Question: Mini Case Study Montmarte v Bervic Montmatre plc is a computer manufacturing company and the board of directors is considering buying Bervic Co, a private

Mini Case Study Montmarte v Bervic

Montmatre plc is a computer manufacturing company and the board of directors is considering buying Bervic Co, a private limited company owned mainly by the Bervics family which manufactures computer monitor screens. If they succeed with the bid the Board of Montmatre have proposed to continue operating Bervic as a going concern as they are in the same industry and Bervic currently serves as a supplier company. Bervics shares are owned by the Bervic family members.

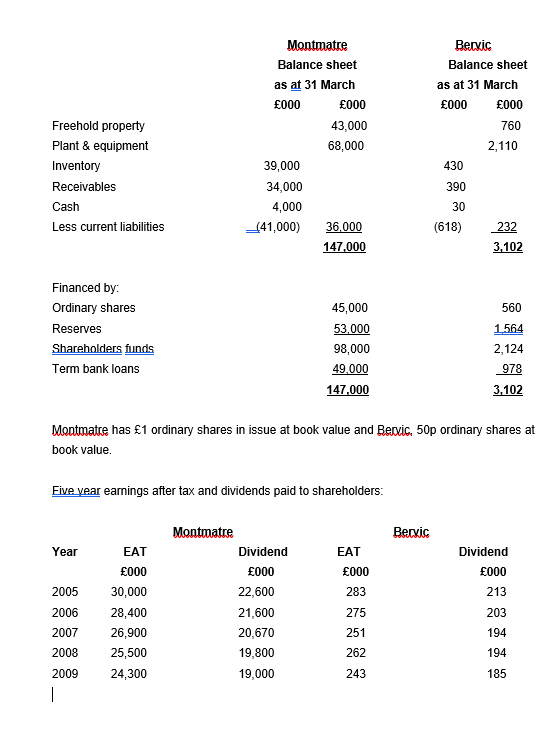

Below is the summarised current years set of financial statements for both companies:

The managing director of Bervic who is also a major shareholder receives an annual salary of 150,000. He vetos most strategic decisions and earns 40,000 more than the average salary received by managing directors of similar companies. The managing director would be replaced, if Montmatre purchases Bervic.

The freehold property of Bervic has not been revalued for five years and is believed to have a market value of 1,100,000. The balance sheet value of plant and equipment is believed to fairly reflect its replacement cost, but its value if sold is likely not to equal its replacement value. Almost 85,000 of inventory is obsolete and could only be sold as a scrap for 20,000.

The ordinary shares of Montmatre is currently trading at 550p ex-div. Bervics shareholders required rate of return on investment has been estimated by CAPM at 15%.

Both companies pay corporation tax at 30%.

Required

Use a variety of valuation models to determine the value of Bervic Co and advise the board of Montmatre as to how much it should offer for Bervics shares. Include in your advice why the board should consider offering Bervic shareholders the maximum price for their shares. Note that the share capital of Bervic has not increased over the last five years. Clearly state any relevant assumptions provided they do not change the outcome of the answer to the question.

Montmatre Balance sheet as at 31 March 000 000 43,000 68,000 39,000 34,000 4,000 141,000) 36.000 147,000 Becxic Balance sheet as at 31 March 000 000 760 2,110 430 Freehold property Plant & equipment Inventory Receivables 390 Cash 30 Less current liabilities (618) 232 3,102 560 Financed by: Ordinary shares Reserves Shareholders funds Term bank loans 1.564 45,000 53,000 98,000 49,000 147,000 2,124 978 3,102 Montmatre has 1 ordinary shares in issue at book value and Recxic, 50p ordinary shares at book value. Five year earnings after tax and dividends paid to shareholders: Becxic Year EAT 000 283 EAT 000 30,000 28,400 26,900 25,500 24,300 Dividend 000 213 203 2005 2006 2007 Montmatre Dividend 000 22,600 21,600 20,670 19,800 19,000 275 251 262 194 2008 194 2009 243 185 Montmatre Balance sheet as at 31 March 000 000 43,000 68,000 39,000 34,000 4,000 141,000) 36.000 147,000 Becxic Balance sheet as at 31 March 000 000 760 2,110 430 Freehold property Plant & equipment Inventory Receivables 390 Cash 30 Less current liabilities (618) 232 3,102 560 Financed by: Ordinary shares Reserves Shareholders funds Term bank loans 1.564 45,000 53,000 98,000 49,000 147,000 2,124 978 3,102 Montmatre has 1 ordinary shares in issue at book value and Recxic, 50p ordinary shares at book value. Five year earnings after tax and dividends paid to shareholders: Becxic Year EAT 000 283 EAT 000 30,000 28,400 26,900 25,500 24,300 Dividend 000 213 203 2005 2006 2007 Montmatre Dividend 000 22,600 21,600 20,670 19,800 19,000 275 251 262 194 2008 194 2009 243 185

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts