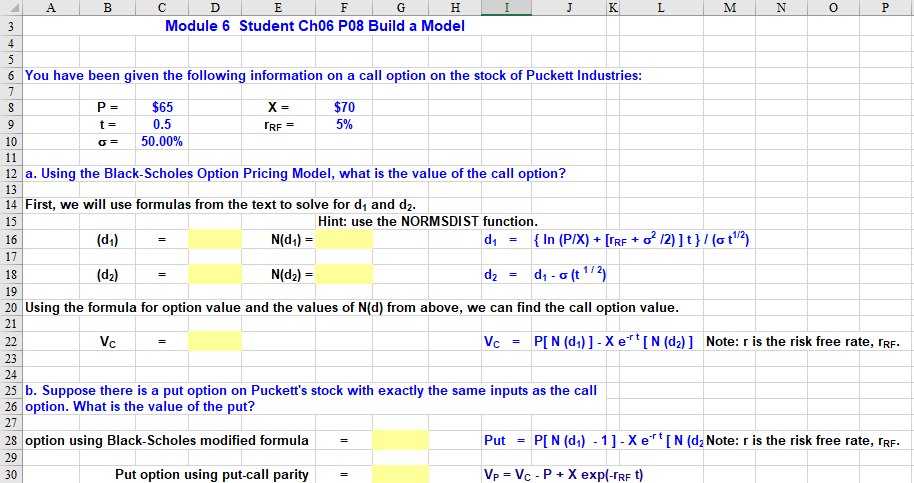

Question: Module 6 Student Ch06 P08 Build a Model 6 You have been given the following information on a call option on the stock of Puckett

Module 6 Student Ch06 P08 Build a Model 6 You have been given the following information on a call option on the stock of Puckett Industries P$65 $70 5% 0.5 50.00% TRF 10 - 12 a. Using the Black-Scholes Option Pricing Model, what is the value of the call option? 13 14 First, we will use formulas from the text to solve for di and d2 15 16 Hint: use the NORMSDIST function (di) N(d1) = 18 19 (d2)- N(d2) = 20 Using the formula for option value and the values of N(d) from above, we can find the call option value 21 VcPIN (d1)]-XeN (d2) Note: r is the risk free rate, rRF 23 24 25 b. Suppose there is a put option on Puckett's stock with exactly the same inputs as the call 26 option. What is the value of the put? 28 option using Black-Scholes modified formula PutPIN (di) -1]-XeN (d2 Note: r is the risk free rate, TRF 30 Put option using put-call parity =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts