Mitchells Food Ltd manufactures chocolate products, which it markets both under its own brand and in unbranded

Question:

Mitchell’s Food Ltd manufactures chocolate products, which it markets both under its own brand and in unbranded packs. Management have adopted a (de-centralized) divisional structure for performance measurement purposes.

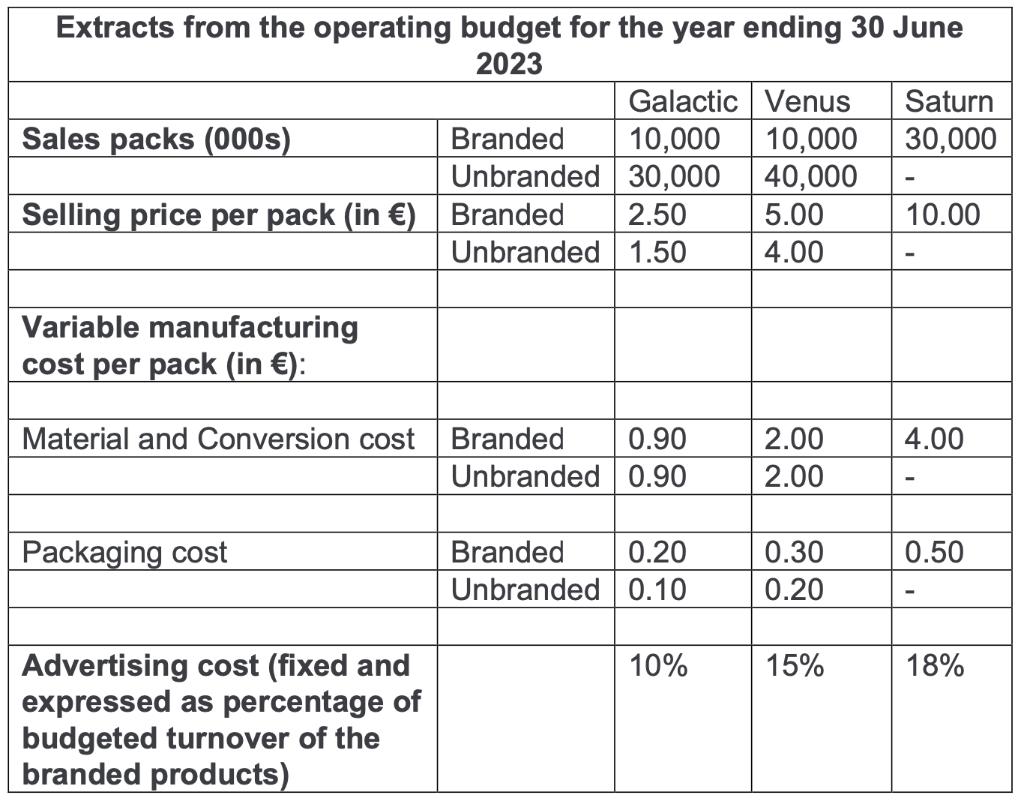

Division-M, which is based in County Cork, south-east of Ireland, manufactures three chocolate products, namely, Galactic, Venus and Saturn, mainly for sale in the domestic market. Budgeted information for Division-M for the year ending 30 June 2023 is as follows:

Division-M is expected to spend €145,000,000 in the year to 30 June 2023 on fixed overheads. Also, advertising is committed under a fixed-term contract and is regarded as fixed cost. Budgeted advertising cost is estimated as percentage of the turnover.

Each of the three products is only sold as a single pack. During the year to 30 June 2023, it is estimated that a maximum of 125 million packs could be manufactured and the management does not plan to increase the manufacturing capacity for Division-M. However, as all the products are manufactured using the same process, management has the flexibility to alter the product mix.

Division-Z of Mitchell’s Food Ltd. is located in Dublin. Division-Z purchases products from various sources, including other divisions of the company, for resale purposes. Recently, Division-Z has requested two alternative quotations from Division-M, for the next year:

Quotation 1: To purchase 5 million packs of ‘Saturn’. Quotation 2: To purchase 12 million packs of ‘Saturn’.

The senior management of Mitchell’s Food Ltd. have decided that a minimum of 30 million packs for ‘Saturn’ must be reserved for local customers in the south of Ireland, in order to ensure that demand can be satisfied and that the product’s competitive position is further consolidated in the local market. Nevertheless, the management is willing, if necessary, to reduce the budgeted quantities of other products in order to satisfy the requirements of Division-Z, however, only to an extent which would maximise the overall contribution for the company as a whole. The senior management uses financial performance measures, particularly ROI and RI, for measuring divisional performance.

The Divisional manager for Division-Z is aware that a competitor product for Saturn is available from another supplier with an estimated price of €7.00 per pack. As per the policy set out by the senior management of Mitchell’s Food Ltd, the de-centralized divisions are allowed autonomy to decide about their suppliers and in setting the transfer price (in case of inter-division transactions), so long the overall contribution for the company could be maximized. Therefore, being free to identify a transfer price, the management of Division-M intends to use market price less 25% as basis for each of the above quotations from Division-Z.

On a separate note, the manager of Division-M is wary that the prices of the chocolates which Division-M produces and sells, are higher than the local competitors. In order to increase local sales for Division-M, one potential option is to lower the prices of the chocolates (mainly the branded ones). However, the divisional manager is reluctant to reduce selling prices for regular sales, as that would decrease the Division’s profit margin, hence potentially diminishing the ROI and RI. The manager is, however, considering ways in which the Division’s costs could be better controlled, while meeting customers’ quality expectations.

In this regard, the manager of Division-M is considering to develop and initiate a quality management programme, for the branded chocolates in the first phase, because a substantial quantity of these products gets mis- shaped during the production process, and are therefore not sellable in the regular market. While the mis-shaped chocolates produced by Division-M gets sold at throw-away prices, in factory outlet shop, nonetheless, the manager and his team believes that getting mis-shaped chocolates and having to sell them in factory-outlet shop are ‘non-value adding’ activities and is a major quality concern. Recently, the manager of Division-M has been asked by the senior management of Mitchell’s Food Ltd. to explore implementation of a Cost of Quality model for Division-M, in order to implement steps which can improve the production processes at the division and hence minimize if not eliminate, the production of mis-shaped chocolates.

Note: Appropriateness of the Decision to use adjusted market price

I. Brief discussion of the alternative methods that could be applied

II. Appropriateness of choosing adjusted market price specifically

III. Implications for both divisions of that choice IV. Supporting calculations

Expert Answer:

I Brief Discussion of the Alternative Methods that Could be Applied There are a number of methods that could be applied to set a transfer price for th... View the full answer

Fundamentals of Cost Accounting

ISBN: 978-0077398194

3rd Edition

Authors: William Lanen, Shannon Anderson, Michael Maher