Question: Midterm Materials Although it is easy to find additional material related to bonds and fixed-income analysis rest assured that all the relevant information has been

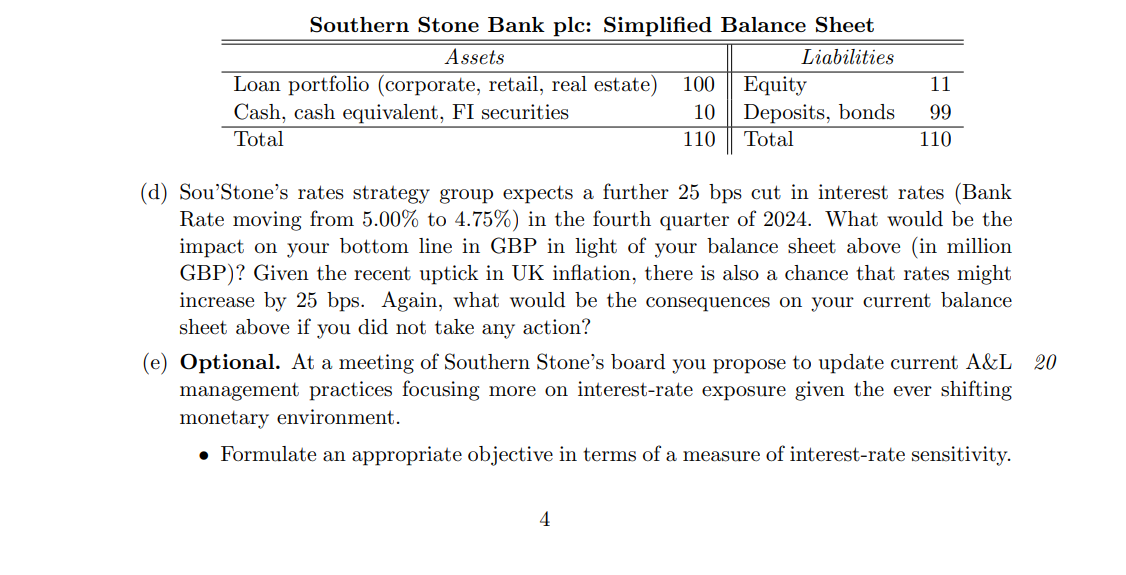

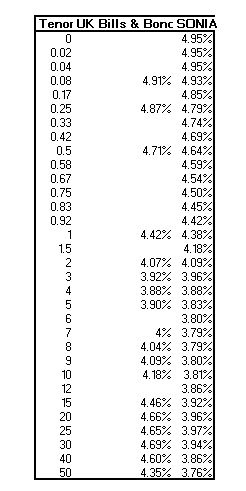

Midterm Materials Although it is easy to find additional material related to bonds and fixed-income analysis rest assured that all the relevant information has been carefully screened and consolidated in the present midterm materials. Hence, do not waste too much of your precious time looking for additional material on the internet unless directed to do so but, instead, rely on the data provided in these instructions, the case, and the data file. Instructions and questions: Midterm Exam (this document). Nangle, T., \"Everything you always wanted to know about bonds (but were afraid to ask). A gascon's guide to gilts,\" Financial Times Alphaville October 23, 2024. You might want to use both the included PDF of the article and the online original, which has nice addtional links (for background information and related topics) as well as interactive charts and graphs, at Nangle (FTAV 241023), Everything Bonds Make sure you have a (free) subscription to the FT through AU (sign up instructions on the Library's website). Data file containing relevant data from and for the FTAV article: FTVA Everything Bonds Data.xlsx. Background readings: UK Debt Management Office (2005), Formulae for Calculating Gilt Prices and Yields; Williamson (2016), \"Neo-Fisherism,\" The Regional Economist July 2016, St. Louis Federal Reserve Bank. In addition, you might want to consult various course materials pertaining to the technical and conceptual aspects of the exam. Case Questions Presentation. In preparing your solutions, make sure to adhere to the presentational guidelines detailed in the above Instructions. In particular, present any analytic spreadsheets as succinctly as possible but make sure to include all the results and even intermediate steps if warranted in your answer document: do not simply refer to your Excel spreadsheets (e.g., \"see XLSX tab 7c\"). Throughout, you are free to make additional assumptions as need be but remember that you have to carefully motivate and document them. If you feel that information is missing or a question ambiguous, please send me email. Exposition. It is easy to get carried away by case studies and write longwinded essays. Most questions are straightforward and do not require long answers or can be answered in tabular form or with simple calculations. If you find yourself writing long answers you probably are missing the point or have not carefully studied the case which contains all the necessary information for succinct, to-the-point answers. Just keep it short and spend more time on thinking through the questions and case rather than writing too much. Exam strategy. You need to give your mind the necessary time and information to start processing the midterm and concentrating on the issues at hand consciously and subconsciously. Before starting the exam, (i) make sure to carefully read through the case, (ii) review the data file (all the tabs, not just opening it \"and taking a look\"), and (iii) read through all the questions below after you thoroughly understand the case and supplied data (as in real life, not all the data is relevant for this midterm!). Then go again through the case questions and order them by preference. Finally, start with the question you ranked second by preference, next answer your favorite question, and then work away at the remaining question in your original order. Currency. A note of caution: the United Kingdom (UK) uses the British Pound as in \"penny- wise and pound-foolish\" (ISO code GBP, currency sign ) as its national money very much like the USA relies on our beloved (greenback) US Dollar (ISO code USD, currency sign $). However, the GBP is also referred to as Sterling abbreviated STG (no, not Raheem Sterling!) as in \"a sterling reputation\" harking back to its origins as pounds of sterling silver which is defined 92.5% pure silver content. On October 14, 2024 the GBP was trading at $1.3049/GBP, on October 23, 2024 at $1.3053/GBP, and on November 03, 2024 at $1.2910/GBP. 1. Of Gilts and Bills. Like on most Fridays in the year, on October 11, 2024 His Majesty's Treasury sold a large amount of T-Bills to fund government operations. Analyze the place- ment mechanism and outcome paying particular attention to similarities and dissimilarities with our own primary market for (US)T-Bills. (a) What are gilts and who issues them? What are T-Bills? (b) Describe how are T-bills are sold in the UK and compare the procedure to the US Treasuries market. The setting and the allocation mechanism is very similar in the US and UK but the final price is set differently. Can you spot the difference? Explain. (c) Analyze the placement procedure and instrument sold on Friday, October 11, 2024. What are the settlement date (actual delivery of the security), nominal and actual ma- turity, total amount tendered, total amount alloted, total amount sold, lowest-highest- actual yield? Present the information in tabular form. 100+20 (d) What amount has been allotted at the highest accept yield? Be precise, i.e., absolutely no rounding. Who presumably got the residual to the nearest nice round number? (e) Verify the prices at the various yield points making sure to fully show your calculations. Explain any deviations from Bloomberg's results. (f) Given the bill's actual price, what is its (bank) discount yield and how does it relate to its BEY (bond equivalent yield) of the issue? Be precise and very careful with the actual day count which is crucial. (g) Optional. Is it true that \"the gap between 97.691 and 97.724 is not very large ... it 20 seems a pretty microscopic price difference?\" What does it represent in terms of auction outcomes? 2. Interest-Rate Risk Management. As chief financial officer (CFO) of Southern Stone 100+20 Bank ple (Sou'Stone: \"we leave no stone unturned\"), a midsized full-service bank in the 3 United Kingdom, one of your primary tasks is the management of its interest rate exposure. You are currently trying to convince your board, composed of an odd assortment of local worthies, former politicians, as well as some very sharp academics, bankers, and accountants, to implement a comprehensive review of your institution's interest-rate risk management, which heavily relies on mathematics and statistics. In particular, it is built on mathematical relations between fixed-income prices and yields and simulated term structure models for the estimation of crucial parameters for your approach. (a) (c) State a formula which relates changes in fixed-income price to interest-rate variability (i.e., changes in yields) using two different measures of yield sensitivity. Illustrate how bond prices are related to yields on the basis of this formula and a diagram. Why or why not is this approach valid? On October 14, 2024, Southern Stone bought GBP 100m strips of the just auctioned 50Y Gilt, which its Treasury Group internally refers to as the Gorilla Bondzo. Note that the convexity of a zero is very close to the square of its maturity; you can ignore slight maturity mismatches and small estimation errors. Determine its presumable yield (from the data in the case), modified duration, and convexity. Compute its current price and the sterling amounts by which you would expect its price to change for a 60 bps rise and fall in interest rates over the next 12 months. Currently, the average duration of your loan portfolio is 3 years whereas the average duration of your various fixed income liabilities (deposits and bonds) is 1.5 years. You may assume that the average yield on assets and liabilities for a bank of Southern Stone's credit quality is around 7.00% and 5.00%, respectively. Propose a strategy to neutralize the effect of interest-rate changes on your balance sheet which is (in million GBP) as follows: Southern Stone Bank plc: Simplified Balance Sheet Assets Liabilities Loan portfolio (corporate, retail, real estate) 100 || Equity 11 Cash, cash equivalent, FI securities 10 || Deposits, bonds 99 Total 110 || Total 110 (d) Sou'Stone's rates strategy group expects a further 25 bps cut in interest rates (Bank Rate moving from 5.00% to 4.75%) in the fourth quarter of 2024. What would be the impact on your bottom line in GBP in light of your balance sheet above (in million GBP)? Given the recent uptick in UK inflation, there is also a chance that rates might increase by 25 bps. Again, what would be the consequences on your current balance sheet above if you did not take any action? (e) Optional. At a meeting of Southern Stone's board you propose to update current A&L management practices focusing more on interest-rate exposure given the ever shifting monetary environment. e Formulate an appropriate objective in terms of a measure of interest-rate sensitivity. 20 e One of your board members, a retired former minister recently voted out of office and parliament and now elevated to the House of Lords, claims that your approach to interest-rate exposure measurement and management is fundamentally flawed. What problems might he referring to? Do you agree with his assessment? 3. Optional Bonus Problem Corporate Lending, Investing, and Forward Rates. You, a senior senior trader on Southern Stone's Rates Derivatives desk just took a call from the Head of Corporate Lending at your bank. One of her major manufacturing clients, who are retooling part of their main factory, just bought a new set of customized machinery (robots) to be delivered in six months' time. The company's treasurer intends to initially finance the purchase in the short-term loan market for six months and had inquired about the possibilities of locking in the borrowing cost now. The amount is GBP 100m and the loan would be disbursed in a six months from now to be repaid in exactly one year's time from now. She wants to price the loan and talk through the transaction with you. (a) What kind of solution to their problem should Corporate Lending suggest to their man- ufacturing client? (b) You ask your sales analyst to collect the necessary information (from the case, not Bloomberg in this instance) for the appropriate reference rate (what might it be) to price the appropriate corporate-loan product on October 14, 2024: Maturity (M) Reference Rate (%) 1 3 6 12 50 (c) Provide a quote to the Head of Corporate Lending so that they, in turn, can price the borrowing cost for the preceding suggestion. Since your analyst is new and you are of a somewhat suspicious nature he better indicate his methodology to derive the quote. UNI IVI DEBT MANAGEMENT OFFICE Formulae for Calculating Gilt Prices from Yields 1s edition: 8 June 1998 2nd edition: 15 January 2002 3rd edition: 16 March 200510/31/24, 10:14 AM Everything you always wanted to know about bonds (but were afraid to ask) Everything you always wanted to know about bonds (but were afraid to ask) A gascon's guide to gilts MOU Oa SETA \f\f\f\f

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!