Ms XYZ is a chef-turned-housewife, who could dish out plates of traditional Indian delicacies. She terminated...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

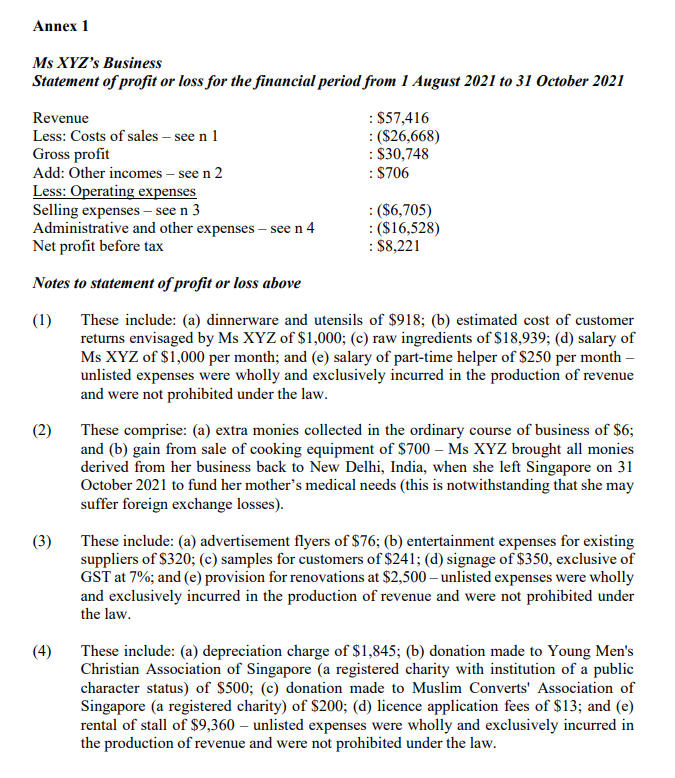

Ms XYZ is a chef-turned-housewife, who could dish out plates of traditional Indian delicacies. She terminated her employment as Head Chef with Indian Accent - a famous restaurant in New Delhi, India, that specialises in Indian-inspired cuisines - to follow her husband to Singapore for his one-year secondment stint. Ms XYZ and her husband arrived in Singapore from New Delhi, India, on 1 July 2021. Ms XYZ's husband bought 10,000 shares in a Singapore incorporated company prior to their arrival. He signed the sale and purchase agreement on 18 June 2021 and paid $1.80 per share, when the company's net asset value was $1.50 per share. Ms XYZ and her husband stayed in a rented condominium unit at Newton Edge along Makeway Avenue upon arrival in Singapore. The Singapore employer of Ms XYZ's husband signed the rental agreement on 2 June 2021 to rent the condominium unit for a year at $7,700 per month, which was 10% cheaper than the market rent then. Ms XYZ decided to set up an Indian food stall to hone her culinary skills. She leased a cooked food stall at Newton Food Centre along Clemenceau Avenue and signed the tenancy contract on 3 July 2021. Ms XYZ agreed to rent the cooked food stall for a year at $3,120 per month, when the market rent was $3,350 per month. Ms XYZ started selling Indian food on 1 August 2021. She had to end her business abruptly on 31 October 2021-see Annex 1 for the statement of profit or loss. Ms XYZ left for New Delhi, India, from Singapore on the same date to take care of her mother, who was critically ill. She never returned to Singapore thereafter. Mr ABC was a regular customer of Ms XYZ. He ran an accounting firm to service small and medium enterprises in Singapore and Malaysia. Mr ABC's accounting firm was registered with the Inland Revenue Authority of Singapore ("IRAS") for Goods and Services Tax ("GST") purposes. Mr ABC recorded several transactions from 1 February 2022 to 30 April 2022 - see Annex 2 for the details. He was financially prudent and would claim input tax from IRAS to the furthest extent possible. Mr ABC opted to account for GST on a quarterly basis upon GST registration. Mr ABC summarised his firm's transactions for the tax year ended 30 April 2022-see Annex 3 for the details. He was informed by his accountant that input tax claimed in the accounting periods of the said tax year amounted to $77,907.07 based on the GST returns filed with IRAS previously. Personal background (9) Ms XYZ and her husband were both citizens of India and 45 years of age as at 31 December 2021. Their parents have passed on apart from Ms XYZ's mother, who was taken care of by a medical team in New Delhi, India. Ms XYZ and her husband had no children. They had strong social support in New Delhi, India, only. Annex 1 Ms XYZ's Business Statement of profit or loss for the financial period from 1 August 2021 to 31 October 2021 Revenue Less: Costs of sales - see n 1 Gross profit Add: Other incomes - see n 2 Less: Operating expenses Selling expenses - see n 3 Administrative and other expenses - see n 4 Net profit before tax Notes to statement of profit or loss above (1) These include: (a) dinnerware and utensils of $918; (b) estimated cost of customer returns envisaged by Ms XYZ of $1,000; (c) raw ingredients of $18,939; (d) salary of Ms XYZ of $1,000 per month; and (e) salary of part-time helper of $250 per month - unlisted expenses were wholly and exclusively incurred in the production of revenue and were not prohibited under the law. (2) (3) : $57,416 : ($26,668) : $30,748 : $706 (4) : ($6,705) : ($16,528) : $8,221 These comprise: (a) extra monies collected in the ordinary course of business of $6; and (b) gain from sale of cooking equipment of $700 - Ms XYZ brought all monies derived from her business back to New Delhi, India, when she left Singapore on 31 October 2021 to fund her mother's medical needs (this is notwithstanding that she may suffer foreign exchange losses). These include: (a) advertisement flyers of $76; (b) entertainment expenses for existing suppliers of $320; (c) samples for customers of $241; (d) signage of $350, exclusive of GST at 7%; and (e) provision for renovations at $2,500-unlisted expenses were wholly and exclusively incurred in the production of revenue and were not prohibited under the law. These include: (a) depreciation charge of $1,845; (b) donation made to Young Men's Christian Association of Singapore (a registered charity with institution of a public character status) of $500; (c) donation made to Muslim Converts' Association of Singapore (a registered charity) of $200; (d) licence application fees of $13; and (e) rental of stall of $9,360 - unlisted expenses were wholly and exclusively incurred in the production of revenue and were not prohibited under the law. Question 1 Apply the principles of income tax to Ms XYZ and compute her taxable business profit and net income tax payable for the relevant year of assessment in a way that would minimise her income tax exposure in Singapore (as a household together with her husband). Show all workings and account for all income and deductions by way of tax adjustments - for example, if an income is taxable, an expense is deductible or a personal relief is not claimable, tax adjustments relating to that income, expense or personal relief must be indicated as "$0" in the income tax computation. State reasonable assumption(s) if any of the facts presented in the case study is/are unclear - for the avoidance of doubt, new facts may not be introduced. Ms XYZ is a chef-turned-housewife, who could dish out plates of traditional Indian delicacies. She terminated her employment as Head Chef with Indian Accent - a famous restaurant in New Delhi, India, that specialises in Indian-inspired cuisines - to follow her husband to Singapore for his one-year secondment stint. Ms XYZ and her husband arrived in Singapore from New Delhi, India, on 1 July 2021. Ms XYZ's husband bought 10,000 shares in a Singapore incorporated company prior to their arrival. He signed the sale and purchase agreement on 18 June 2021 and paid $1.80 per share, when the company's net asset value was $1.50 per share. Ms XYZ and her husband stayed in a rented condominium unit at Newton Edge along Makeway Avenue upon arrival in Singapore. The Singapore employer of Ms XYZ's husband signed the rental agreement on 2 June 2021 to rent the condominium unit for a year at $7,700 per month, which was 10% cheaper than the market rent then. Ms XYZ decided to set up an Indian food stall to hone her culinary skills. She leased a cooked food stall at Newton Food Centre along Clemenceau Avenue and signed the tenancy contract on 3 July 2021. Ms XYZ agreed to rent the cooked food stall for a year at $3,120 per month, when the market rent was $3,350 per month. Ms XYZ started selling Indian food on 1 August 2021. She had to end her business abruptly on 31 October 2021-see Annex 1 for the statement of profit or loss. Ms XYZ left for New Delhi, India, from Singapore on the same date to take care of her mother, who was critically ill. She never returned to Singapore thereafter. Mr ABC was a regular customer of Ms XYZ. He ran an accounting firm to service small and medium enterprises in Singapore and Malaysia. Mr ABC's accounting firm was registered with the Inland Revenue Authority of Singapore ("IRAS") for Goods and Services Tax ("GST") purposes. Mr ABC recorded several transactions from 1 February 2022 to 30 April 2022 - see Annex 2 for the details. He was financially prudent and would claim input tax from IRAS to the furthest extent possible. Mr ABC opted to account for GST on a quarterly basis upon GST registration. Mr ABC summarised his firm's transactions for the tax year ended 30 April 2022-see Annex 3 for the details. He was informed by his accountant that input tax claimed in the accounting periods of the said tax year amounted to $77,907.07 based on the GST returns filed with IRAS previously. Personal background (9) Ms XYZ and her husband were both citizens of India and 45 years of age as at 31 December 2021. Their parents have passed on apart from Ms XYZ's mother, who was taken care of by a medical team in New Delhi, India. Ms XYZ and her husband had no children. They had strong social support in New Delhi, India, only. Annex 1 Ms XYZ's Business Statement of profit or loss for the financial period from 1 August 2021 to 31 October 2021 Revenue Less: Costs of sales - see n 1 Gross profit Add: Other incomes - see n 2 Less: Operating expenses Selling expenses - see n 3 Administrative and other expenses - see n 4 Net profit before tax Notes to statement of profit or loss above (1) These include: (a) dinnerware and utensils of $918; (b) estimated cost of customer returns envisaged by Ms XYZ of $1,000; (c) raw ingredients of $18,939; (d) salary of Ms XYZ of $1,000 per month; and (e) salary of part-time helper of $250 per month - unlisted expenses were wholly and exclusively incurred in the production of revenue and were not prohibited under the law. (2) (3) : $57,416 : ($26,668) : $30,748 : $706 (4) : ($6,705) : ($16,528) : $8,221 These comprise: (a) extra monies collected in the ordinary course of business of $6; and (b) gain from sale of cooking equipment of $700 - Ms XYZ brought all monies derived from her business back to New Delhi, India, when she left Singapore on 31 October 2021 to fund her mother's medical needs (this is notwithstanding that she may suffer foreign exchange losses). These include: (a) advertisement flyers of $76; (b) entertainment expenses for existing suppliers of $320; (c) samples for customers of $241; (d) signage of $350, exclusive of GST at 7%; and (e) provision for renovations at $2,500-unlisted expenses were wholly and exclusively incurred in the production of revenue and were not prohibited under the law. These include: (a) depreciation charge of $1,845; (b) donation made to Young Men's Christian Association of Singapore (a registered charity with institution of a public character status) of $500; (c) donation made to Muslim Converts' Association of Singapore (a registered charity) of $200; (d) licence application fees of $13; and (e) rental of stall of $9,360 - unlisted expenses were wholly and exclusively incurred in the production of revenue and were not prohibited under the law. Question 1 Apply the principles of income tax to Ms XYZ and compute her taxable business profit and net income tax payable for the relevant year of assessment in a way that would minimise her income tax exposure in Singapore (as a household together with her husband). Show all workings and account for all income and deductions by way of tax adjustments - for example, if an income is taxable, an expense is deductible or a personal relief is not claimable, tax adjustments relating to that income, expense or personal relief must be indicated as "$0" in the income tax computation. State reasonable assumption(s) if any of the facts presented in the case study is/are unclear - for the avoidance of doubt, new facts may not be introduced.

Expert Answer:

Answer rating: 100% (QA)

Based on the provided information here is the breakdown of the statement of profit or loss for Ms XY... View the full answer

Related Book For

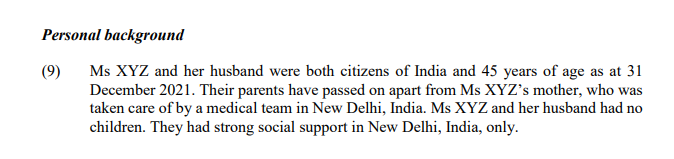

Business Law Text and Cases

ISBN: 978-0324655223

11th Edition

Authors: Kenneth W. Clarkson, Roger LeRoy Miller, Gaylord A. Jentz, F

Posted Date:

Students also viewed these accounting questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Water is an essential resource. For that reason moral considerations exert considerable pressure to assure that everyone has access to at least enough water to survive. Yet it appears that equity and...

-

How many degrees of freedom does an F-curve have? What are those degrees of freedom called?

-

Use indirect proof to prove that the following statements are tautologies. (Q R) [(P Q) (P R)] 32

-

On February 20, 2009, Cedar Valley Aviation, a wholly owned subsidiary of Aerial Services, Inc. (ASI), brought a Piper 522AS (Cheyenne II) in for maintenance to Des Moines Flying Service, Inc....

-

MicroProducts, Incorporated (MPI) manufactures printed circuit boards for a major PC manufacturer. Before a board is sent to the customer, three key components must be tested. These components can be...

-

A firm selling a normal good has a price elasticity of demand coefficient of 3.0 and an income elasticity of demand coefficient of 2.2. Assume that economists forecast a recession within the next...

-

During the Plan Order Phase, the hours for the Receive Order phase (marked with an *) are actual times, as this work has already been performed. In addition to these internal labors costs, the...

-

A lab technician has to prepare the following daily diet for rats used in an experiment. The diet requires a minimum of 600 mg of Vitamin C, 360 mg of Vitamin D, and 40 mg of Vitamin E. The rats...

-

In 20X8 and 20X9, Dorothy's Restaurant made the following transactions: 1. On July 1, 20X8, Dorothy's Restaurant borrowed $20,000 from the Kansas Bank at 12 percent interest for nine months. 2. On...

-

3. Is the commercial banks are financial intermediary? Why? How he could achieve this service? (5 Points) Enter your answer

-

Find a recent issue in the news relating to social media. 1. Summarize the article 2. Identify if it is a security, privacy and/or ethical issue. 3. Copy/paste the link to the article.

-

Due to a recent incident the company must go through an internal WHS audit. In the process of the audit you are required to collate employee feedback and other information to assess and improve the...

-

Alex personally mentored a client when the inherited a family business on the death of their elderly parent and they have developed a friendship. The client sold the family business during the year...

-

A ball is dropped from a height of 10m and is pulled towards the Earth due to the gravitational field of 10N/kg. What is the mass of the ball if the ball has 100J of GPE?

-

Sandcastles, Inc.s management has recently been looking at a proposal to purchase a new brick molding machine. With the new machine, the company would not have to buy bricks. The estimated useful...

-

Under the current UPA, can Als Feed Barn bring an action against Jason individually for the Cowboy Palaces debt? Why or why not? Grace Tarnavsky and her sons, Manny and Jason, bought a ranch known as...

-

Would a court likely decide that Odins employment contract falls within the Statute of Frauds? Why or why not? Charter Golf, Inc., manufactures and sells golf apparel and supplies. Ken Odin had...

-

Attorneys in personal-injury and other tort lawsuits frequently charge clients on a contingency fee basis; that is, a lawyer will agree to take on a clients case in return for, say, 30 percent of...

-

An engineering organisational system is composed of major groups such as management, research and development, preliminary design, experiments, product design and drafting, fabrication and...

-

The student-teacher learning activity is inherently a feedback exercise intended to reduce the system error to a minimum. The desired output is the knowledge being studied, and the student is the...

-

Give two examples of feedback control systems in which a human acts as a controller.

Study smarter with the SolutionInn App