Question: Martin Technologies Inc., a large electronics company, is evaluating the possible acquisition of Columbia Electronics, a regional electronics company. Martin's analysts project the following post-merger

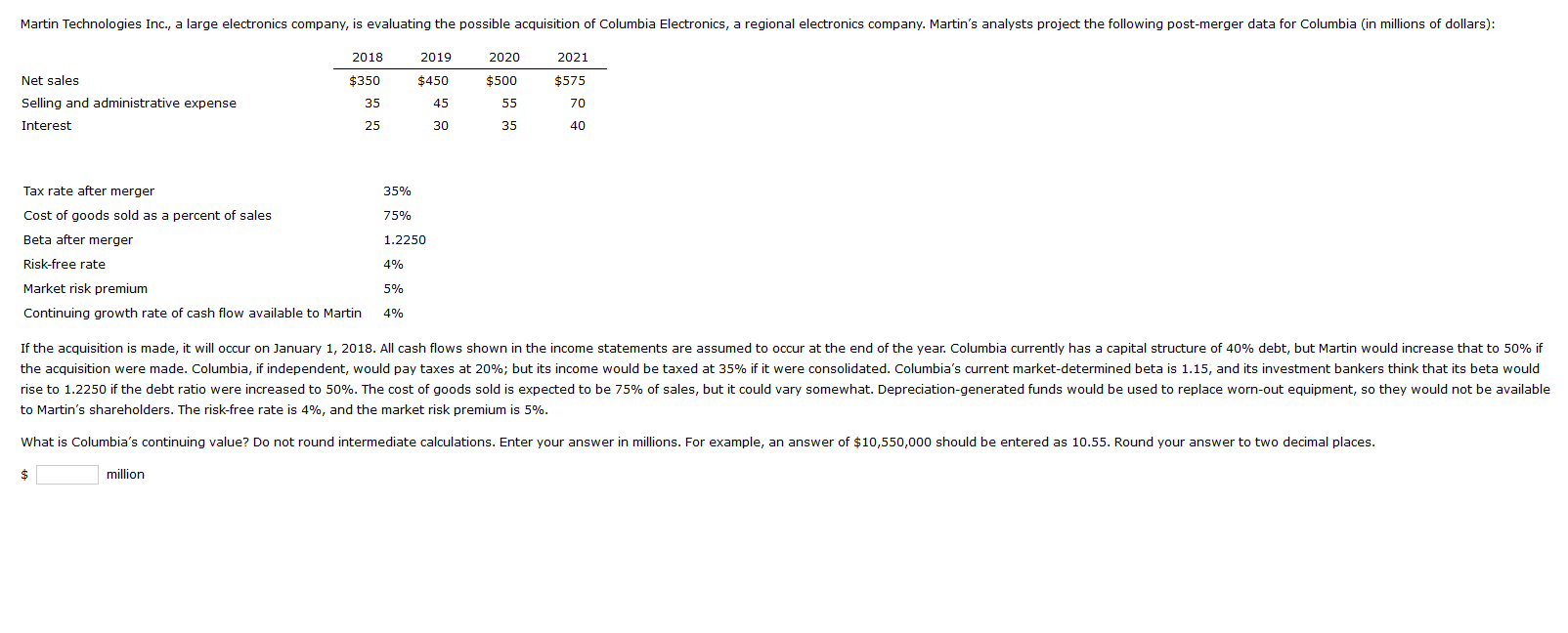

Martin Technologies Inc., a large electronics company, is evaluating the possible acquisition of Columbia Electronics, a regional electronics company. Martin's analysts project the following post-merger data for Columbia (in millions of dollars): 2018 2019 2020 2021 Net sales $350 $450 $500 $575 Selling and administrative expense 35 45 55 70 Interest 25 30 35 40 35% 75% 1.2250 Tax rate after merger Cost of goods sold as a percent of sales Beta after merger Risk-free rate Market risk premium Continuing growth rate of cash flow available to Martin 4% 5% 4% If the acquisition is made, it will occur on January 1, 2018. All cash flows shown in the income statements are assumed to occur at the end of the year. Columbia currently has a capital structure of 40% debt, but Martin would increase that to 50% if the acquisition were made. Columbia, if independent, would pay taxes at 20%; but its income would be taxed at 35% if it were consolidated. Columbia's current market-determined beta is 1.15, and its investment bankers think that its beta would rise to 1.2250 if the debt ratio were increased to 50%. The cost of goods sold is expected to be 75% of sales, but it could vary somewhat. Depreciation-generated funds would be used to replace worn-out equipment, so they would not be available to Martin's shareholders. The risk-free rate is 4%, and the market risk premium is 5%. What is Columbia's continuing value? Do not round intermediate calculations. Enter your answer in millions. For example, an answer of $10,550,000 should be entered as 10.55. Round your answer to two decimal places. million Martin Technologies Inc., a large electronics company, is evaluating the possible acquisition of Columbia Electronics, a regional electronics company. Martin's analysts project the following post-merger data for Columbia (in millions of dollars): 2018 2019 2020 2021 Net sales $350 $450 $500 $575 Selling and administrative expense 35 45 55 70 Interest 25 30 35 40 35% 75% 1.2250 Tax rate after merger Cost of goods sold as a percent of sales Beta after merger Risk-free rate Market risk premium Continuing growth rate of cash flow available to Martin 4% 5% 4% If the acquisition is made, it will occur on January 1, 2018. All cash flows shown in the income statements are assumed to occur at the end of the year. Columbia currently has a capital structure of 40% debt, but Martin would increase that to 50% if the acquisition were made. Columbia, if independent, would pay taxes at 20%; but its income would be taxed at 35% if it were consolidated. Columbia's current market-determined beta is 1.15, and its investment bankers think that its beta would rise to 1.2250 if the debt ratio were increased to 50%. The cost of goods sold is expected to be 75% of sales, but it could vary somewhat. Depreciation-generated funds would be used to replace worn-out equipment, so they would not be available to Martin's shareholders. The risk-free rate is 4%, and the market risk premium is 5%. What is Columbia's continuing value? Do not round intermediate calculations. Enter your answer in millions. For example, an answer of $10,550,000 should be entered as 10.55. Round your answer to two decimal places. million

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts