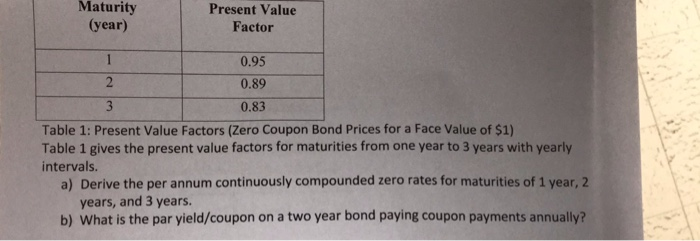

Question: Maturity Present Value Factor (year) 0.95 0.89 0.83 Table 1: Present Value Factors (Zero Coupon Bond Prices for a Face Value of $1) Table 1

Maturity Present Value Factor (year) 0.95 0.89 0.83 Table 1: Present Value Factors (Zero Coupon Bond Prices for a Face Value of $1) Table 1 gives the present value factors for maturities from one year to 3 years with yearly intervals a) Derive the per annum continuously compounded zero rates for maturities of 1 year, 2 years, and 3 years. b) What is the par yield/coupon on a two year bond paying coupon payments annually

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock