Question: May1. Paid rent for May $ 5000 Date Description post ref Debit Credit MAY 1. RENT EXPENSE A/C Dr 531 5000 To CASH A/C 110

| May1. Paid rent for May $ 5000 |

| Date | Description | post ref | Debit | Credit |

| MAY 1. | RENT EXPENSE A/C Dr | 531 | 5000 | |

| To CASH A/C | 110 | 5000 |

May 3.Purchased merchandise on account from Martin Co., terms 2/10, n/30, FOB shipping point, $36,000.

| Date | Description | post ref | Debit | Credit |

| MAY 3. | INVENTORY A/C Dr | 115 | 36000 | |

| To ACCOUNTS PAYABLE A/C | 210 | 36000 |

May 4: Paid freight on purchase of May 3, $600.

| Date | Description | post ref | Debit | Credit |

| MAY 4. | INVENTORY A/C Dr | 115 | 600 | |

| TO CASH A/C | 112 | 600 |

May 6: Sold merchandise on account to Korman Co., terms 2/10, n/30, FOB shipping point, $68,500. The cost of the goods sold was $41,000.

| Date | Description | post ref | Debit | Credit |

| MAY 6.-SALES | ACCOUNTS RECEIVABLE A/C Dr | 112 | 68500 | |

| TO SALES A/C | 410 | 68500 | ||

| MAY 6.-COST | COST OF GOODS SOLD A/C Dr | 510 | 41000 | |

| TO INVENTORY A/C | 115 | 41000 |

May 7: Received $22,300 cash from Halstad Co. on account.

| Date | Description | post ref | Debit | Credit |

| MAY 7 | CASH A/C Dr | 110 | 22300 | |

| TO ACCOUNTS RECEIVABLE A/C | 112 | 22300 |

May 10: Sold merchandise for cash, $54,000. The cost of the goods sold was $32,000.

| Date | Description | post ref | Debit | Credit |

| MAY 10-SALE | CASH A/C Dr | 110 | 54000 | |

| TO SALES A/C | 410 | 54000 | ||

| MAY 10-COST | COST OF GOODS SOLD A/C Dr | 510 | 32000 | |

| TO INVENTORY A/C | 115 | 32000 |

May 13: Paid for merchandise purchased on May 3.

| Date | Description | post ref | Debit | Credit |

| MAY.13 | ACCOUNTS PAYABLE A/C Dr | 210 | 360 | |

| DISCOUNT OF1% | TO INVENTORY A/C | 115 | 360 | |

| MAY 13-PAYMENT | ACCOUNTS PAYABLE A/C Dr | 210 | 35640 | |

| TO CASH A/C | 110 | 35640 |

May 15: Paid advertising expense for last half of May, $11,000.

| Date | Description | post ref | Debit | Credit |

| MAY 15 | ADVERTISING EXPENSE A/C Dr | 521 | 11000 | |

| TO CASH A/C | 110 | 11000 |

May 16: Received cash from sale of May 6.

| Date | Description | post ref | Debit | Credit |

| MAY .16 | CASH A/C Dr | 110 | 67130 | |

| SALES DISCOUNT A/C Dr | 1370 | |||

| TO ACCOUNTS RECEIVABLE A/C | 112 | 68500 | ||

| (2% SALE DISCOUNT) |

May 19: Purchased merchandise for cash, $18,700.

| Date | Description | post ref | Debit | Credit |

| MAY 19 | INVENTORY A/C Dr | 115 | 18700 | |

| TO CASH A/C | 110 | 18700 |

May 19: Paid $33,450 to Buttons Co. on account.

| Date | Description | post ref | Debit | Credit |

| MAY 19 | ACCOUNTS PAYABLE A/C Dr | 210 | 33450 | |

| TO CASH A/C | 110 | 33450 |

May 20: Paid Korman Co. a cash refund of $13,230 for returned merchandise from sale of May 6. The invoice amount of the returned merchandise was $13,500 and the cost of the returned merchandise was $8,000

| Date | Description | post ref | Debit | Credit |

| MAY 20-SALES | SALES RETURN A/C Dr | 13230 | ||

| TO CASH A/C | 110 | 13230 | ||

| MAY 20-COST | INVENTORY A/C Dr | 115 | 8000 | |

| TO COST OF GOODS SOLD A/C | 510 | 8000 |

May 20: Sold merchandise on account to Crescent Co., terms 1/10, n/30, FOB shipping point, $110,000. The cost of the goods sold was $70,000.

| Date | Description | post ref | Debit | Credit |

| MAY 20-SALE | ACCOUNTS RECEIVABLE A/C Dr | 112 | 110000 | |

| TO SALES A/C | 410 | 110000 | ||

| MAY 20-COST | COST OF GOOD SOLD A/C Dr | 510 | 70000 | |

| TO INVENTORY A/C | 115 | 70000 |

May 21: For the convenience of Crescent Co., paid freight on sale of May 20, $2,300.

| Date | Description | post ref | Debit | Credit |

| MAY 21 | ACCOUNTS RECEIVABLE A/C Dr | 112 | 2300 | |

| TO CASH A/C | 110 | 2300 |

FOR FREIGHT PAID BY THE SELLER(THE AMOUNT WILL BE TAKEN FROM THE PURCHASER AND HENCE ACCOUNTS RECEIVABLE IS DEBITED

May 21: Received $42,900 cash from Gee Co. on account.

| Date | Description | post ref | Debit | Credit |

| ,MAY 21 | CASH A/C Dr | 110 | 42900 | |

| TO ACCOUNTS RECEIVABLE A/C | 112 | 42900 |

May 21: Purchased merchandise on account from Osterman Co., terms 1/10, n/30, FOB destination, $88,000

| Date | Description | post ref | Debit | Credit |

| MAY 21 | INVENTORY A/C Dr | 115 | 88000 | |

| TO ACCOUNTS PAYABLE A/C | 210 | 88000 |

May 24: Returned damaged merchandise purchased on May 21, receiving a credit memo from the seller for $5,000.

| Date | Description | post ref | Debit | Credit |

| MAY 24 | ACCOUNTS PAYABLE A/C Dr | 210 | 5000 | |

| TO INVENTORY A/C | 115 | 5000 |

May 26: Refunded cash on sales made for cash, $7,500. The cost of the merchandise returned was $4,800.

| Date | Description | post ref | Debit | Credit |

| MAY 26-REFUND | SALES RETURNS A/C Dr | 7500 | ||

| TO CASH A/C | 110 | 7500 | ||

| MAY 26- COST | INVENTORY A/C Dr | 115 | 4800 | |

| TO COST OF GOODS SOLD A/C | 510 | 4800 |

May 28: Paid sales salaries of $56,000 and office salaries of $29,000

| Date | Description | post ref | Debit | Credit |

| MAY 28 | SALES SALARIES EXPENSE A/C Dr | 520 | 56000 | |

| OFFICE SALARIES EXPENSE A/C Dr | 530 | 29000 | ||

| TO CASH A/C | 110 | 85000 |

May 29: Purchased store supplies for cash, $2,400.

| Date | Description | post ref | Debit | Credit |

| MAY 29 | STORE SUPPLIES A/C | 118 | 2400 | |

| TO CASH A/C | 110 | 2400 |

May 30: Sold merchandise on account to Turner Co., terms 2/10, n/30, FOB shipping point, $78,750. The cost of the goods sold was $47,000.

| Date | Description | post ref | Debit | Credit |

| MAY 30-SALES | ACCOUNTS RECEIVABLE A/C Dr | 112 | 78750 | |

| TO SALES A/C | 410 | 78750 | ||

| MAY 30-COST | COST OF GOODS SOLD A/C Dr | 510 | 47000 | |

| TO INVENTORY A/C | 115 | 47000 |

May 30: Received cash from sale of May 20 plus freight paid on May 21.

| Date | Description | post ref | Debit | Credit |

| MAY 30 | CASH A/C Dr | 110 | 111200 | |

| SALES DISCOUNT A/C Dr | 1100 | |||

| TO ACCOUNTS RECEIVABLE A/C | 112 | 112300 |

1% DISCOUNT ON 110000

May 31: Paid for purchase of May 21, less return of May 24.

| Date | Description | post ref | Debit | Credit |

| MAY 31 | ACCOUNTS PAYABLE A/C Dr | 210 | 83000 | |

| TO CASH A/C | 110 | 83000 |

-

Prepare an unadjusted trial balance. If an amount box does not require an entry, leave it blank.

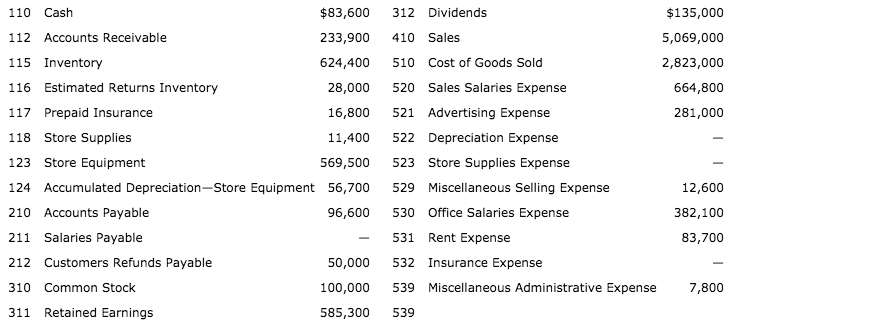

Palisade Creek Co. Unadjusted Trial Balance May 31, 20Y6 Debit Credit Cash Accounts Receivable Inventory Estimated Returns Inventory Prepaid Insurance Store Supplies Store Equipment Accumulated Depreciation-Store Equipment Accounts Payable Salaries Payable Customers Refunds Payable Common Stock Retained Earnings Dividends Sales Cost of Goods Sold Sales Salaries Expense Advertising Expense Depreciation Expense Store Supplies Expense Miscellaneous Selling Expense Office Salaries Expense Rent Expense Insurance Expense Miscellaneous Administrative Expense

110 Cash $83,600 312 Dividends $135,000 112 Accounts Receivable 233,900 410 Sales 5,069,000 115 Inventory 2,823,000 624,400 510 Cost of Goods Sold 116 Estimated Returns Inventory Sales Salaries Expense 28,000 520 664,800 521 Advertising Expense 117 Prepaid Insurance 16,800 281,000 118 Store Supplies 522 Depreciation Expense 11,400 123 Store Equipment 523 Store Supplies Expense 569,500 Miscellaneous Selling Expense 124 Accumulated Depreciation-Store Equipment 56,700 529 12,600 210 Accounts Payable Office Salaries Expense 382,100 96,600 530 Salaries Payable Rent Expense 211 531 83,700 212 Customers Refunds Payable 50,000 532 Insurance Expense Miscellaneous Administrative Expense 310 Common Stock 100,000 539 7,800 Retained Earnings 311 585,300 539

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts