Monte Company acquired 70% of the stock of Mo Company on 1 January 2018, for $150,000. On

Question:

Monte Company acquired 70% of the stock of Mo Company on 1 January 2018, for $150,000. On this date, the balances of Mo’s stockholders’ equity accounts were: Common Stock, $130,000, and Retained Earnings, $14,000. On 1 January 2018, the market value for the 30% of shares not purchased by Monte was $63,800.

On 1 January 2018, Mo’s recorded book values were equal to fair values for all items except: (1) accounts receivable had a book value of $40,000 and a fair value of $36,000, (2) buildings and equipment, net, had a book value of $35,000 and a fair value of $53,000, (3) the licenses intangible asset had a book value of $10,000 and a fair value of $52,000, and (4) notes payable had a book value of $24,000 and a fair value of $18,000. Both companies use the FIFO inventory method and sell all of their inventories at least once per year. The net balance of trade receivables are collected in the following year. On the acquisition date, the subsidiary’s buildings and equipment, net, had a remaining useful life of 6 years, licenses had a remaining useful life of 7 years, and notes payable had a remaining term of 4 years.

On 1 January 2021, Monte sold a building to Mo for $65,000. On this date, the building was carried on Monte’s books (net of accumulated depreciation) at $50,000. Both companies estimated that the building has a remaining life of 6 years on the intercompany sale date, with no salvage value.

Each company routinely sells merchandise to the other company, with a gross profit margin of 25 percent (regardless of the direction of the sale). During 2022, intercompany sales amount to $15,000, of which $8,000 of merchandise remains in the ending inventory of the parent. On 31 December 2022, $4,000 of these intercompany sales remained unpaid. Additionally, the subsidiary’s 31 December 2021 inventory includes $12,000 of merchandise purchased in 2021 from the parent. During 2021, intercompany sales amount to $20,000, and on 31 December 2021, $7,000 of these intercompany sales remained unpaid.

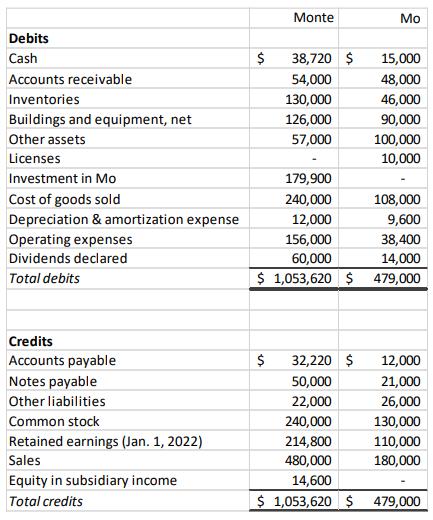

Monte uses the equity method to account for its investment in Mo. The pre-closing trial balances for the two companies for the year ended 31 December 2022, are provided on the following page.

Required: Prepare a consolidation worksheet and the appropriate eliminating entries to determine consolidated balances for external financial reporting as of 31 December 2022. You will earn credit for this problem by (1) journalizing the correct consolidating entries, and (2) computing the correct consolidated balances for each line item on the financial statements (including the income to the noncontrolling interest).

Expert Answer:

Consolidation work sheet Particulars Monte Company Mo Company Eliminations Non controlling interest ... View the full answer

International Financial Reporting A Practical Guide

ISBN: 978-1292200743

6th edition

Authors: Alan Melville