc 300.00 Questions (be sure to number each section): 1. Prepare a net worth statement for this couple using a similar format to the one on page 52 in Chapter 2 in the textbook or in the Personal Finance Planner document on the textbook companion website. (5 marks) 2. Prepare a monthly cash flow statement for this couple, noting which expenditures are fixed and which are flexible (variable), similar to the one on page 54 in Chapter 2 in the textbook. What is this couple's total cash surplus or deficit for an average month? (5 marks) 3. Identify the stated and implicit financial goals for this family and sort them into short, medium and long-term. Stated goals are the ones that are obvious from the case; implicit goals are ones you as a financial planner will tell the couple to consider. (10 marks) 4. What future difficulties do you foresee for this family if they continue on their current financial path? What do you think are the underlying problems/issues causing this financial situation? (10 marks) 5. Thinking of the deficit you identified in Question 2, what are the various range of options this couple could consider to eliminate it? Try, where possible, to quantify your suggestions to demonstrate their effect on the deficit you've identified. (10 marks) 6. This couple has come to see you (a financial planner). Outline the approach you would take with this couple to help them to improve their overall financial situation, get things back on track and stay on track. This may include relevant steps in a financial plan, setting goals and budgets, or other areas you will discuss with them to consider. (10 marks) Marta and Marcel, a couple in their early-forties, recently purchased a house in the suburbs of Calgary, Alberta. The purchase price of $440,000 was a little more than they had anticipated, but with their growing children, they felt they needed to finally move from their apartment. Marcel works as a sales manager for a telecommunications company in northeast Calgary. Marta works part-time as an accountant in downtown Calgary and is just getting back into the workforce now that her children are both attending school. Colton is eight and Ashley is six. Marta is working casual and contract positions until a full-time position comes available, thus her present income is somewhat uncertain and irregular. The couple placed a down payment of $200,000 on the new house, which were from years of saving topped up with a gift from Marta's parents. They carry a mortgage of $240,000, with a five year term and a rate of 5.5%. The mortgage will be paid off over 25 years, which is longer than they had intended. The payments are $1335 per month. Their new house also needed blinds and some new furniture, which they financed with a personal loan of $4,000 over two years at 8.5%, with payments of $182 a month. The couple also recently purchased a newer van valued at $16,500 with financing of $12,000 over four years at 6.5%. The payments on this loan are $285 a month. They have $2,500 in Canada Savings Bonds, $500 in a savings account, and $750 in their joint chequing account. Last year, they received $72 in interest on the Canada Savings Bonds. Marcel has $4,500 in a mutual fund RRSP – money transferred from a non-vested pension plan from the last company he worked for. He has an RRSP invested in a term deposit now worth $3,000, which was purchased before they were married. They have named each other as beneficiaries on their RRSPS. When they were married, Marta and Marcel both purchased $100,000 whole life insurance policies that now have a cash surrender value of $2,000 each. They are named as each other's beneficiaries. They have no will. The couple relies on a line of credit from their bank for emergencies. It has a limit of $15,000 and is currently at a zero balance. At present, they owe $1,300 on a Visa credit card (interest rate of 18.5%, minimum payment of $65 a month) and $1,000 on a MasterCard (interest rate of 19%, minimum payment of $50 a month). Both cards have credit limits of $5,000. They use these credit cards to cover spending in the months when the paycheque just does not cover everything. None of this debt carries life insurance or disability insurance other than the mortgage, which is life insured for both of them. They have little flexibility should Marcel be off work for any length of time due to an illness or injury. He does have disability insurance coverage at work that pays 50% of his usual wages, tax free, should he become disabled for longer than three months. During the three month waiting period, he would collect a small Employment Insurance benefit and approximately two weeks of sick pay. Marcel's benefits at work include the use of a leased car and an expense account for entertaining clients. He has a comprehensive dental, drug, and vision care plan as well as a group life insurance policy equaling two times his salary. The company does not have a pension plan but does offer a group RSP, matching each dollar contributed by the employee (up to 5% of their salary). Marcel doesn't feel they have the extra funds right now, so does not currently participate in this plan even though he knows that he is passing up on a substantial contribution by the company by not doing so. Marta does not have any benefits at work, as she is only part-time. Marta and Marcel would like to start renovating the basement of their new home but doubt they can do this until Marta gets a full-time teaching position. The couple rarely takes vacations other than going to Marcel's parent's cabin in British Columbia at a cost of $1,200 each year. They would really like to go to Disneyland next year and figure the trip will cost about $4,000 for all four of them combined. From their view, the only extravagance in their spending is the $2,400 it costs each year to keep the kids in hockey, ballet, and other sports. It seems to Marcel that, with his income of $50,000 a year plus regular commissions of $15,000, they should not be having the money worries they are currently experiencing - but he knows something is not quite right with their financial situation. Before the children were born, the couple spent money quite freely, but with no established management pattern, money now just seems to disappear. They still do not really keep track of their finances or spending – they rarely balance their cheque book and throw all their bills and financial papers on a desk in the den. Many months, they do run out of money in their account before all the bills are paid. They tend to keep their fears and concerns to themselves, rarely communicating their anxieties with each other. Below is a list of monthly net income and expenses that are not already mentioned above. The income figures are net of deductions at source such as income tax, El, and CPP and, in Marcel's case, include his commissions. Income Marcel's monthly take home pay Marta's average monthly net income CSB interest per year $4,050.00 700.00 72.00 Other expenses are provided on the next page. Other Expenses Heating Electricity and water Home telephone $120.00 165.00 35.00 Home insurance 55.00 Property taxes Food and groceries Entertainment Clothes 200.00 750.00 175.00 200.00 Babysitter Netflix, Apple music, subscriptions 80.00 38.00 Gifts 150.00 Life insurance 86.00 Transportation (insurance/gas/maint) Cell phone 425.00 110.00 Misc 300.00 Questions (be sure to number each section): 1. Prepare a net worth statement for this couple using a similar format to the one on page 52 in Chapter 2 in the textbook or in the Personal Finance Planner document on the textbook companion website. (5 marks) 2. Prepare a monthly cash flow statement for this couple, noting which expenditures are fixed and which are flexible (variable), similar to the one on page 54 in Chapter 2 in the textbook. What is this couple's total cash surplus or deficit for an average month? (5 marks) 3. Identify the stated and implicit financial goals for this family and sort them into short, medium and long-term. Stated goals are the ones that are obvious from the case; implicit goals are ones you as a financial planner will tell the couple to consider. (10 marks) 4. What future difficulties do you foresee for this family if they continue on their current financial path? What do you think are the underlying problems/issues causing this financial situation? (10 marks) 5. Thinking of the deficit you identified in Question 2, what are the various range of options this couple could consider to eliminate it? Try, where possible, to quantify your suggestions to demonstrate their effect on the deficit you've identified. (10 marks) 6. This couple has come to see you (a financial planner). Outline the approach you would take with this couple to help them to improve their overall financial situation, get things back on track and stay on track. This may include relevant steps in a financial plan, setting goals and budgets, or other areas you will discuss with them to consider. (10 marks)

Expert Answer:

Answer rating: 100% (QA)

1 Family Background This is a family of four individual These are their details as at 31 st December 2016 Particulars Husband Wife Daughter Son Common ... View the full answer

Posted Date:

Students also viewed these accounting questions

-

A $7500 loan will be paid off by four equal payments to be made 2, 5, 9, and 12 months after the date of the loan. What is the amount of each payment if the interest rate on the loan is 9.9%?

-

In your capacity as assistant sales manager for a large office products retailer, you have been assigned the task of interviewing purchasing managers for medium and large companies in the San...

-

As the sales manager for EDI how would you approach future reverse auctions?

-

A machine was sold in December 20x3 for $13,000. It was purchased in January 20x1 for $19,000, and depreciation of $16,000 was recorded from the date of purchase through the date of disposal....

-

Suppose that, in a hypothesis test, the null hypothesis is in fact true. a. Is it possible to make a Type I error? Explain your answer. b. Is it possible to make a Type II error? Explain your answer.

-

The 2014 and 2013 comparative balance sheets and 2014 income statement of Sommar Medical Supply Corp. follow: Sommar Medical Supply had no noncash investing and financing transactions during 2014....

-

Describe corporate ethics, the SarbanesOxley Act of 2002, and corporate compliance.

-

On January 1, the company issued 10-year bonds with a face value of $200,000. The bonds carry a coupon rate of 10%, and interest is paid semiannually. On the issue date, the market interest rate for...

-

Need to calculate payback period for each project Project A Year 0 - $-8,000,000 Year 1 - $4,000,000 Year 2 - $2,500,000 Year 3 - $2,500,000 Project B Year 0 - $-4,250,000 Year 1 - $1,500,000 Year 2...

-

The goodwill of $20,000 on Illini's 12/31/20X0 Balance Sheet is related to a subsidiary of Illini (i.e., a reporting unit). At the end of 20X1, there is no indication that it is more likely than not...

-

Bryan has recently taken out a $554,000, 30-year mortgage with a 5.31% APR. How much will Byran's required monthly payment be?

-

True Or False Contributory negligence prevents a negligent plaintiff from recovering unless the defendant is more negligent than the plaintiff.

-

True Or False Those states that have adopted comparative negligence have either abolished assumption of risk as a separate defense or have merged it into the defense of comparative negligence.

-

A doctor will not necessarily have to disclose a risk if a. the risk is highly improbable, and the doctor believes that disclosing it would severely reduce the effectiveness of the treatment. b. the...

-

In assessing a plaintiffs conduct who has allegedly assumed the risk, a(n) ____________ standard is used, whereas in assessing a plaintiffs conduct who was allegedly negligent, a(n) ____________...

-

What must be shown before a plaintiff will be considered to have impliedly assumed the risk?

-

1. In Question 1 of PS 1, you worked the details of the two policies that intended to help individuals in need. In particular, you presented reasons suggesting that cash transfers are always "at...

-

1. Below is depicted a graph G constructed by joining two opposite vertices of C12. Some authors call this a "theta graph" because it resembles the Greek letter 0. a. What is the total degree of this...

-

Honeybees accumulate charge as they fly, and they transfer charge to the flowers they visit. Honeybees are able to sense electric fields; tests show that they can detect a change in field as small as...

-

A platypus foraging for prey can detect an electric field as small as 0.002 N/C. To give an idea of the sensitivity of the platypuss electric sense, how far from a +10 nC point charge does the field...

-

A bumblebee can sense electric fields as the fields bend hairs on its body. Bumblebees have been conclusively shown to detect an electric field of 60 N/C. Could a bumblebee use this sense to detect...

Study smarter with the SolutionInn App