Question: MBA 509 - Spring 2020 Case Study 2 - No Regrets Inc. (An independent case study to be prepared without assistance from any other individual).

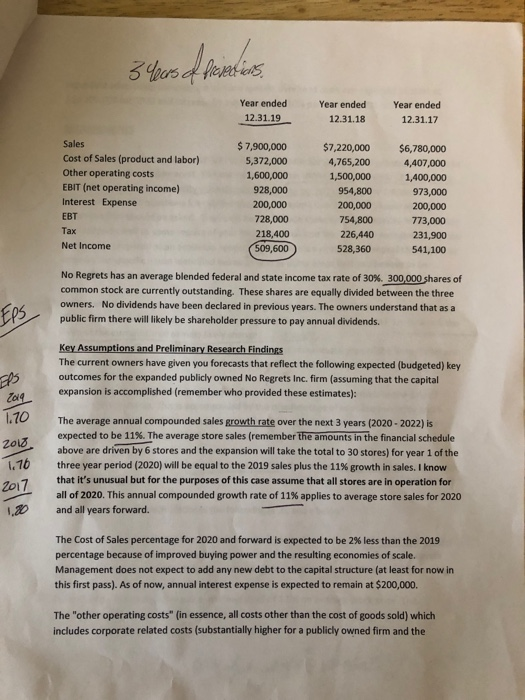

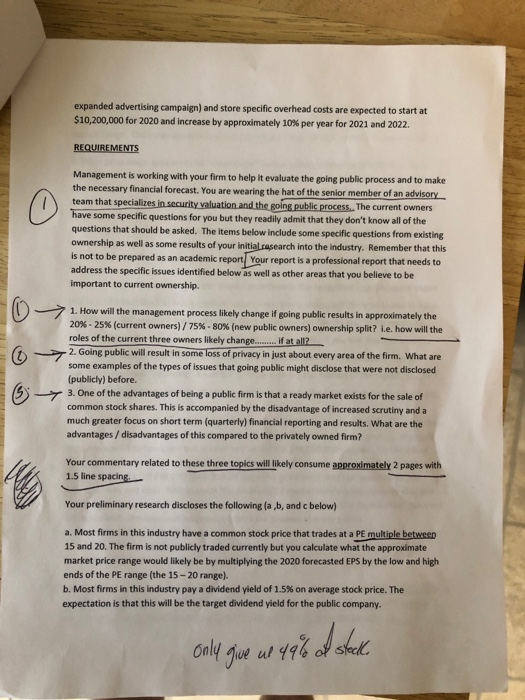

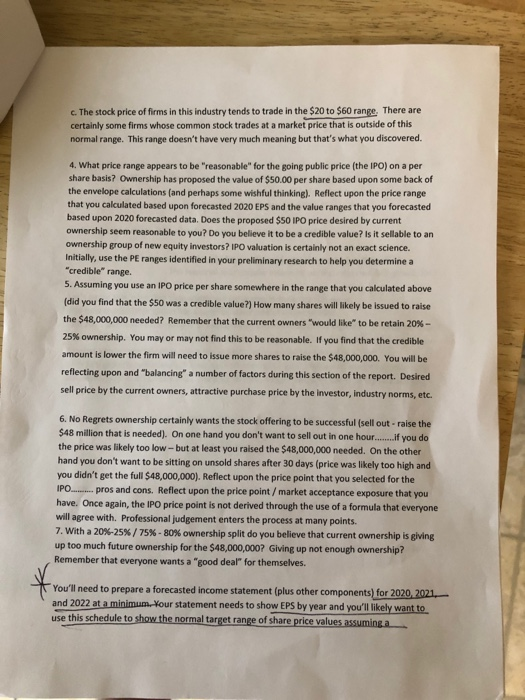

MBA 509 - Spring 2020 Case Study 2 - No Regrets Inc. (An independent case study to be prepared without assistance from any other individual). Please see the University Policy on Academic Honesty. This case includes a variety of areas where the student needs to make some "credible" assumptions driven by "ranges" of information. No two reports/ package of calculations will be complexly the same. You will likely want to review some content in chapter 18 in your text (or perhaps other sources) related to taking a company public to better understand the thought process behind IPO valuation. Key Topic Coverage - Security Valuation (PE multiple and Constant Growth Model approaches) (Note - Carry out any decimal calculations to 4 places) Public vs. Private Ownership Background- No Regrets, Inc. is a privately owned corporation that operates six specialty beverage / baked goods / light food fare "restaurants in the mid-Atlantic region of the U.S. The firm is investigating the possibility of taking the ownership of the corporation public and raising enough new equity capital, through the sale of common stock, to expand to approximately 30 locations over a five state region. No Regrets ownership estimates that the cost of expansion will be approximately $48 million. The existing three owners hope to retain a 20% - 25% ownership stake after the IPO. None of the existing owners have the cash available to make an additional equity investment at this time. This (the 20% - 25%) may or may not be reasonable but it is the current desire of existing ownership. The three owners have requested your input and reflection on a number of issues (The questions from the owners are identified at the end of the case. These are the minimum responses expected (The "C" grade content - you need to add to this list to provide answers to questions that the current owners should have asked but didn't know to ask). The schedule below highlights the firm's financial performance over the past three years. 3 Years of prevedions. Year ended 12.31.19 Year ended 12.31.18 Year ended 12.31.17 Sales Cost of Sales (product and labor) Other operating costs EBIT (net operating income) Interest Expense EBT Tax Net Income $ 7,900,000 5,372,000 1,600,000 928,000 200,000 728,000 218,400 509,600 $7,220,000 4,765,200 1,500,000 954,800 200,000 754,800 226,440 528,360 $6,780,000 4,407,000 1,400,000 973,000 200,000 773,000 231,900 541,100 No Regrets has an average blended federal and state income tax rate of 30% 300,000 shares of common stock are currently outstanding. These shares are equally divided between the three owners. No dividends have been declared in previous years. The owners understand that as a public firm there will likely be shareholder pressure to pay annual dividends. Key Assumptions and Preliminary Research Findings The current owners have given you forecasts that reflect the following expected (budgeted) key outcomes for the expanded publicly owned No Regrets Inc. firm (assuming that the capital expansion is accomplished (remember who provided these estimates): The average annual compounded sales growth rate over the next 3 years (2020-2022) is expected to be 11%. The average store sales (remember the amounts in the financial schedule above are driven by 6 stores and the expansion will take the total to 30 stores) for year 1 of the three year period (2020) will be equal to the 2019 sales plus the 11% growth in sales. I know that it's unusual but for the purposes of this case assume that all stores are in operation for all of 2020. This annual compounded growth rate of 11% applies to average store sales for 2020 and all years forward. The Cost of Sales percentage for 2020 and forward is expected to be 2% less than the 2019 percentage because of improved buying power and the resulting economies of scale Management does not expect to add any new debt to the capital structure (at least for now in this first pass). As of now, annual interest expense is expected to remain at $200,000 The "other operating costs" (in essence, all costs other than the cost of goods sold) which includes corporate related costs (substantially higher for a publicly owned firm and the expanded advertising campaign) and store specific overhead costs are expected to start at $10,200,000 for 2020 and increase by approximately 10% per year for 2021 and 2022 REQUIREMENTS Management is working with your firm to help it evaluate the going public process and to make the necessary financial forecast. You are wearing the hat of the senior member of an advisor team that specializes in security valuation and the going public process. The current owners have some specific questions for you but they readily admit that they don't know all of the questions that should be asked. The items below include some specific questions from existing ownership as well as some results of your initial research into the industry. Remember that this is not to be prepared as an academic report Your report is a professional report that needs to address the specific issues identified below as well as other areas that you believe to be important to current ownership. 7 1. How will the management process likely change if going public results in approximately the 20% - 25% (current owners)/75%-80% (new public owners) ownership split? i.e. how will the roles of the current three owners likely change......... If at all? 2. Going public will result in some loss of privacy in just about every area of the firm. What are some examples of the types of issues that going public might disclose that were not disclosed (publicly) before. 3. One of the advantages of being a public firm is that a ready market exists for the sale of common stock shares. This is accompanied by the disadvantage of increased scrutiny and a much greater focus on short term (quarterly) financial reporting and results. What are the advantages / disadvantages of this compared to the privately owned firm? 1673.00 Your commentary related to these three topics will likely consume approximately 2 pages with 1.5 line spacing Your preliminary research discloses the following (a,b, and below) a. Most firms in this industry have a common stock price that trades at a PE multiple between 15 and 20. The firm is not publicly traded currently but you calculate what the approximate market price range would likely be by multiplying the 2020 forecasted EPS by the low and high ends of the PE range (the 15-20 range) b. Most firms in this industry pay a dividend yield of 1.5% on average stock price. The expectation is that this will be the target dividend yield for the public company. only give ue 49% od stack C. The stock price of firms in this industry tends to trade in the $20 to $60 range. There are certainly some firms whose common stock trades at a market price that is outside of this normal range. This range doesn't have very much meaning but that's what you discovered 4. What price range appears to be "reasonable" for the going public price (the IPO) on a per share basis? Ownership has proposed the value of $50.00 per share based upon some back of the envelope calculations (and perhaps some wishful thinking). Reflect upon the price range that you calculated based upon forecasted 2020 EPS and the value ranges that you forecasted based upon 2020 forecasted data. Does the proposed $SO IPO price desired by current ownership seem reasonable to you? Do you believe it to be a credible value? Is it sellable to an ownership group of new equity investors? IPO valuation is certainly not an exact science Initially, use the PE ranges identified in your preliminary research to help you determine a "credible range 5. Assuming you use an IPO price per share somewhere in the range that you calculated above (did you find that the $50 was a credible value?) How many shares will likely be issued to raise the $48,000,000 needed? Remember that the current owners would like to be retain 20%- 25% ownership. You may or may not find this to be reasonable. If you find that the credible amount is lower the firm will need to issue more shares to raise the $48,000,000. You will be reflecting upon and "balancing a number of factors during this section of the report. Desired sell price by the current owners, attractive purchase price by the investor, industry norms, etc. 6. No Regrets ownership certainly wants the stock offering to be successful (sell out raise the $48 million that is needed). On one hand you don't want to sell out in one hour...if you do the price was likely too low-but at least you raised the $48,000,000 needed. On the other hand you don't want to be sitting on unsold shares after 30 days (price was likely too high and you didn't get the full $48,000,000). Reflect upon the price point that you selected for the IPO._... pros and cons. Reflect upon the price point/market acceptance exposure that you have. Once again, the IPO price point is not derived through the use of a formula that everyone will agree with. Professional judgement enters the process at many points. 7. With a 20%-25%/75%-80% ownership split do you believe that current ownership is giving up too much future ownership for the $48,000,000? Giving up not enough ownership? Remember that everyone wants a "good dear for themselves. You'll need to prepare a forecasted income statement (plus other components) for 2020 2021 and 2022 at a minimum. Your statement needs to show EPS by year and you'll likely want to use this schedule to show the normal target range of share price values assuminga continuation of a PE range of 15 on the low end and 20 on the high end. Always remember that these values are not absolutes. The 15 and 20 low and high PE range represents a normal range but sure not an absolute range. Once again, there is no exact science here. Your initial common stock share price estimating was based upon using the historical norms for a high and low PE range. To take a broader view (the MBA view) you decide to use your forecasted information from above, make some additional estimates, and use the Constant Growth Model approach to common stock share price valuation. The Constant Growth Valuation Formula is usually written as follows: The target market price today = the dividend to be paid over the next 12 months (D1) The required shareholder return minus the expected EPS growth rate Let's agree that your first pass additional estimates include the following: The new shareholder group has a target annual rate of return of 20% The 2021 per share dividend (D1 in the constant growth formula) is expected to be 85 cents per share. Let's all use 85 cents as a starting point. How does the $.85 per share dividend compare to what you would calculate using the industry average dividend yield of 1.5%? Your EPS growth rate moving forward is determined by your forecast of the EPS growth rate between 2020 and let's say 2022. Be sure to reflect upon absolute values and the emerging trend. Reflect upon what the Constant Growth Valuation Model is telling you compared to what the use of the normal PE range is telling you. Are the calculated valuations in the same general value range area or do you see a wide variation. The owners await your very well rounded......in depth report. This needs to be an example of your very best work. The full package, including all exhibits is likely to be approximately 7 pages with 1.5 line spacing. Use your MBA level talent to make any assumptions that you need to make. Justify the key assumptions that you do make. MBA 509 - Spring 2020 Case Study 2 - No Regrets Inc. (An independent case study to be prepared without assistance from any other individual). Please see the University Policy on Academic Honesty. This case includes a variety of areas where the student needs to make some "credible" assumptions driven by "ranges" of information. No two reports/ package of calculations will be complexly the same. You will likely want to review some content in chapter 18 in your text (or perhaps other sources) related to taking a company public to better understand the thought process behind IPO valuation. Key Topic Coverage - Security Valuation (PE multiple and Constant Growth Model approaches) (Note - Carry out any decimal calculations to 4 places) Public vs. Private Ownership Background- No Regrets, Inc. is a privately owned corporation that operates six specialty beverage / baked goods / light food fare "restaurants in the mid-Atlantic region of the U.S. The firm is investigating the possibility of taking the ownership of the corporation public and raising enough new equity capital, through the sale of common stock, to expand to approximately 30 locations over a five state region. No Regrets ownership estimates that the cost of expansion will be approximately $48 million. The existing three owners hope to retain a 20% - 25% ownership stake after the IPO. None of the existing owners have the cash available to make an additional equity investment at this time. This (the 20% - 25%) may or may not be reasonable but it is the current desire of existing ownership. The three owners have requested your input and reflection on a number of issues (The questions from the owners are identified at the end of the case. These are the minimum responses expected (The "C" grade content - you need to add to this list to provide answers to questions that the current owners should have asked but didn't know to ask). The schedule below highlights the firm's financial performance over the past three years. 3 Years of prevedions. Year ended 12.31.19 Year ended 12.31.18 Year ended 12.31.17 Sales Cost of Sales (product and labor) Other operating costs EBIT (net operating income) Interest Expense EBT Tax Net Income $ 7,900,000 5,372,000 1,600,000 928,000 200,000 728,000 218,400 509,600 $7,220,000 4,765,200 1,500,000 954,800 200,000 754,800 226,440 528,360 $6,780,000 4,407,000 1,400,000 973,000 200,000 773,000 231,900 541,100 No Regrets has an average blended federal and state income tax rate of 30% 300,000 shares of common stock are currently outstanding. These shares are equally divided between the three owners. No dividends have been declared in previous years. The owners understand that as a public firm there will likely be shareholder pressure to pay annual dividends. Key Assumptions and Preliminary Research Findings The current owners have given you forecasts that reflect the following expected (budgeted) key outcomes for the expanded publicly owned No Regrets Inc. firm (assuming that the capital expansion is accomplished (remember who provided these estimates): The average annual compounded sales growth rate over the next 3 years (2020-2022) is expected to be 11%. The average store sales (remember the amounts in the financial schedule above are driven by 6 stores and the expansion will take the total to 30 stores) for year 1 of the three year period (2020) will be equal to the 2019 sales plus the 11% growth in sales. I know that it's unusual but for the purposes of this case assume that all stores are in operation for all of 2020. This annual compounded growth rate of 11% applies to average store sales for 2020 and all years forward. The Cost of Sales percentage for 2020 and forward is expected to be 2% less than the 2019 percentage because of improved buying power and the resulting economies of scale Management does not expect to add any new debt to the capital structure (at least for now in this first pass). As of now, annual interest expense is expected to remain at $200,000 The "other operating costs" (in essence, all costs other than the cost of goods sold) which includes corporate related costs (substantially higher for a publicly owned firm and the expanded advertising campaign) and store specific overhead costs are expected to start at $10,200,000 for 2020 and increase by approximately 10% per year for 2021 and 2022 REQUIREMENTS Management is working with your firm to help it evaluate the going public process and to make the necessary financial forecast. You are wearing the hat of the senior member of an advisor team that specializes in security valuation and the going public process. The current owners have some specific questions for you but they readily admit that they don't know all of the questions that should be asked. The items below include some specific questions from existing ownership as well as some results of your initial research into the industry. Remember that this is not to be prepared as an academic report Your report is a professional report that needs to address the specific issues identified below as well as other areas that you believe to be important to current ownership. 7 1. How will the management process likely change if going public results in approximately the 20% - 25% (current owners)/75%-80% (new public owners) ownership split? i.e. how will the roles of the current three owners likely change......... If at all? 2. Going public will result in some loss of privacy in just about every area of the firm. What are some examples of the types of issues that going public might disclose that were not disclosed (publicly) before. 3. One of the advantages of being a public firm is that a ready market exists for the sale of common stock shares. This is accompanied by the disadvantage of increased scrutiny and a much greater focus on short term (quarterly) financial reporting and results. What are the advantages / disadvantages of this compared to the privately owned firm? 1673.00 Your commentary related to these three topics will likely consume approximately 2 pages with 1.5 line spacing Your preliminary research discloses the following (a,b, and below) a. Most firms in this industry have a common stock price that trades at a PE multiple between 15 and 20. The firm is not publicly traded currently but you calculate what the approximate market price range would likely be by multiplying the 2020 forecasted EPS by the low and high ends of the PE range (the 15-20 range) b. Most firms in this industry pay a dividend yield of 1.5% on average stock price. The expectation is that this will be the target dividend yield for the public company. only give ue 49% od stack C. The stock price of firms in this industry tends to trade in the $20 to $60 range. There are certainly some firms whose common stock trades at a market price that is outside of this normal range. This range doesn't have very much meaning but that's what you discovered 4. What price range appears to be "reasonable" for the going public price (the IPO) on a per share basis? Ownership has proposed the value of $50.00 per share based upon some back of the envelope calculations (and perhaps some wishful thinking). Reflect upon the price range that you calculated based upon forecasted 2020 EPS and the value ranges that you forecasted based upon 2020 forecasted data. Does the proposed $SO IPO price desired by current ownership seem reasonable to you? Do you believe it to be a credible value? Is it sellable to an ownership group of new equity investors? IPO valuation is certainly not an exact science Initially, use the PE ranges identified in your preliminary research to help you determine a "credible range 5. Assuming you use an IPO price per share somewhere in the range that you calculated above (did you find that the $50 was a credible value?) How many shares will likely be issued to raise the $48,000,000 needed? Remember that the current owners would like to be retain 20%- 25% ownership. You may or may not find this to be reasonable. If you find that the credible amount is lower the firm will need to issue more shares to raise the $48,000,000. You will be reflecting upon and "balancing a number of factors during this section of the report. Desired sell price by the current owners, attractive purchase price by the investor, industry norms, etc. 6. No Regrets ownership certainly wants the stock offering to be successful (sell out raise the $48 million that is needed). On one hand you don't want to sell out in one hour...if you do the price was likely too low-but at least you raised the $48,000,000 needed. On the other hand you don't want to be sitting on unsold shares after 30 days (price was likely too high and you didn't get the full $48,000,000). Reflect upon the price point that you selected for the IPO._... pros and cons. Reflect upon the price point/market acceptance exposure that you have. Once again, the IPO price point is not derived through the use of a formula that everyone will agree with. Professional judgement enters the process at many points. 7. With a 20%-25%/75%-80% ownership split do you believe that current ownership is giving up too much future ownership for the $48,000,000? Giving up not enough ownership? Remember that everyone wants a "good dear for themselves. You'll need to prepare a forecasted income statement (plus other components) for 2020 2021 and 2022 at a minimum. Your statement needs to show EPS by year and you'll likely want to use this schedule to show the normal target range of share price values assuminga continuation of a PE range of 15 on the low end and 20 on the high end. Always remember that these values are not absolutes. The 15 and 20 low and high PE range represents a normal range but sure not an absolute range. Once again, there is no exact science here. Your initial common stock share price estimating was based upon using the historical norms for a high and low PE range. To take a broader view (the MBA view) you decide to use your forecasted information from above, make some additional estimates, and use the Constant Growth Model approach to common stock share price valuation. The Constant Growth Valuation Formula is usually written as follows: The target market price today = the dividend to be paid over the next 12 months (D1) The required shareholder return minus the expected EPS growth rate Let's agree that your first pass additional estimates include the following: The new shareholder group has a target annual rate of return of 20% The 2021 per share dividend (D1 in the constant growth formula) is expected to be 85 cents per share. Let's all use 85 cents as a starting point. How does the $.85 per share dividend compare to what you would calculate using the industry average dividend yield of 1.5%? Your EPS growth rate moving forward is determined by your forecast of the EPS growth rate between 2020 and let's say 2022. Be sure to reflect upon absolute values and the emerging trend. Reflect upon what the Constant Growth Valuation Model is telling you compared to what the use of the normal PE range is telling you. Are the calculated valuations in the same general value range area or do you see a wide variation. The owners await your very well rounded......in depth report. This needs to be an example of your very best work. The full package, including all exhibits is likely to be approximately 7 pages with 1.5 line spacing. Use your MBA level talent to make any assumptions that you need to make. Justify the key assumptions that you do make

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts