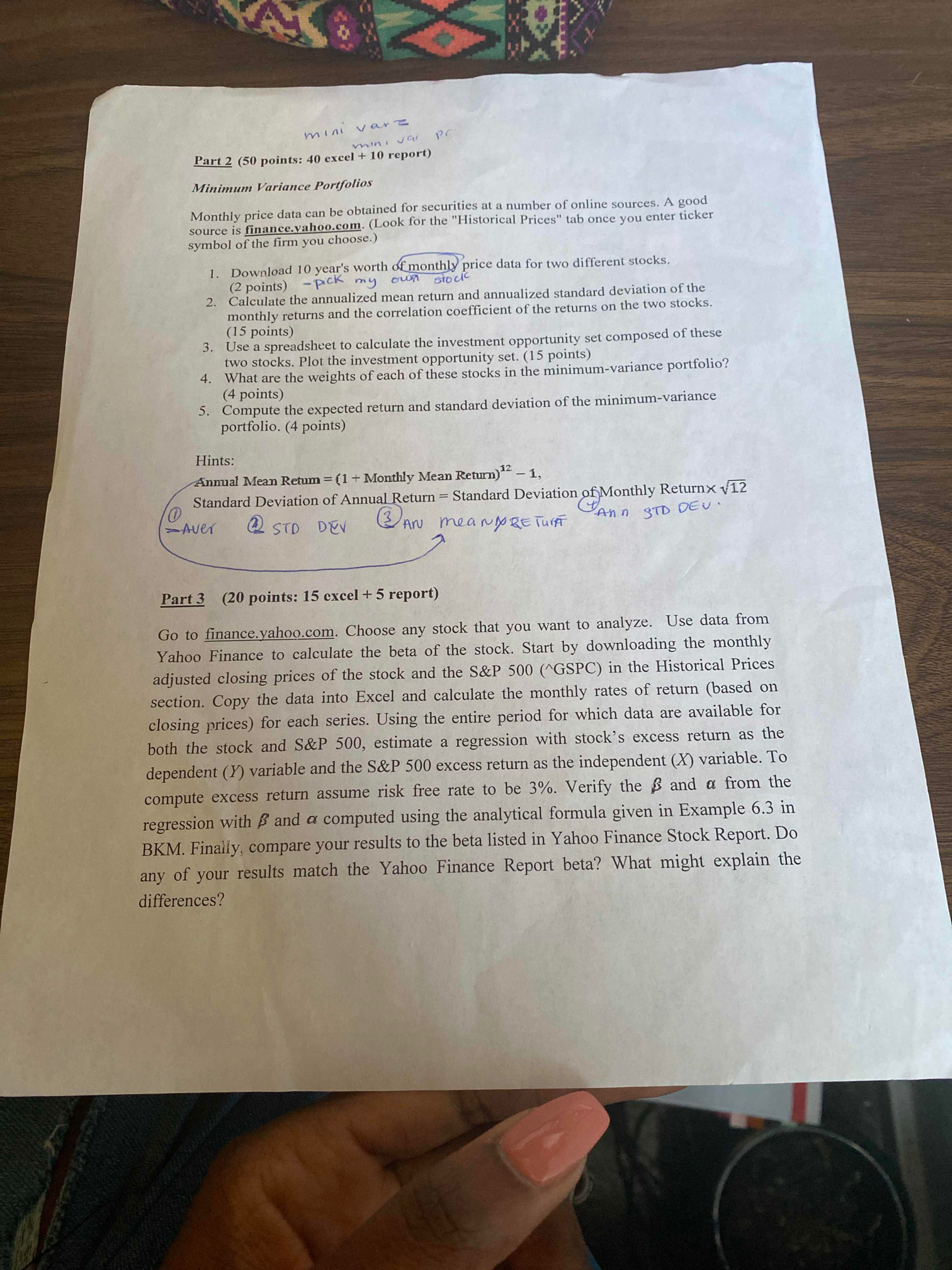

Question: mini var mini var pr Part 2 (50 points: 40 excel + 10 report) Minimum Variance Portfolios Monthly price data can be obtained for securities

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock