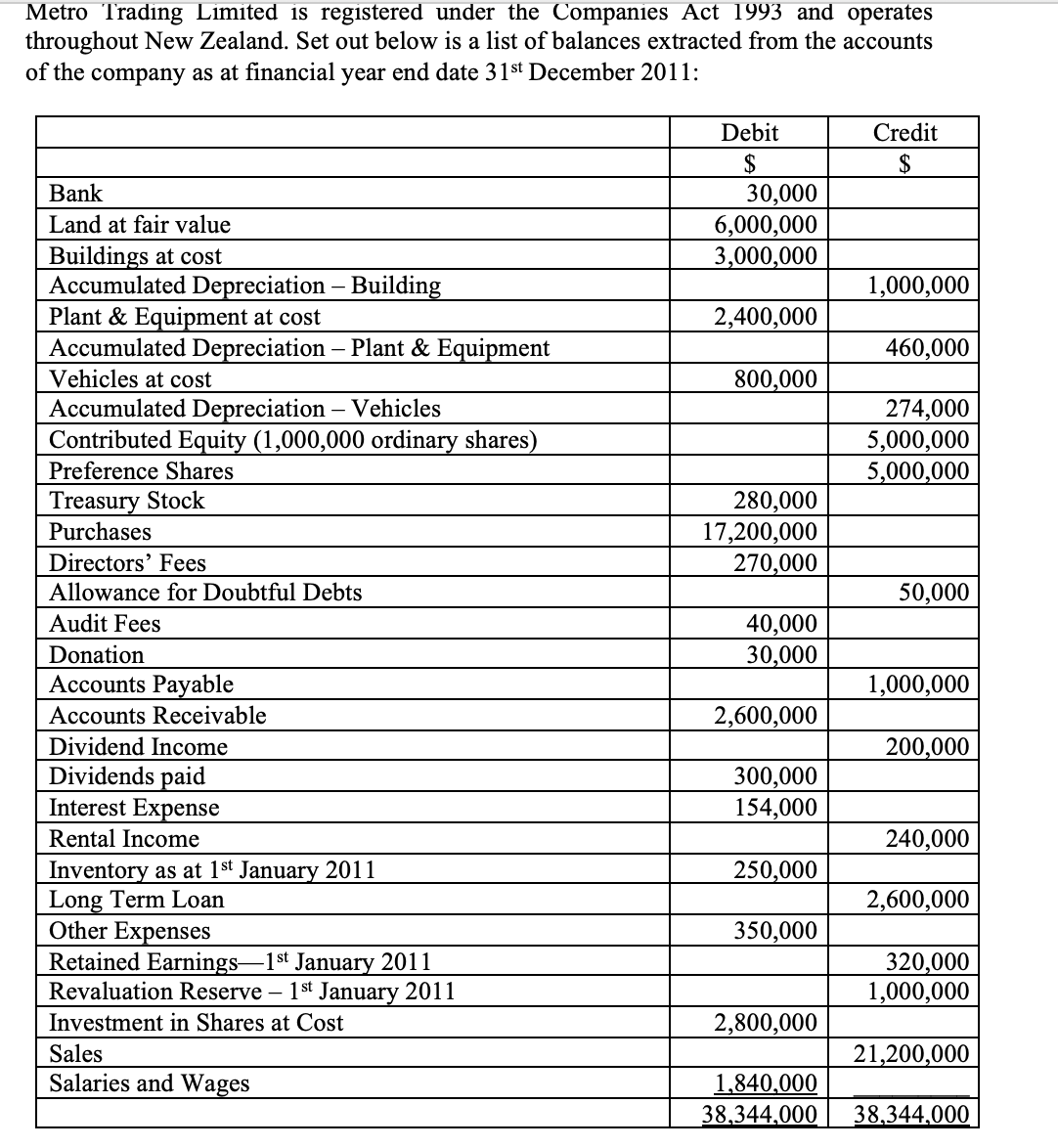

Metro Trading Limited is registered under the Companies Act 1993 and operates throughout New Zealand. Set...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

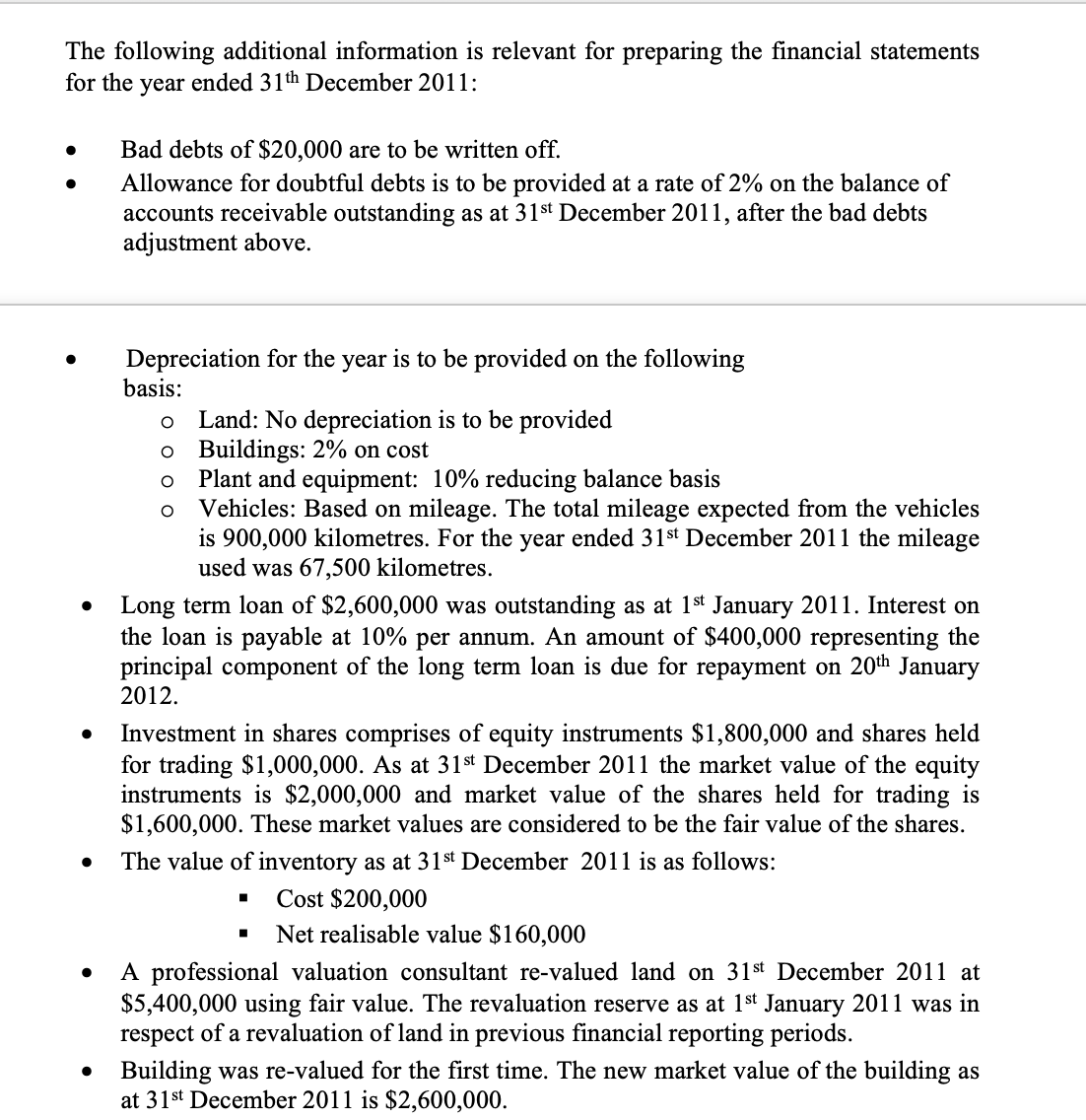

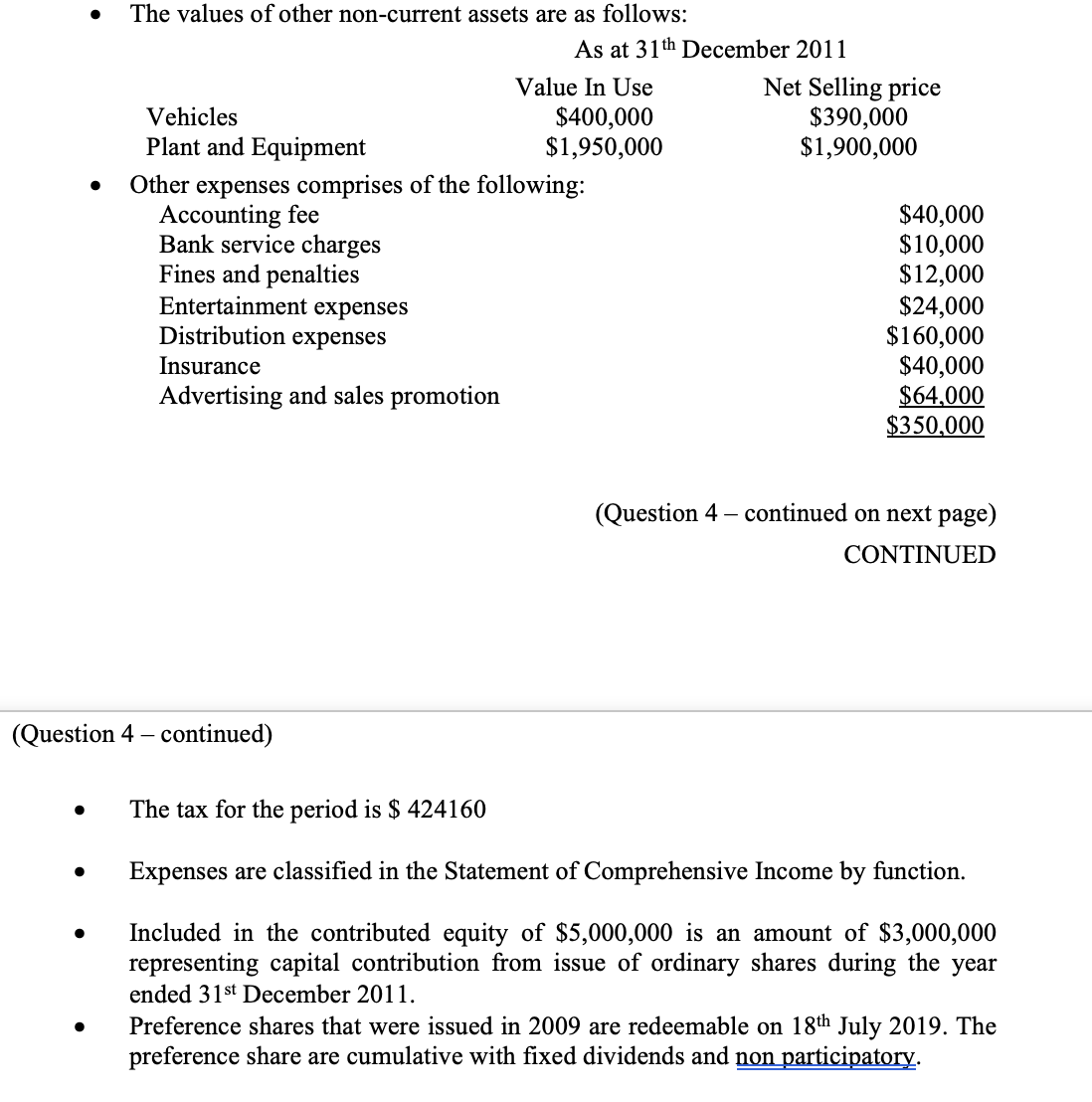

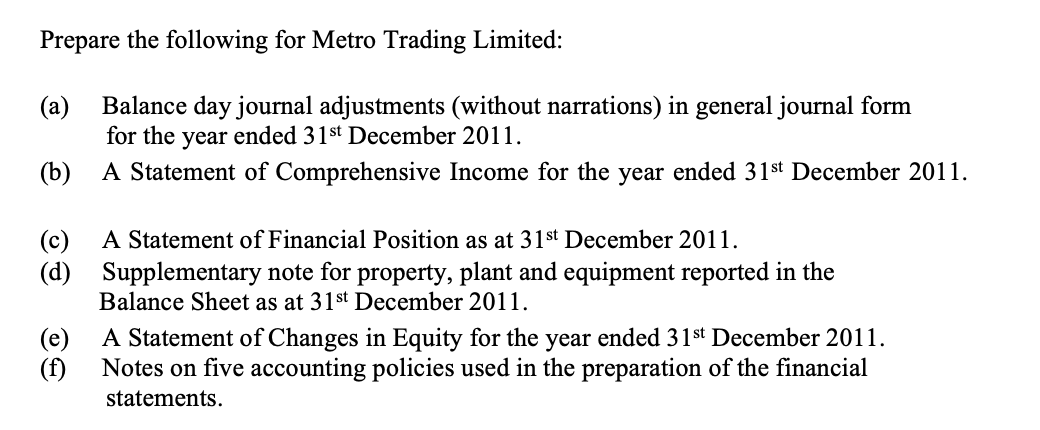

Metro Trading Limited is registered under the Companies Act 1993 and operates throughout New Zealand. Set out below is a list of balances extracted from the accounts of the company as at financial year end date 31st December 2011: Bank Land at fair value Buildings at cost Accumulated Depreciation - Building Plant & Equipment at cost Accumulated Depreciation - Plant & Equipment Vehicles at cost Accumulated Depreciation - Vehicles Contributed Equity (1,000,000 ordinary shares) Preference Shares Treasury Stock Purchases Directors' Fees Allowance for Doubtful Debts Audit Fees Donation Accounts Payable Accounts Receivable Dividend Income Dividends paid Interest Expense Rental Income Inventory as at 1st January 2011 Long Term Loan Other Expenses Retained Earnings1st January 2011 Revaluation Reserve - 1st January 2011 Investment in Shares at Cost Sales Salaries and Wages Debit $ 30,000 6,000,000 3,000,000 2,400,000 800,000 280,000 17,200,000 270,000 40,000 30,000 2,600,000 300,000 154,000 250,000 350,000 2,800,000 Credit $ 1,000,000 460,000 274,000 5,000,000 5,000,000 50,000 1,000,000 200,000 240,000 2,600,000 320,000 1,000,000 21,200,000 1,840,000 38,344,000 38,344,000 The following additional information is relevant for preparing the financial statements for the year ended 31th December 2011: Bad debts of $20,000 are to be written off. Allowance for doubtful debts is to be provided at a rate of 2% on the balance of accounts receivable outstanding as at 31st December 2011, after the bad debts adjustment above. Depreciation for the year is to be provided on the following basis: O Land: No depreciation is to be provided O Buildings: 2% on cost O Plant and equipment: 10% reducing balance basis O Vehicles: Based on mileage. The total mileage expected from the vehicles is 900,000 kilometres. For the year ended 31st December 2011 the mileage used was 67,500 kilometres. Long term loan of $2,600,000 was outstanding as at 1st January 2011. Interest on the loan is payable at 10% per annum. An amount of $400,000 representing the principal component of the long term loan is due for repayment on 20th January 2012. Investment in shares comprises of equity instruments $1,800,000 and shares held for trading $1,000,000. As at 31st December 2011 the market value of the equity instruments is $2,000,000 and market value of the shares held for trading is $1,600,000. These market values are considered to be the fair value of the shares. The value of inventory as at 31st December 2011 is as follows: Cost $200,000 Net realisable value $160,000 A professional valuation consultant re-valued land on 31st December 2011 at $5,400,000 using fair value. The revaluation reserve as at 1st January 2011 was in respect of a revaluation of land in previous financial reporting periods. Building was re-valued for the first time. The new market value of the building as at 31st December 2011 is $2,600,000. The values of other non-current assets are as follows: Vehicles Plant and Equipment Bank service charges Fines and penalties Entertainment expenses Distribution expenses Insurance Advertising and sales promotion As at 31th December 2011 Other expenses comprises of the following: Accounting fee (Question 4 - continued) Value In Use $400,000 $1,950,000 Net Selling price $390,000 $1,900,000 $40,000 $10,000 $12,000 $24,000 $160,000 $40,000 $64,000 $350,000 (Question 4 - continued on next page) CONTINUED The tax for the period is $424160 Expenses are classified in the Statement Comprehensive Income by function. Included in the contributed equity of $5,000,000 is an amount of $3,000,000 representing capital contribution from issue of ordinary shares during the year ended 31st December 2011. Preference shares that were issued in 2009 are redeemable on 18th July 2019. The preference share are cumulative with fixed dividends and non participatory. Prepare the following for Metro Trading Limited: (a) Balance day journal adjustments (without narrations) in general journal form for the year ended 31st December 2011. (b) A Statement of Comprehensive Income for the year ended 31st December 2011. (c) (d) A Statement of Financial Position as at 31st December 2011. Supplementary note for property, plant and equipment reported in the Balance Sheet as at 31st December 2011. (e) A Statement of Changes in Equity for the year ended 31st December 2011. (f) Notes on five accounting policies used in the preparation of the financial statements. Metro Trading Limited is registered under the Companies Act 1993 and operates throughout New Zealand. Set out below is a list of balances extracted from the accounts of the company as at financial year end date 31st December 2011: Bank Land at fair value Buildings at cost Accumulated Depreciation - Building Plant & Equipment at cost Accumulated Depreciation - Plant & Equipment Vehicles at cost Accumulated Depreciation - Vehicles Contributed Equity (1,000,000 ordinary shares) Preference Shares Treasury Stock Purchases Directors' Fees Allowance for Doubtful Debts Audit Fees Donation Accounts Payable Accounts Receivable Dividend Income Dividends paid Interest Expense Rental Income Inventory as at 1st January 2011 Long Term Loan Other Expenses Retained Earnings1st January 2011 Revaluation Reserve - 1st January 2011 Investment in Shares at Cost Sales Salaries and Wages Debit $ 30,000 6,000,000 3,000,000 2,400,000 800,000 280,000 17,200,000 270,000 40,000 30,000 2,600,000 300,000 154,000 250,000 350,000 2,800,000 Credit $ 1,000,000 460,000 274,000 5,000,000 5,000,000 50,000 1,000,000 200,000 240,000 2,600,000 320,000 1,000,000 21,200,000 1,840,000 38,344,000 38,344,000 The following additional information is relevant for preparing the financial statements for the year ended 31th December 2011: Bad debts of $20,000 are to be written off. Allowance for doubtful debts is to be provided at a rate of 2% on the balance of accounts receivable outstanding as at 31st December 2011, after the bad debts adjustment above. Depreciation for the year is to be provided on the following basis: O Land: No depreciation is to be provided O Buildings: 2% on cost O Plant and equipment: 10% reducing balance basis O Vehicles: Based on mileage. The total mileage expected from the vehicles is 900,000 kilometres. For the year ended 31st December 2011 the mileage used was 67,500 kilometres. Long term loan of $2,600,000 was outstanding as at 1st January 2011. Interest on the loan is payable at 10% per annum. An amount of $400,000 representing the principal component of the long term loan is due for repayment on 20th January 2012. Investment in shares comprises of equity instruments $1,800,000 and shares held for trading $1,000,000. As at 31st December 2011 the market value of the equity instruments is $2,000,000 and market value of the shares held for trading is $1,600,000. These market values are considered to be the fair value of the shares. The value of inventory as at 31st December 2011 is as follows: Cost $200,000 Net realisable value $160,000 A professional valuation consultant re-valued land on 31st December 2011 at $5,400,000 using fair value. The revaluation reserve as at 1st January 2011 was in respect of a revaluation of land in previous financial reporting periods. Building was re-valued for the first time. The new market value of the building as at 31st December 2011 is $2,600,000. The values of other non-current assets are as follows: Vehicles Plant and Equipment Bank service charges Fines and penalties Entertainment expenses Distribution expenses Insurance Advertising and sales promotion As at 31th December 2011 Other expenses comprises of the following: Accounting fee (Question 4 - continued) Value In Use $400,000 $1,950,000 Net Selling price $390,000 $1,900,000 $40,000 $10,000 $12,000 $24,000 $160,000 $40,000 $64,000 $350,000 (Question 4 - continued on next page) CONTINUED The tax for the period is $424160 Expenses are classified in the Statement Comprehensive Income by function. Included in the contributed equity of $5,000,000 is an amount of $3,000,000 representing capital contribution from issue of ordinary shares during the year ended 31st December 2011. Preference shares that were issued in 2009 are redeemable on 18th July 2019. The preference share are cumulative with fixed dividends and non participatory. Prepare the following for Metro Trading Limited: (a) Balance day journal adjustments (without narrations) in general journal form for the year ended 31st December 2011. (b) A Statement of Comprehensive Income for the year ended 31st December 2011. (c) (d) A Statement of Financial Position as at 31st December 2011. Supplementary note for property, plant and equipment reported in the Balance Sheet as at 31st December 2011. (e) A Statement of Changes in Equity for the year ended 31st December 2011. (f) Notes on five accounting policies used in the preparation of the financial statements.

Expert Answer:

Answer rating: 100% (QA)

a Balance day journal adjustments for the year ended 31st December 2011 1 Bad debts written off Bad Debts Expense 20000 Allowance for Doubtful Debts 20000 2 Provision for doubtful debts Allowance for ... View the full answer

Related Book For

Financial Reporting and Analysis Using Financial Accounting Information

ISBN: 978-1439080603

12th Edition

Authors: Charles H Gibson

Posted Date:

Students also viewed these accounting questions

-

In recent years, Freeman Transportation purchased three used buses. Because of frequent turnover in the accounting department, a different accountant selected the depreciation method for each bus,...

-

Cindy Bagnal, the manager of Cayce Printing Service, has provided you with the following aging schedule for Cayce's accounts receivable: Cindy indicates that the $126,700 of accounts receivable...

-

Clarissa sells her cupcakes for $2.50 each. Clarissa's variable costs per cupcake equal $0.50 and her monthly fixed costs are $3,000. Required: a. What is Clarissa's contribution margin per cupcake?...

-

A simply supported wood beam AB with span length L = 4m carries a uniform load of intensity q = 5.8kN/m (see figure). (a) Calculate the maximum bending stress Ïmax due to the load if the beam...

-

On June 8, 2017, Eugene Weiner made a post on Isaac Aflalos Facebook page. The post read, Yurim and Isaac took advantage of a old 94plus sick man elder abuse [sic]. Alflalo took umbrage to the post...

-

Information related to Jordan Schlansky Company for 2012 is summarized below. Total credit sales $2,200,000 Accounts receivable at December 31 825,000 Bad debts written off 33,000 Instructions (a)...

-

Convert the following NFA into an equivalent DFA. Show every step. 91 e 93 90 e a b 92 b e

-

Powell Office Express is the company that made the photocopier popular, but since then has grown a new business related to business process outsourcing. It recently disclosed the following...

-

You roll a 6-sided die. What is the probability that you will roll either a 6 or a 5? P(6 or 5)= You flip a 2-sided coin. What is the probability that you will get either heads or tails? P(heads or...

-

x+12 Let f(x) = 6x + 12 and g(x) == Find (fo 2 g)(-0.3) and (gof)(-0.3). Round to three decimals if necessary. a) (fog)(-0.3) (fog)(-0.3)= b) (g)(-0.3) (gof)(-0.3)=

-

Discuss an example of Canadian media (newspaper, radio program, film, TV show, YouTube series, etc.) and how it has influenced understanding of Canadian culture?

-

Which is the more powerful, appeal to reason or appeal to emotion? Discuss your response with an example. In addition, which do you think is a more difficult challenge, discontinuance or deterrence?...

-

In the basic communication model, which term refers to the method that is used to convey the message? Explain 3 Communication models

-

Daniel, age 38, is single and has the following income and expenses in 2018: Salary income $60,000 Net rent income 6,000 Dividend income 3,500 Payment of alimony in accordance with the separation...

-

Solve each equation. x 3 - 6x 2 = -8x

-

In this case, we review the debt of several specialty retail stores. The companies reviewed and the year-end dates are as follows: 1. Abercrombie & Fitch Co. (January 31, 200952-week; February 2,...

-

Could a profit-oriented enterprise use fund accounting practices? Comment.

-

You are considering buying the stock of a large publicly traded company. You need an opinion of timeliness of the industry and the company. Which publication could you use?

-

Graph the following table: a. What is marginal product and average product at each level of production? b. Graph marginal product and average product. c. Label the areas of increasing marginal...

-

If average product is falling, what is happening to short-run average variable cost?

-

If marginal cost is increasing, what do we know about average cost?

Study smarter with the SolutionInn App