Mesmerizing Marketers (MM) is a marketing company that offers a variety of marketing offerings to its...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

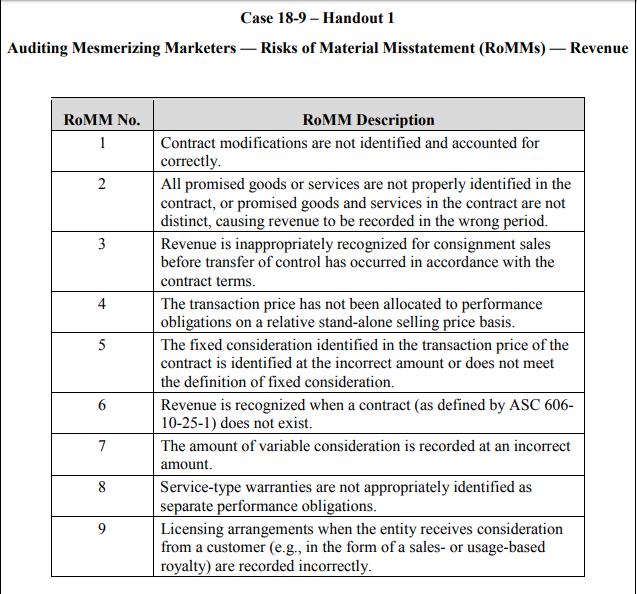

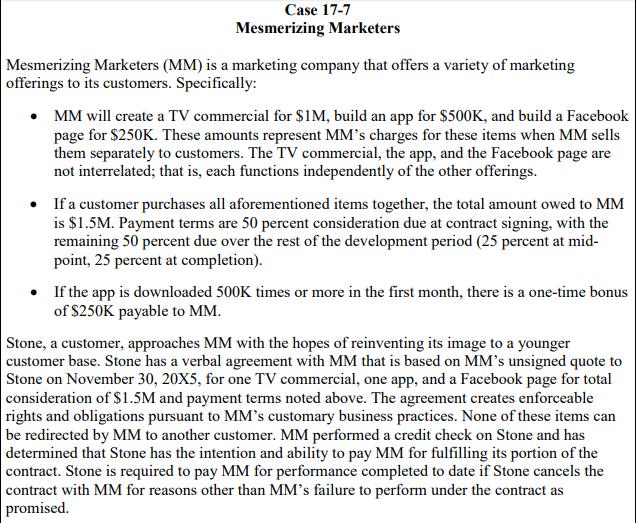

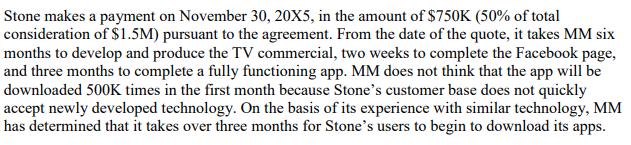

Mesmerizing Marketers (MM) is a marketing company that offers a variety of marketing offerings to its customers, including TV commercial production, app construction, and Facebook page creation. MM accounts for its revenue in accordance with ASC 606, Revenue From Contracts With Customers. As part of our audit procedures, we need to understand the accounting for an account balance before we begin auditing that balance. Therefore, this case assumes you have read and understood MM's marketing services and the accounting of such services, which are presented in Case 17-7 (available on the Trueblood Case Study Series website). Note that you have been provided with Handout 1, which contains the risks of material misstatement matrix, and Handout 2, which is MM's control matrix. Required Activities: 1. Read Case 17-7, Mesmerizing Marketers. On the basis of the facts stated therein related to the contract between MM and Stone, a customer, what are some risks of material misstatement (ROMMS) that we may identify as part of our audit? Handout 1, the ROMMS matrix, may be used to assist with identifying relevant ROMMS. 2. Tailoring ROMMS to the specific revenue streams and assertions is an important step in designing an audit plan for revenue. Now that you have identified the ROMMS that are applicable to the contract between MM and Stone, how might you tailor the ROMMS that you identified in Activity 1 to the facts presented in this case? Case 18-9 – Handout 1 Auditing Mesmerizing Marketers – Risks of Material Misstatement (ROMMS) – Revenue ROMM No. ROMM Description 1 Contract modifications are not identified and accounted for correctly. All promised goods or services are not properly identified in the contract, or promised goods and services in the contract are not distinct, causing revenue to be recorded in the wrong period. 2 3 Revenue is inappropriately recognized for consignment sales before transfer of control has occurred in accordance with the contract terms. 4 The transaction price has not been allocated to performance obligations on a relative stand-alone selling price basis. The fixed consideration identified in the transaction price of the contract is identified at the incorrect amount or does not meet 5 the definition of fixed consideration. Revenue is recognized when a contract (as defined by ASC 606- 10-25-1) does not exist. 7 The amount of variable consideration is recorded at an incorrect amount. 8 Service-type warranties are not appropriately identified as separate performance obligations. Licensing arrangements when the entity receives consideration from a customer (e.g., in the form of a sales- or usage-based royalty) are recorded incorrectly. Case 17-7 Mesmerizing Marketers Mesmerizing Marketers (MM) is a marketing company that offers a variety of marketing offerings to its customers. Specifically: • MM will create a TV commercial for $1M, build an app for $500K, and build a Facebook page for $250K. These amounts represent MM's charges for these items when MM sells them separately to customers. The TV commercial, the app, and the Facebook page are not interrelated; that is, each functions independently of the other offerings. • If a customer purchases all aforementioned items together, the total amount owed to MM is $1.5M. Payment terms are 50 percent consideration due at contract signing, with the remaining 50 percent due over the rest of the development period (25 percent at mid- point, 25 percent at completion). • If the app is downloaded 500K times or more in the first month, there is a one-time bonus of $250K payable to MM. Stone, a customer, approaches MM with the hopes of reinventing its image to a younger customer base. Stone has a verbal agreement with MM that is based on MM's unsigned quote to Stone on November 30, 20X5, for one TV commercial, one app, and a Facebook page for total consideration of $1.5M and payment terms noted above. The agreement creates enforceable rights and obligations pursuant to MM's customary business practices. None of these items can be redirected by MM to another customer. MM performed a credit check on Stone and has determined that Stone has the intention and ability to pay MM for fulfilling its portion of the contract. Stone is required to pay MM for performance completed to date if Stone cancels the contract with MM for reasons other than MM's failure to perform under the contract as promised. Stone makes a payment on November 30, 20X5, in the amount of $750K (50% of total consideration of $1.5M) pursuant to the agreement. From the date of the quote, it takes MM six months to develop and produce the TV commercial, two weeks to complete the Facebook page, and three months to complete a fully functioning app. MM does not think that the app will be downloaded 500K times in the first month because Stone's customer base does not quickly accept newly developed technology. On the basis of its experience with similar technology, MM has determined that it takes over three months for Stone's users to begin to download its apps. Mesmerizing Marketers (MM) is a marketing company that offers a variety of marketing offerings to its customers, including TV commercial production, app construction, and Facebook page creation. MM accounts for its revenue in accordance with ASC 606, Revenue From Contracts With Customers. As part of our audit procedures, we need to understand the accounting for an account balance before we begin auditing that balance. Therefore, this case assumes you have read and understood MM's marketing services and the accounting of such services, which are presented in Case 17-7 (available on the Trueblood Case Study Series website). Note that you have been provided with Handout 1, which contains the risks of material misstatement matrix, and Handout 2, which is MM's control matrix. Required Activities: 1. Read Case 17-7, Mesmerizing Marketers. On the basis of the facts stated therein related to the contract between MM and Stone, a customer, what are some risks of material misstatement (ROMMS) that we may identify as part of our audit? Handout 1, the ROMMS matrix, may be used to assist with identifying relevant ROMMS. 2. Tailoring ROMMS to the specific revenue streams and assertions is an important step in designing an audit plan for revenue. Now that you have identified the ROMMS that are applicable to the contract between MM and Stone, how might you tailor the ROMMS that you identified in Activity 1 to the facts presented in this case? Case 18-9 – Handout 1 Auditing Mesmerizing Marketers – Risks of Material Misstatement (ROMMS) – Revenue ROMM No. ROMM Description 1 Contract modifications are not identified and accounted for correctly. All promised goods or services are not properly identified in the contract, or promised goods and services in the contract are not distinct, causing revenue to be recorded in the wrong period. 2 3 Revenue is inappropriately recognized for consignment sales before transfer of control has occurred in accordance with the contract terms. 4 The transaction price has not been allocated to performance obligations on a relative stand-alone selling price basis. The fixed consideration identified in the transaction price of the contract is identified at the incorrect amount or does not meet 5 the definition of fixed consideration. Revenue is recognized when a contract (as defined by ASC 606- 10-25-1) does not exist. 7 The amount of variable consideration is recorded at an incorrect amount. 8 Service-type warranties are not appropriately identified as separate performance obligations. Licensing arrangements when the entity receives consideration from a customer (e.g., in the form of a sales- or usage-based royalty) are recorded incorrectly. Case 17-7 Mesmerizing Marketers Mesmerizing Marketers (MM) is a marketing company that offers a variety of marketing offerings to its customers. Specifically: • MM will create a TV commercial for $1M, build an app for $500K, and build a Facebook page for $250K. These amounts represent MM's charges for these items when MM sells them separately to customers. The TV commercial, the app, and the Facebook page are not interrelated; that is, each functions independently of the other offerings. • If a customer purchases all aforementioned items together, the total amount owed to MM is $1.5M. Payment terms are 50 percent consideration due at contract signing, with the remaining 50 percent due over the rest of the development period (25 percent at mid- point, 25 percent at completion). • If the app is downloaded 500K times or more in the first month, there is a one-time bonus of $250K payable to MM. Stone, a customer, approaches MM with the hopes of reinventing its image to a younger customer base. Stone has a verbal agreement with MM that is based on MM's unsigned quote to Stone on November 30, 20X5, for one TV commercial, one app, and a Facebook page for total consideration of $1.5M and payment terms noted above. The agreement creates enforceable rights and obligations pursuant to MM's customary business practices. None of these items can be redirected by MM to another customer. MM performed a credit check on Stone and has determined that Stone has the intention and ability to pay MM for fulfilling its portion of the contract. Stone is required to pay MM for performance completed to date if Stone cancels the contract with MM for reasons other than MM's failure to perform under the contract as promised. Stone makes a payment on November 30, 20X5, in the amount of $750K (50% of total consideration of $1.5M) pursuant to the agreement. From the date of the quote, it takes MM six months to develop and produce the TV commercial, two weeks to complete the Facebook page, and three months to complete a fully functioning app. MM does not think that the app will be downloaded 500K times in the first month because Stone's customer base does not quickly accept newly developed technology. On the basis of its experience with similar technology, MM has determined that it takes over three months for Stone's users to begin to download its apps.

Expert Answer:

Answer rating: 100% (QA)

Auditing Mesmerizing Markets MM Risk of material misstatement RoMM Contract between MM and Stone Sr No RoMM Revenue As Per Handout 1 RoMM Tailored to facts of the case Assertion Addressed 1 Contract m... View the full answer

Posted Date:

Students also viewed these accounting questions

-

Mesmerizing Marketers (MM) is a marketing company that offers a variety of marketing offerings to its customers. Specifically: MM will create a TV commercial for $1M, build an app for $500K, and...

-

What advice would you have for a marketing company that is considering the use of avatars (animated people-like images) on their website? Lead this exercise in the context of trying to help consumers...

-

Stone Pest Control offers extermination services to customers in various arrangements and packages. For example, a customer could call Stone as needed to come out and spray for insects; for this...

-

Your company, Printers Inc., is considering investing in a new plant to manufacture a new generation of 3D printers developed by the firms research and development (R&D) department. A consulting...

-

Refer to the previous exercise. The output shows the result of comparing the mean responses on parties and sports. Paired T for parties - sports Difference 10 12.8000 22.5477 7.1302 95% CI for mean...

-

1. How successful was this project? 2. What best practices were evident in the case? How did they contribute to project objectives? Chad Cromwell, head of university housing, gazed up at the tower at...

-

(a) As the electric motor shown schematically in Figure P28.30 operates, which of the arrows shown could represent the magnetic dipole moment at various instants? (b) If there are any arrows that are...

-

Classic Theater is in the Greenbelt Mall. A cashiers booth is located near the entrance to the theater. Two cashiers are employed. One works from 1:00 to 5:00 P.M., the other from 5:00 to 9:00 P.M....

-

The formula of a compound is Y3(PO4)2. The electronic configuration of the atom of Y is 15. A. 2.8.2 B. 2.8.3 C 2.8.4 16. D. 2.8.5 The atomic numbers and mass numbers of atoms, W, X, Y and Z are...

-

In this exercise you will be assuming the role of an Account Manager working within our Personal Care Appliances category during Amazon Black Friday. You act as a general manager responsible for...

-

A car is being tested on a circular track having a radius of 5 0 0 m . At the moment the car's velocity is directed north, the car's acceleration is directed west and has a magnitude of 5 m / s ....

-

3. What is the momentum of a car with a mass of 1,300 kg traveling north at a speed of 28 m/s? 4. A baseball has a momentum of 6.0 kgm/s south and a mass of 0.15 kg. What is the baseball's velocity?

-

Which statement correctly describes the electric force, electric field, electric potential energy, and electric potential difference? (a) the field and potential energy are intrinsic, force and...

-

Air in a 138-km/h wind strikes head-on the face of a building 45 m wide by 73 m high and is brought to rest. if air has a mass of 1.3 kg per cubic meter, determine the average force of the wind on...

-

The Board of Directors of KE Ltd. manufacturers of three products A, B and C have asked for advice on the production mixture of the company. (a) You are required to present a statement to advice the...

-

A popular podcast interviews an average of 5 guests every 90 minutes. Using a Poisson distribution, what is the probability that the podcast interviews less than 3 guests in a 90-minute time...

-

Assume you live in the U.S. and have only U.S dollars. You are building a house in Mexico. Every month, you have to take dollars out of your bank account, convert them to pesos and send the money to...

-

Splitting hairs, if you shine a beam of colored light to a friend above in a high tower, will the color of light your friend receives be the same color you send? Explain.

-

Define effective listening .

-

Explain four strategies for improving listening skills.

-

Define the following factors and explain how they affect listening: body factors, voice factors, proximity factors.

Study smarter with the SolutionInn App