Question: ( Minimum variance portfolio and efficient portfolio to match target return ) . During the decade 2 0 0 5 2 0 1 4 ,

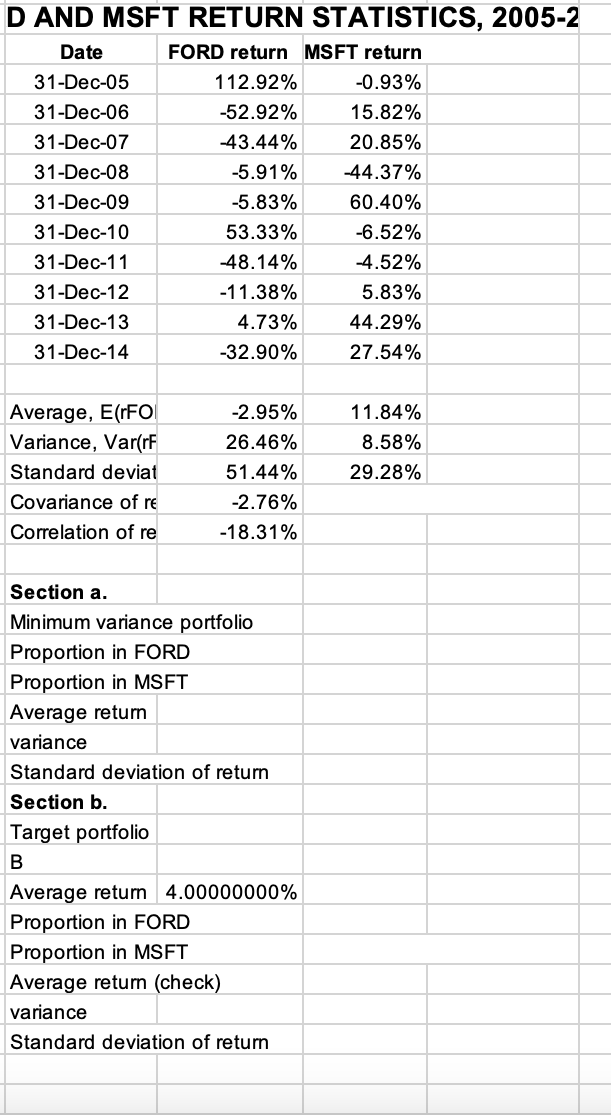

Minimum variance portfolio and efficient portfolio to match target return During the decade Ford and Microsoft MSFT were negatively correlated see data below Find the following two portfolios: a Find The minimum variance portfolio. a: what is the proportion in Ford? a: what is the average return for the portfolio? a: the standard deviation of return for the portfolio? b The efficient portfolio having an expected return of a: what is the proportion in Ford? a: what is the average return for the portfolio? a: the standard deviation of return for the portfolio?

D AND MSFT RETURN STATISTICS,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock