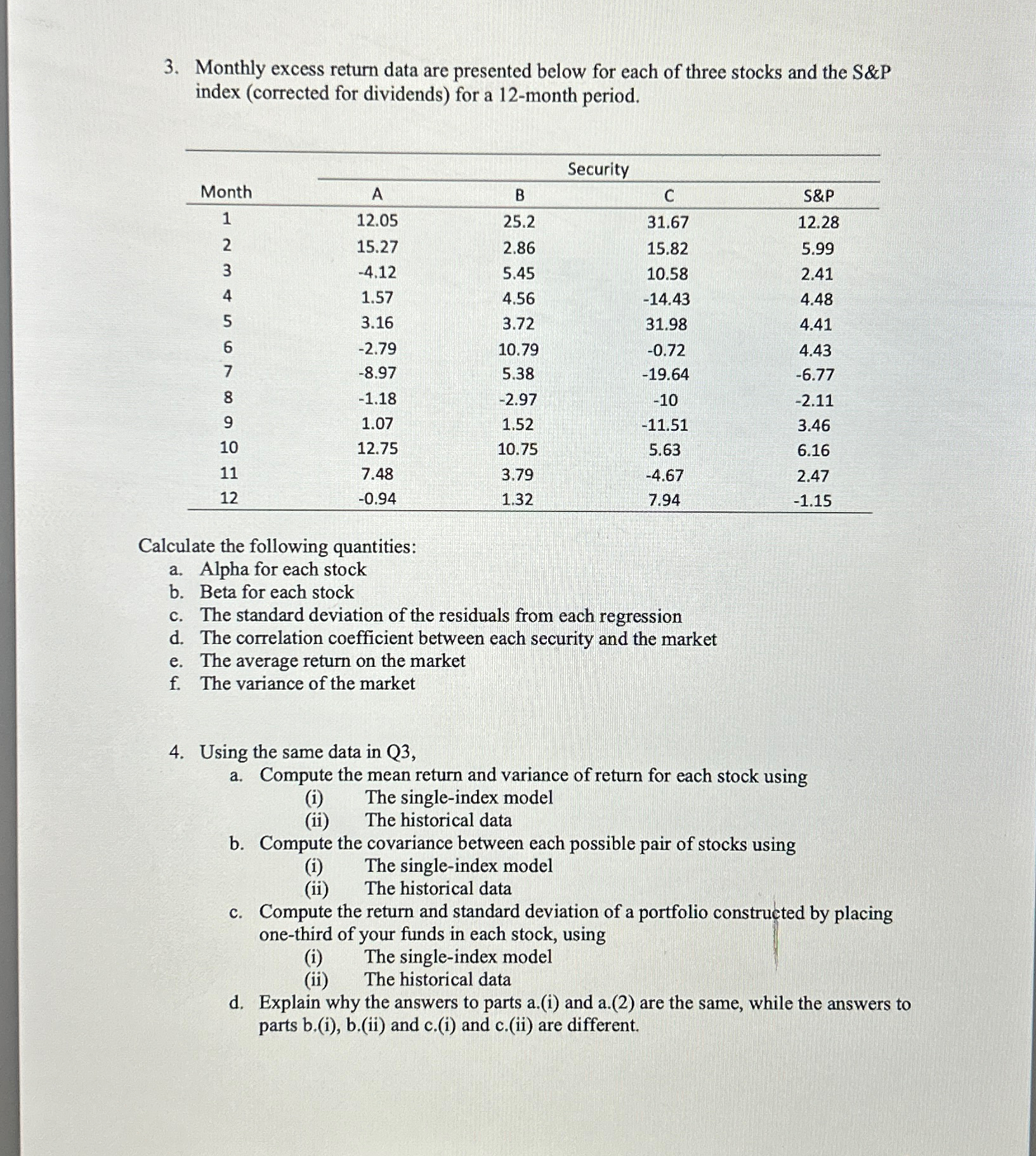

Question: Monthly excess return data are presented below for each of three stocks and the S&P index ( corrected for dividends ) for a 1 2

Monthly excess return data are presented below for each of three stocks and the S&P index corrected for dividends for a month period.

tableSecurityMonthABCS&P

Calculate the following quantities:

a Alpha for each stock

b Beta for each stock

c The standard deviation of the residuals from each regression

d The correlation coefficient between each security and the market

e The average return on the market

f The variance of the market

Using the same data in Q

a Compute the mean return and variance of return for each stock using

i The singleindex model

ii The historical data

b Compute the covariance between each possible pair of stocks using

i The singleindex model

ii The historical data

c Compute the return and standard deviation of a portfolio constructed by placing onethird of your funds in each stock, using

i The singleindex model

ii The historical data

d Explain why the answers to parts ai and a are the same, while the answers to parts bi bii and ci and cii are different.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock