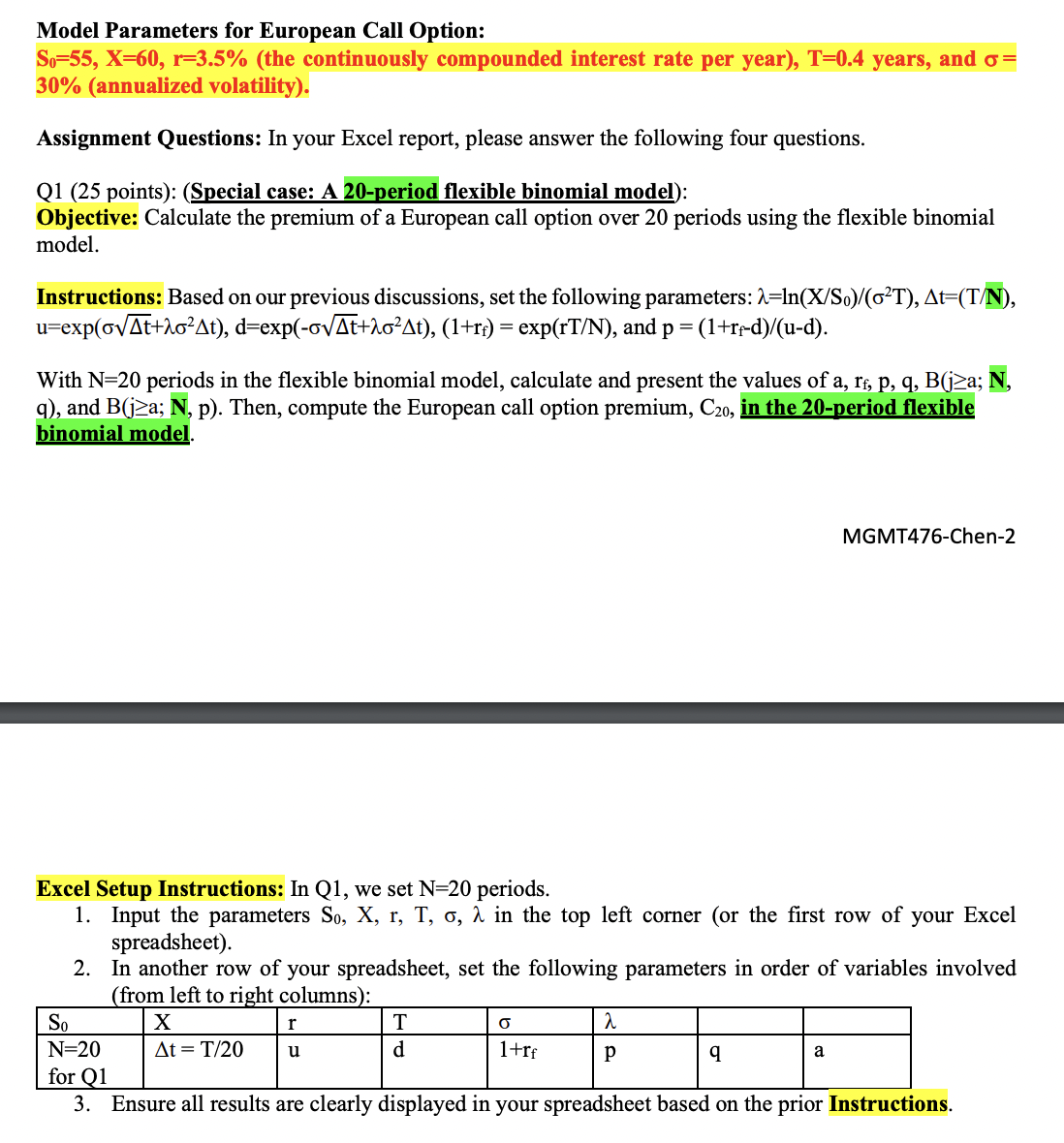

Question: Model Parameters for European Call Option: S 0 = 5 5 , x = 6 0 , r = 3 . 5 % ( the

Model Parameters for European Call Option:

the continuously compounded interest rate per year years, and

annualized volatility

Assignment Questions: In your Excel report, please answer the following four questions.

Q points: Special case: A period flexible binomial model:

Objective: Calculate the premium of a European call option over periods using the flexible binomial model.

Instructions: Based on our previous discussions, set the following parameters:

expexpexp and

With periods in the flexible binomial model, calculate and present the values of

and ; Then, compute the European call option premium, in the period flexible binomial model.

Excel Setup Instructions: In we set periods.

Input the parameters in the top left corner or the first row of your Excel

spreadsheet

In another row of your spreadsheet, set the following parameters in order of variables involved

from left to right columns:

Ensure all results are clearly displayed in your spreadsheet based on the prior Instructions.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock