Question: Mini Case 2 Normal Boom 0.5 0.3 6.0 6.0 20.0 42.0 5.0 (12.0) 15.0 26.0 16.0 30.0 Your client is a very curious investor who

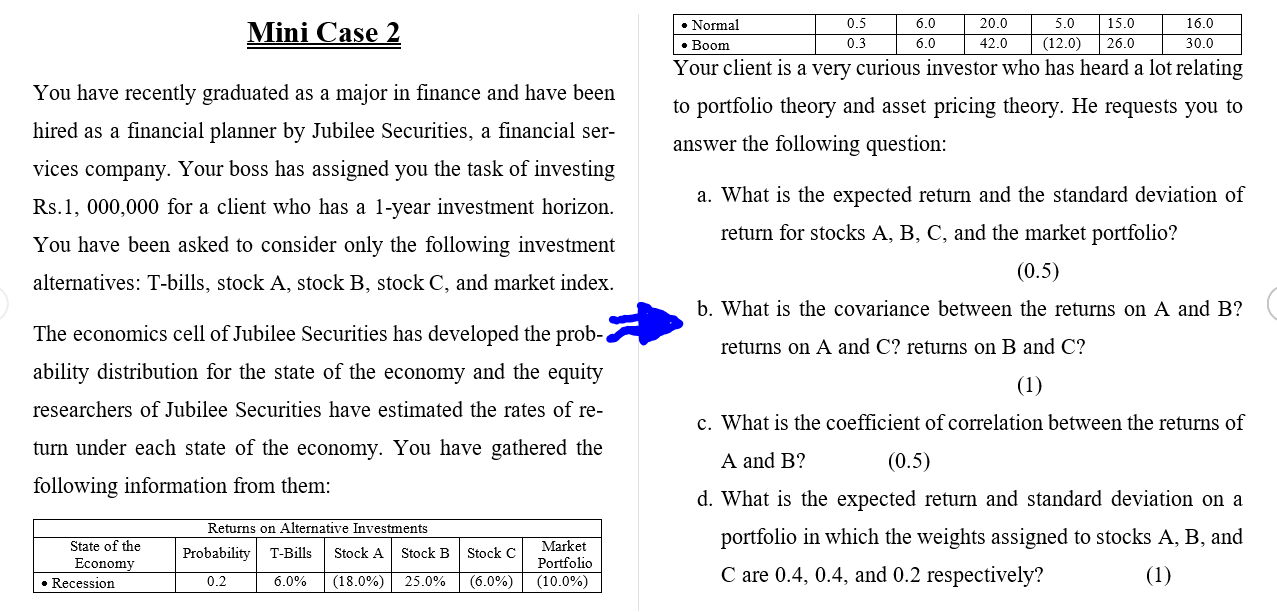

Mini Case 2 Normal Boom 0.5 0.3 6.0 6.0 20.0 42.0 5.0 (12.0) 15.0 26.0 16.0 30.0 Your client is a very curious investor who has heard a lot relating to portfolio theory and asset pricing theory. He requests you to answer the following question: You have recently graduated as a major in finance and have been hired as a financial planner by Jubilee Securities, a financial ser- vices company. Your boss has assigned you the task of investing Rs.1, 000,000 for a client who has a 1-year investment horizon. You have been asked to consider only the following investment alternatives: T-bills, stock A, stock B, stock C, and market index. a. What is the expected return and the standard deviation of return for stocks A, B, C, and the market portfolio? (0.5) b. What is the covariance between the returns on A and B? returns on A and C? returns on B and C? (1) The economics cell of Jubilee Securities has developed the prob- ability distribution for the state of the economy and the equity researchers of Jubilee Securities have estimated the rates of re- turn under each state of the economy. You have gathered the following information from them: c. What is the coefficient of correlation between the returns of A and B? (0.5) d. What is the expected return and standard deviation on a portfolio in which the weights assigned to stocks A, B, and C are 0.4, 0.4, and 0.2 respectively? (1) State of the Economy Recession Returns on Alternative Investments Probability T-Bills Stock A Stock B Stock C 0.2 6.0% (18.0%) 25.0% Market Portfolio (10.0%) (6.0%)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts