Question: Monte Carlo - Stochastic Processes Question: Exercise (11.9)Suppose that you have bought a call option with strike price 100 yen, and want to evaluate its

Monte Carlo - Stochastic Processes Question:

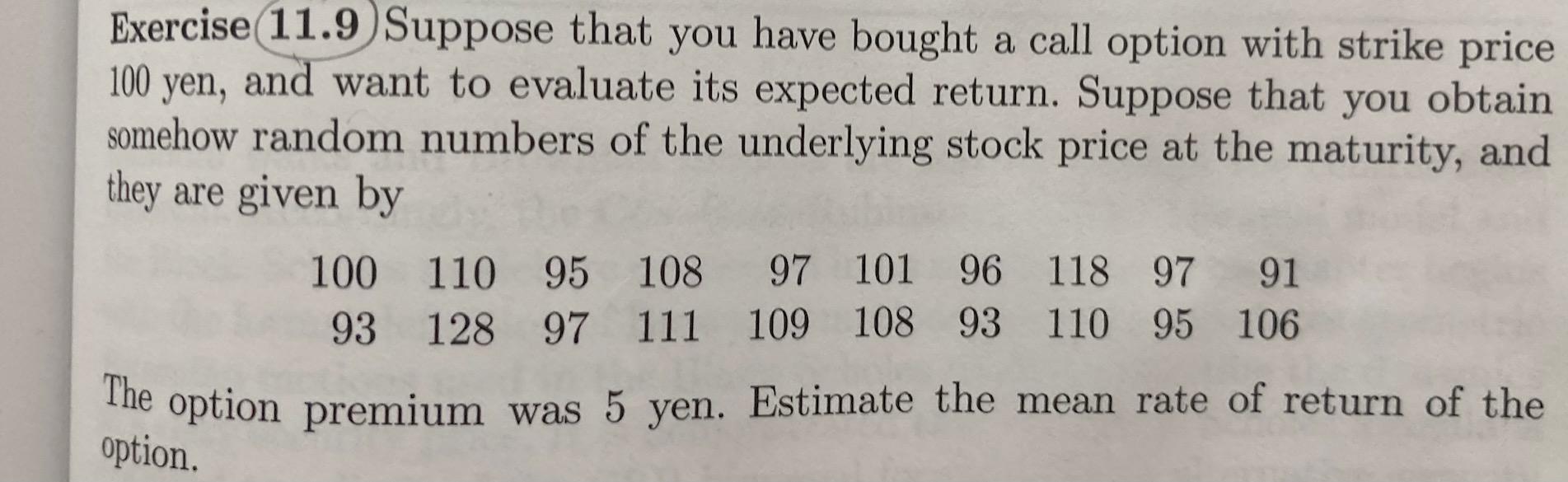

Exercise (11.9)Suppose that you have bought a call option with strike price 100 yen, and want to evaluate its expected return. Suppose that you obtain somehow random numbers of the underlying stock price at the maturity, and they are given by The option premium was 5 yen. Estimate the mean rate of return of the option

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock