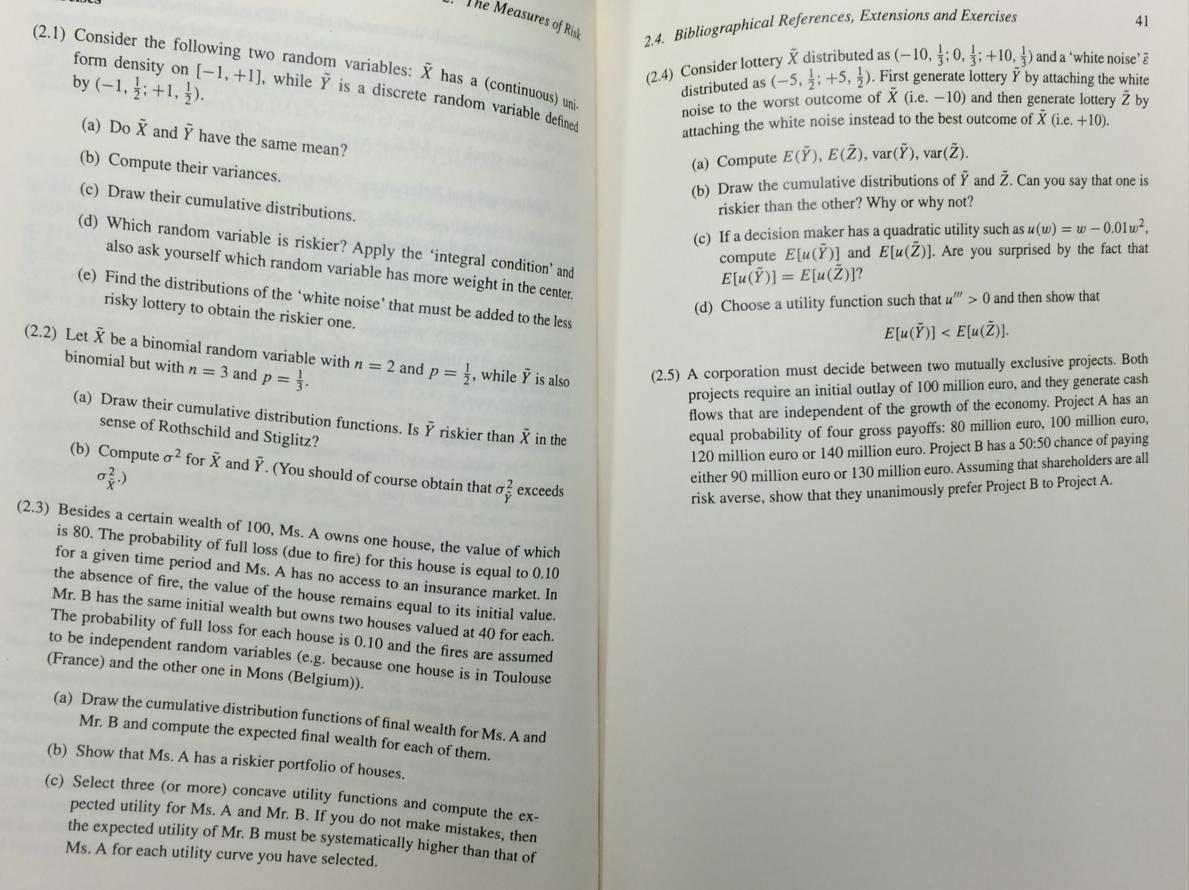

Measures of Risk (2.1) Consider the following two random variables: X has a (continuous) uni- form...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

John E Freunds Mathematical Statistics With Applications

ISBN: 9780134995373

8th Edition

Authors: Irwin Miller, Marylees Miller

Posted Date: