Question: MTH 101 Milestone 1 Worksheet In this milestone, you will learn how to make wise financial decisions Whether you are a recent college graduate or

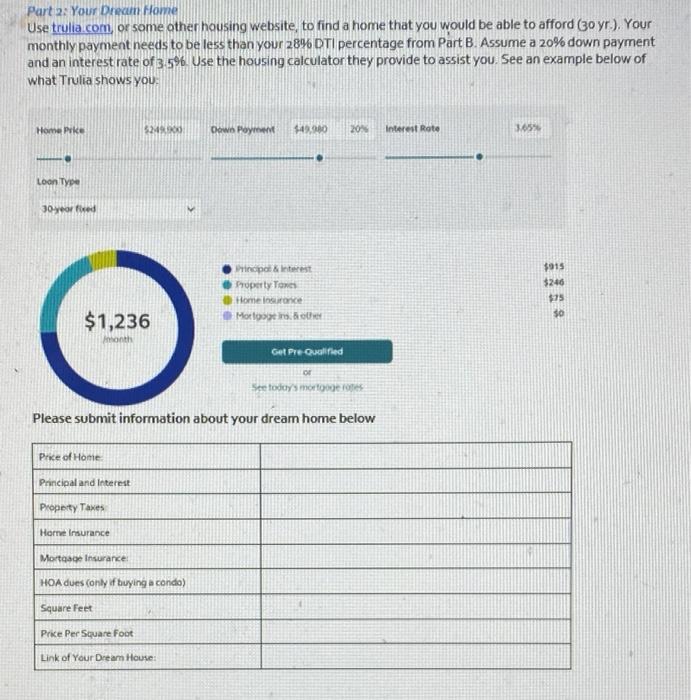

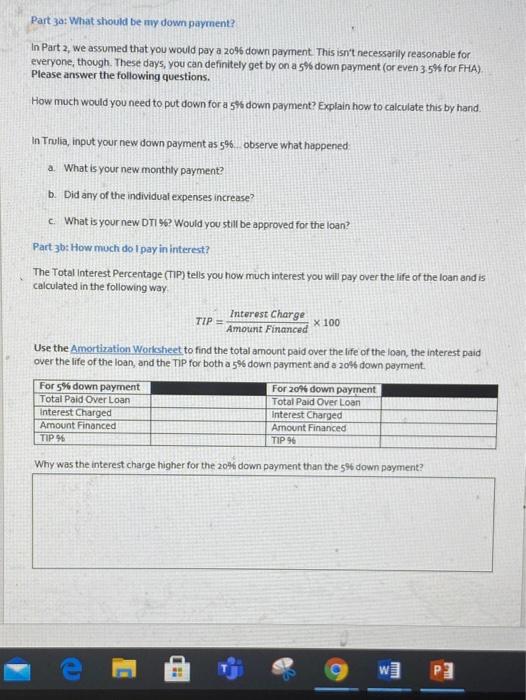

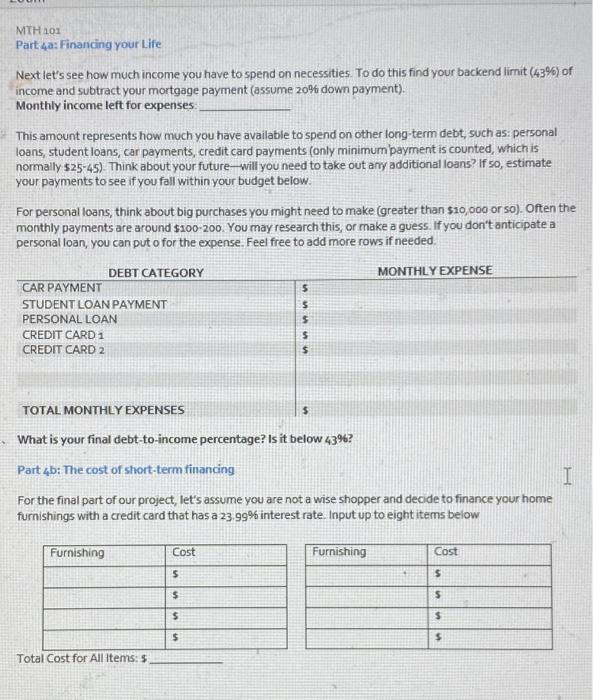

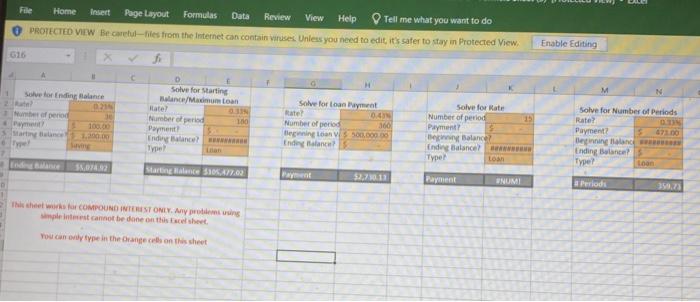

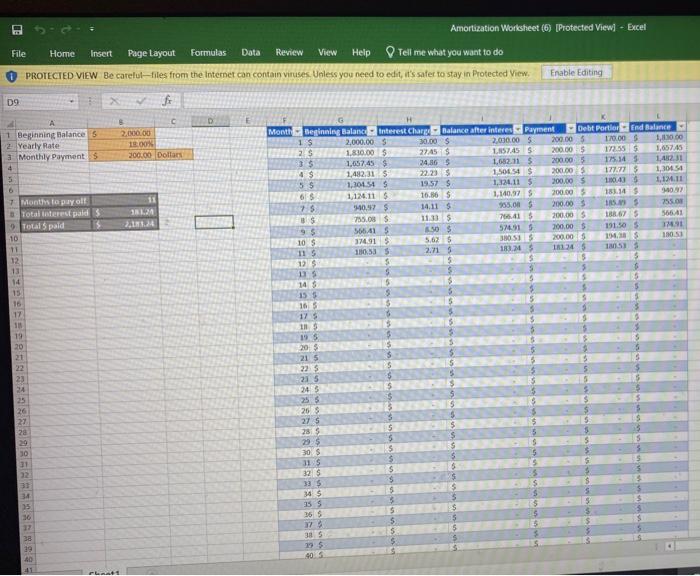

MTH 101 Milestone 1 Worksheet In this milestone, you will learn how to make wise financial decisions Whether you are a recent college graduate or a seasoned professional, you'll be equipped with the knowledge necessary to purchase big ticket items (or share this information with a family member!). Bear in mind that you are not required to submit any personal financial information if you are uncomfortable doing so. You are certainly welcome to fabricate this information if you wish. It may be more interesting to you though if you use accurate information Part 1a: Your Gross Income Imagine that you've just finished your Bachelors with NLU and that you've landed your desired job. You may also currently (or wish to in the future) have a spouse/significant other with whom you might like to purchase the house. Please identify the following: Your desired salary for your dream job): Your spouse/significant other's desired salary (you can also write N/A): Total Gross Income: Monthly Gross Income I Part 1b: What Can You Afford? Debt-To-Income is a measure of your overall debt to how much you make. It is normally written as a percentage and is calculated by the following formula: Monthly Debt DTI % = Monthly Gross Income X 100 Lenders will not allow you to take out a loan if the debt-to-Income percentage is greater than 2896, as you won't be able to afford your home. Explain how to find your maximum DTI ratios below: Assuming a 28% DTI ratio, what is the maximum monthly mortgage payment (eg monthly debt you would be able to take on in order to be approved for a loan (given you meet other underwriting requirements)? Lenders also look at a back-end DTI ratio. This is calculated by adding your mortgage payment and all other monthly debt expenses (car payment, credit card debt, student loans, personal loans) into one combined Monthly Debt value. Your back-end DTI must be less than 4396 to be approved. What is the maramum amount you are able to spend on debt to be approved? Part 2: Your Dream Home Use trulia.com, or some other housing website, to find a home that you would be able to afford (30 yr.). Your monthly payment needs to be less than your 289 DTI percentage from Part B. Assume a 20% down payment and an interest rate of 3.596. Use the housing calculator they provide to assist you. See an example below of what Trulia shows you: Home Pike 52 Down Payment $4,80 20% Interest Rate 3.65% Loon Type 30 yo fed Principatinet Property Tone Home Force More $915 $246 $15 $0 $1,236 Month Get Pre-Qualified or See today's more Please submit information about your dream home below Price of Home Principal and Interest Property Taxes Home Insurance Mortgage Insurance HOA dues (only if buying a condo) Square feet Prke Per Square Foot Link of Your Dream House: Part 3: What should be my down payment? in Part 2, we assumed that you would pay a 20% down payment. This isn't necessarily reasonable for everyone, though. These days, you can definitely get by on a 5% down payment (or even 35% for FHA) Please answer the following questions. How much would you need to put down for a 5% down payment? Explain how to calculate this by hand. In Trulia, input your new down payment as 546. Observe what happened a. What is your new monthly payment? b. Did any of the individual expenses increase? c. What is your new DTI 96? Would you still be approved for the loan? Part 3b: How much do I pay in interest? The Total Interest Percentage (TIP) tells you how much interest you will pay over the life of the loan and is calculated in the following way Interest Charge TIP Amount Financed Use the Amortization Worksheet to find the total amount paid over the life of the loan, the interest paid over the life of the loan, and the TIP for both a 5% down payment and a 20% down payment x 100 For 5% down payment Total Paid Over Loan interest Charged Amount Financed TIP For 20% down payment Total Paid Over Loan Interest Charged Amount Financed TIP 96 Why was the interest charge higher for the 20% down payment than the 5% down payment? e wi P3 MTH 101 Part 4: Financing your Life Next let's see how much income you have to spend on necessities. To do this find your backend limit (43%) of income and subtract your mortgage payment (assume 20% down payment), Monthly income left for expenses This amount represents how much you have available to spend on other long-term debt, such as: personal loans, student loans, car payments, credit card payments (only minimum payment is counted, which is normally 525-45). Think about your future will you need to take out any additional loans? If so, estimate your payments to see if you fall within your budget below. For personal loans, think about big purchases you might need to make (greater than $10,000 or so). Often the monthly payments are around $100-200 You may research this or make a guess. If you don't anticipate a personal loan, you can put o for the expense. Feel free to add more rows if needed. MONTHLY EXPENSE 5 5 DEBT CATEGORY CAR PAYMENT STUDENT LOAN PAYMENT PERSONAL LOAN CREDIT CARD 1 CREDIT CARD 2 M $ TOTAL MONTHLY EXPENSES What is your final debt-to-income percentage? Is it below 4396? Partb: The cost of short-term financing For the final part of our project, let's assume you are not a wise shopper and decide to finance your home furnishings with a credit card that has a 23.99% interest rate. Input up to eight items below I Furnishing Cost Furnishing Cost 5 $ $ $ $ $ $ $ Total Cost for All items: 5 MTH 101 Now many people only pay the minimum payment for their credit cards, which is a huge mistake. Let's assume your minimum payment is 3% of your total cost of items for each month. Given the balance that you just accrued above, let's find the following by using the Module 2 & 3 Forinula Sheet: 1) How long did it take you to pay off your debt? 2) How much did you have to end up paying in total? 3) What was your interest charge? 4) What was your TIP %? Part 5: Reflection Please write at least one full paragraph (4-6 complete sentences) for every question: 1) Why might it be a better idea to wait until you can put a 20% down payment on a house? What might be some of the drawbacks? 2) Some lenders allow you to make additional payments to your mortgage over time. What if you paid an additional $100 per month towards your mortgage? How might that impact your TIP % during the life of the loan? How does compound interest factor into this consideration? 3) Should you finance purchases with credit cards? In what ways do you think credit cards can be useful and how should they be used to prevent hefty interest charges? Is there a correct way to use credit cards? File Home Insert Page Layout Formulas Data Review View Help Tell me what you want to do PROTECTED VIEW Be careful-Hiles from the Internet can contain viruses. Unless you need to edit, it's safer to stay in Protected View 616 Enable Editing 1 So for Ending Balance Solve for starting Blanca/Maimum loan Kate ON berried 100 Payment! Indo Balance Type Nuber of period ment Martin Solve for loan 0. Number of period 300 Geenington 500.000,00 Index tance 15 . Solve for Rate Number of period Payment De Balance Ending Balance Type Loan Solve for Number of Periods Rate? ON Payment? Beginning and Ending Balance Type? Loon Balance Starting Kance SAIZ.02 Fayant $270.13 Payment ENUMI Periods This the works for COMPOUND INTEREST ONLY imple cannot be done on this we shoot You can only type in the range ces on this sheet Amortization Worksheet (6) Protected View] - Excel File Home Insert Page Layout Formulas Data Review View Help Tell me what you want to do PROTECTED VIEW Be carelut-Files from the Internet can contain viruses. Unless you need to edit, it's safer to stay in Protected View f Enable Editing D9 D c 2.000.00 18.00 200.00 Dollars 11 1.21 16WE ISOU 1 Beginning Balance 5 2 Yearly Rate 3 Monthly Payments 4 3 0 7 Months to pay oll Total trest paid Total Spald 10 11 12 13 14 15 15 17 1 19 20 21 22 23 5 $ $ S 5 $ Month Beinnig Balance Interest Charge Balance after interes Payment Debt PortierEnd Balance 1$ 2,000.00 30.00 $ 2,000.00 $ 200.00 5 170.00 $ 1,000.00 2 $ 1.830.00 $ 27455 L5745 200,005 172.555 1,057.45 1,057,45 $ 34,865 1,682,115 200.00 135.14 1.42.31 4. $ 1.482.31 22 23 1.500.54 $ 200.00 177.773 1,30451 5$ 1,301545 19.575 1.12.11 5 300,00 110.43 12 | 6 $ 1,124.11 16.365 1,140.97 200.00 183.14 1403 75 40,97$ 14.115 555.00 $ 200.00 15 255.0 755.08 $ 11.335 765.41 200.00 5 BOYS 566.41 95 566415 SOS 5741 200.00 $ 191.50 $ 10 S 3741 5.625 38051 200.00 1985 115 180.535 2.715 183 INT 12345 12 5 $ S 5 15 5 14 15 5 165 5 175 15 195 20$ $ 21 5 23 5 23 5 243 255 26 $ 3 275 285 20 S 30$ $ S 31 S S $ 32 $ 3 $ 33 $ $ 5 5 $ VE 26 22 28 29 10 31 22 31 5 $ VE St $ SVE S.SE S.SE LE 30 17 38 19 AD 385 29 $ 11 Fle MTH 101 Milestone 1 Worksheet In this milestone, you will learn how to make wise financial decisions Whether you are a recent college graduate or a seasoned professional, you'll be equipped with the knowledge necessary to purchase big ticket items (or share this information with a family member!). Bear in mind that you are not required to submit any personal financial information if you are uncomfortable doing so. You are certainly welcome to fabricate this information if you wish. It may be more interesting to you though if you use accurate information Part 1a: Your Gross Income Imagine that you've just finished your Bachelors with NLU and that you've landed your desired job. You may also currently (or wish to in the future) have a spouse/significant other with whom you might like to purchase the house. Please identify the following: Your desired salary for your dream job): Your spouse/significant other's desired salary (you can also write N/A): Total Gross Income: Monthly Gross Income I Part 1b: What Can You Afford? Debt-To-Income is a measure of your overall debt to how much you make. It is normally written as a percentage and is calculated by the following formula: Monthly Debt DTI % = Monthly Gross Income X 100 Lenders will not allow you to take out a loan if the debt-to-Income percentage is greater than 2896, as you won't be able to afford your home. Explain how to find your maximum DTI ratios below: Assuming a 28% DTI ratio, what is the maximum monthly mortgage payment (eg monthly debt you would be able to take on in order to be approved for a loan (given you meet other underwriting requirements)? Lenders also look at a back-end DTI ratio. This is calculated by adding your mortgage payment and all other monthly debt expenses (car payment, credit card debt, student loans, personal loans) into one combined Monthly Debt value. Your back-end DTI must be less than 4396 to be approved. What is the maramum amount you are able to spend on debt to be approved? Part 2: Your Dream Home Use trulia.com, or some other housing website, to find a home that you would be able to afford (30 yr.). Your monthly payment needs to be less than your 289 DTI percentage from Part B. Assume a 20% down payment and an interest rate of 3.596. Use the housing calculator they provide to assist you. See an example below of what Trulia shows you: Home Pike 52 Down Payment $4,80 20% Interest Rate 3.65% Loon Type 30 yo fed Principatinet Property Tone Home Force More $915 $246 $15 $0 $1,236 Month Get Pre-Qualified or See today's more Please submit information about your dream home below Price of Home Principal and Interest Property Taxes Home Insurance Mortgage Insurance HOA dues (only if buying a condo) Square feet Prke Per Square Foot Link of Your Dream House: Part 3: What should be my down payment? in Part 2, we assumed that you would pay a 20% down payment. This isn't necessarily reasonable for everyone, though. These days, you can definitely get by on a 5% down payment (or even 35% for FHA) Please answer the following questions. How much would you need to put down for a 5% down payment? Explain how to calculate this by hand. In Trulia, input your new down payment as 546. Observe what happened a. What is your new monthly payment? b. Did any of the individual expenses increase? c. What is your new DTI 96? Would you still be approved for the loan? Part 3b: How much do I pay in interest? The Total Interest Percentage (TIP) tells you how much interest you will pay over the life of the loan and is calculated in the following way Interest Charge TIP Amount Financed Use the Amortization Worksheet to find the total amount paid over the life of the loan, the interest paid over the life of the loan, and the TIP for both a 5% down payment and a 20% down payment x 100 For 5% down payment Total Paid Over Loan interest Charged Amount Financed TIP For 20% down payment Total Paid Over Loan Interest Charged Amount Financed TIP 96 Why was the interest charge higher for the 20% down payment than the 5% down payment? e wi P3 MTH 101 Part 4: Financing your Life Next let's see how much income you have to spend on necessities. To do this find your backend limit (43%) of income and subtract your mortgage payment (assume 20% down payment), Monthly income left for expenses This amount represents how much you have available to spend on other long-term debt, such as: personal loans, student loans, car payments, credit card payments (only minimum payment is counted, which is normally 525-45). Think about your future will you need to take out any additional loans? If so, estimate your payments to see if you fall within your budget below. For personal loans, think about big purchases you might need to make (greater than $10,000 or so). Often the monthly payments are around $100-200 You may research this or make a guess. If you don't anticipate a personal loan, you can put o for the expense. Feel free to add more rows if needed. MONTHLY EXPENSE 5 5 DEBT CATEGORY CAR PAYMENT STUDENT LOAN PAYMENT PERSONAL LOAN CREDIT CARD 1 CREDIT CARD 2 M $ TOTAL MONTHLY EXPENSES What is your final debt-to-income percentage? Is it below 4396? Partb: The cost of short-term financing For the final part of our project, let's assume you are not a wise shopper and decide to finance your home furnishings with a credit card that has a 23.99% interest rate. Input up to eight items below I Furnishing Cost Furnishing Cost 5 $ $ $ $ $ $ $ Total Cost for All items: 5 MTH 101 Now many people only pay the minimum payment for their credit cards, which is a huge mistake. Let's assume your minimum payment is 3% of your total cost of items for each month. Given the balance that you just accrued above, let's find the following by using the Module 2 & 3 Forinula Sheet: 1) How long did it take you to pay off your debt? 2) How much did you have to end up paying in total? 3) What was your interest charge? 4) What was your TIP %? Part 5: Reflection Please write at least one full paragraph (4-6 complete sentences) for every question: 1) Why might it be a better idea to wait until you can put a 20% down payment on a house? What might be some of the drawbacks? 2) Some lenders allow you to make additional payments to your mortgage over time. What if you paid an additional $100 per month towards your mortgage? How might that impact your TIP % during the life of the loan? How does compound interest factor into this consideration? 3) Should you finance purchases with credit cards? In what ways do you think credit cards can be useful and how should they be used to prevent hefty interest charges? Is there a correct way to use credit cards? File Home Insert Page Layout Formulas Data Review View Help Tell me what you want to do PROTECTED VIEW Be careful-Hiles from the Internet can contain viruses. Unless you need to edit, it's safer to stay in Protected View 616 Enable Editing 1 So for Ending Balance Solve for starting Blanca/Maimum loan Kate ON berried 100 Payment! Indo Balance Type Nuber of period ment Martin Solve for loan 0. Number of period 300 Geenington 500.000,00 Index tance 15 . Solve for Rate Number of period Payment De Balance Ending Balance Type Loan Solve for Number of Periods Rate? ON Payment? Beginning and Ending Balance Type? Loon Balance Starting Kance SAIZ.02 Fayant $270.13 Payment ENUMI Periods This the works for COMPOUND INTEREST ONLY imple cannot be done on this we shoot You can only type in the range ces on this sheet Amortization Worksheet (6) Protected View] - Excel File Home Insert Page Layout Formulas Data Review View Help Tell me what you want to do PROTECTED VIEW Be carelut-Files from the Internet can contain viruses. Unless you need to edit, it's safer to stay in Protected View f Enable Editing D9 D c 2.000.00 18.00 200.00 Dollars 11 1.21 16WE ISOU 1 Beginning Balance 5 2 Yearly Rate 3 Monthly Payments 4 3 0 7 Months to pay oll Total trest paid Total Spald 10 11 12 13 14 15 15 17 1 19 20 21 22 23 5 $ $ S 5 $ Month Beinnig Balance Interest Charge Balance after interes Payment Debt PortierEnd Balance 1$ 2,000.00 30.00 $ 2,000.00 $ 200.00 5 170.00 $ 1,000.00 2 $ 1.830.00 $ 27455 L5745 200,005 172.555 1,057.45 1,057,45 $ 34,865 1,682,115 200.00 135.14 1.42.31 4. $ 1.482.31 22 23 1.500.54 $ 200.00 177.773 1,30451 5$ 1,301545 19.575 1.12.11 5 300,00 110.43 12 | 6 $ 1,124.11 16.365 1,140.97 200.00 183.14 1403 75 40,97$ 14.115 555.00 $ 200.00 15 255.0 755.08 $ 11.335 765.41 200.00 5 BOYS 566.41 95 566415 SOS 5741 200.00 $ 191.50 $ 10 S 3741 5.625 38051 200.00 1985 115 180.535 2.715 183 INT 12345 12 5 $ S 5 15 5 14 15 5 165 5 175 15 195 20$ $ 21 5 23 5 23 5 243 255 26 $ 3 275 285 20 S 30$ $ S 31 S S $ 32 $ 3 $ 33 $ $ 5 5 $ VE 26 22 28 29 10 31 22 31 5 $ VE St $ SVE S.SE S.SE LE 30 17 38 19 AD 385 29 $ 11 Fle

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts