Question: Multiple Choice : Choose the best possible answer. Please be guided by the INSTRUCTIONS given in this material. Include solution for the problems. 1. Daffodil

Multiple Choice :

Choose the best possible answer. Please be guided by the INSTRUCTIONS given in this material. Include solution for the problems.

1. Daffodil Corporation, requires a minimum return on investment of 8% for any project to be carried out by the company. The company is decentralized and investment decisions are up to the judgment of the division managers as long as this ROI level is realized. Plant Division, has had a return on investment of 14% for the division for the past 3 years and believes the division continues to have the same return in the coming year .It also has the opportunity to invest in a new product that is projected to have an ROI of 12%. If Daffodil Corporation evaluates managerial performance using return on investment, what will be the preference for taking on the proposed new product?

a. Daffodil will accept / Plant will reject

b. Daffodil will reject / Plant will accept

c. Daffodil will accept / Plant will accept

d. Daffodil will reject / Plant will reject

e. cannot be determined with the data given

2. Monstera Company's Adansoni Division has the following accounts last year:Sales ...P480,000 ; Cost of goods sold...P222,000; Selling and administrative expense ...P210,000; Income tax rate 30% ; Total capital employed ... P300,000. Monstera Company's actual cost of capital is 10 percent. The value added returns amounts to P3,650.

a. None of the above.

b. True

c. False

3. Division A of Coleus Group had investments at the year end of P56,000,000which includes a new equipment costing P3 million acquired two weeks before the end of the year. This equipment was paid for by the Head Office Finance Unit of Coleus, and is recorded in the accounts as an inter-company loan.The profit of division A for the year was P7 million before deducting head office allocated cost of P800,000. The most suitable rate of ROI for Division A for the year is ?

a. 11.07%

b. 13.2%

c. 11.7%

d. 12.5%

4. Choose the option that best describes the statements below.

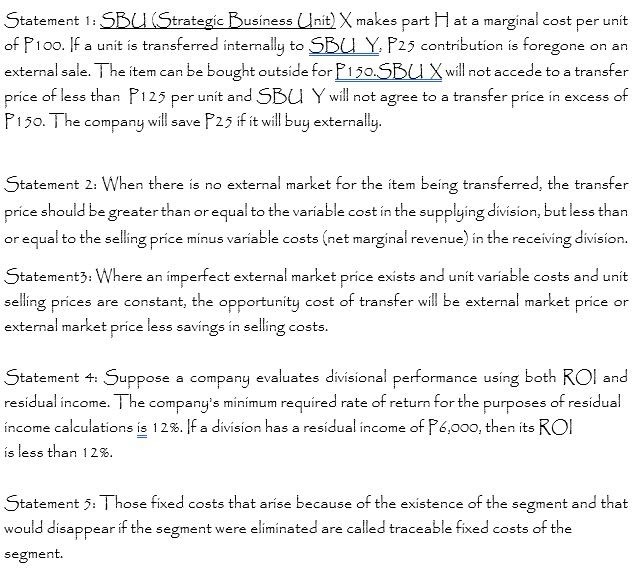

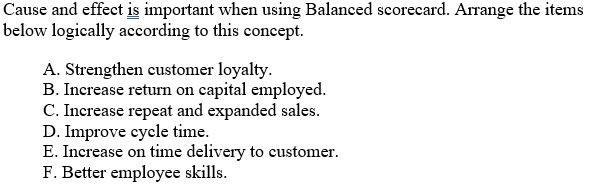

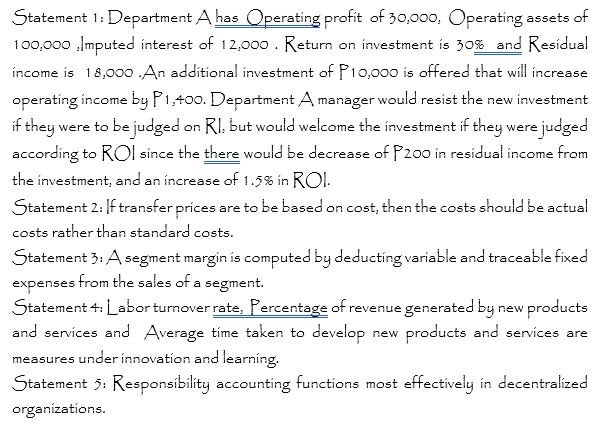

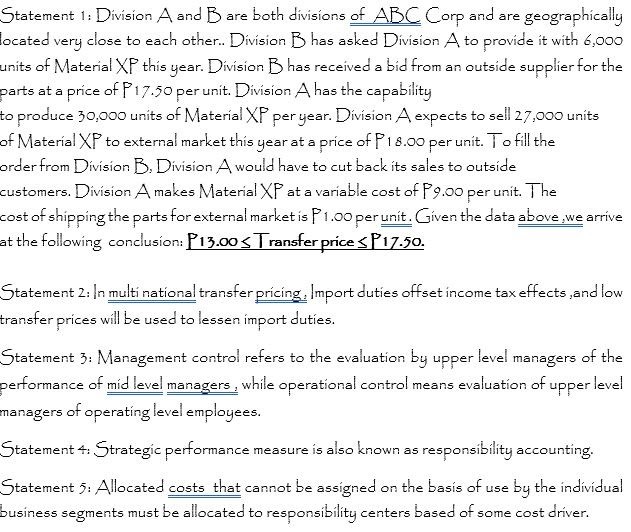

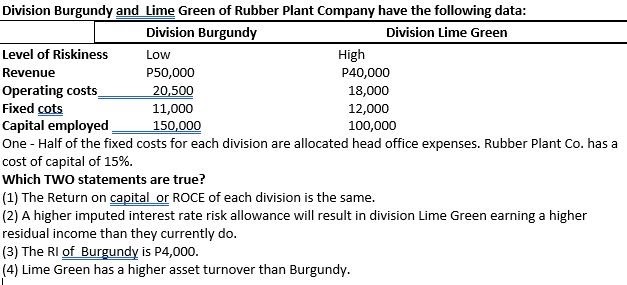

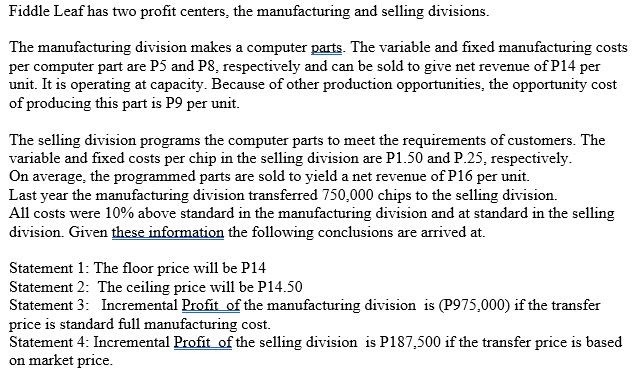

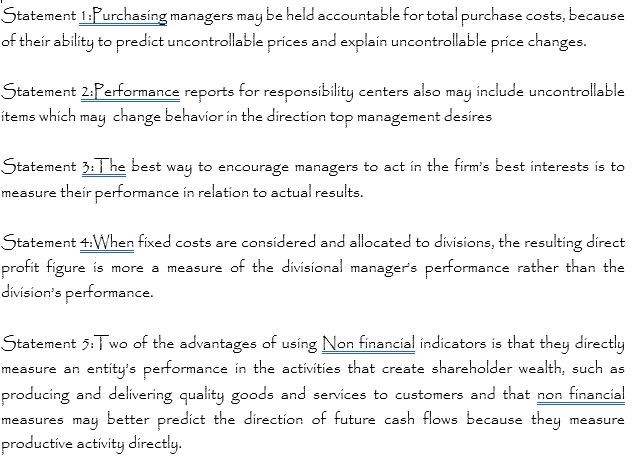

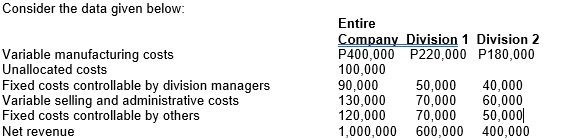

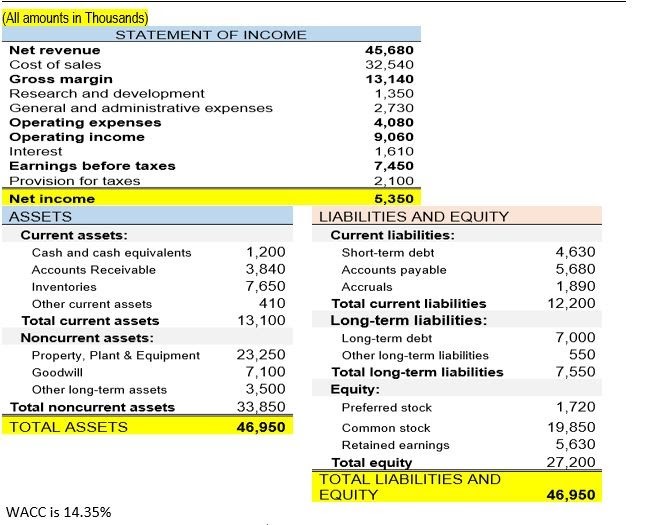

Statement 1: SB(1(Strategic Business (Init) X makes part | at a marginal cost per unit of Floo. If a unit is transferred internally to SBC Y, P25 contribution is foregone on an external sale. The item can be bought outside for F1 50.5D(| X will not accede to a transfer price of less than P125 per unit and SDU Y will not agree to a transfer price in excess of F150. The company will save P25 if it will buy externally. Statement 2: When there is no external market for the item being transferred, the transfer price should be greater than or equal to the variable cost in the supplying division, but less than or equal to the selling price minus variable costs ( net marginal revenue) in the receiving division. Statement3: Where an imperfect external market price exists and unit variable costs and unit selling prices are constant, the opportunity cost of transfer will be external market price or external market price less savings in selling costs. Statement 4: Suppose a company evaluates divisional performance using both ROI and residual income. ] he company's minimum required rate of return for the purposes of residual income calculations is 12%. If a division has a residual income of F6,000, then its ROI is less than 12%. Statement 5: Those fixed costs that arise because of the existence of the segment and that would disappear if the segment were eliminated are called traceable fixed costs of the segment.Cause and effect E important when using Balanced scorecard. Arrange the items blw logically according to this concept. A. Strengthen customer loyalty. 13. Increase return on capital employed. C. Increase repeat and expanded sales. Dr. Improve cycle time. E. Increase on time delivery to customer. F. Better employee skills. Which TWO of the following assertions about the balanced scorecard are correct? (a) Each of the perspectives are independent of one another. (b) To be successful, the measures included in the scorecard should be limited in number, fairly consistent and ranked in some order of significance. (c) BSC promotes that management focus on the short term. (d) The financial data included within the balanced scorecard is limited.Mama Mary Loves You Hospital is using Balanced Scorecard. Which 2 of the measures below fall under the internal process perspective of a balanced scorecard? (1) Employee attrition [2) Treatment oversights per dose. (3) Patient contentment more than 97%. (4) % of patients attended to within 15 minutes upon arrival.Statement 1: Department A has Operating profit of 30,000, Operating assets of 100,000 ,Imputed interest of 12,000 . Return on investment is 30% and Residual income is 18,000 .An additional investment of P10,000 is offered that will increase operating income by 1,400. Department A manager would resist the new investment if they were to be judged on RI, but would welcome the investment if they were judged according to ROI since the there would be decrease of F200 in residual income from the investment, and an increase of 1.5% in ROI. Statement 2: If transfer prices are to be based on cost, then the costs should be actual costs rather than standard costs. Statement 3: A segment margin is computed by deducting variable and traceable fixed expenses from the sales of a segment. Statement 4: Labor turnover rate, Percentage of revenue generated by new products and services and Average time taken to develop new products and services are measures under innovation and learning. Statement 5: Responsibility accounting functions most effectively in decentralized organizations.Statement 1: Division A and B are both divisions of ABC Corp and are geographically ocated very close to each other.. Division D has asked Division A to provide it with 6,000 units of Material XP this year. Division B has received a bid from an outside supplier for the parts at a price of F17.50 per unit. Division A has the capability to produce 30,000 units of Material XP per year. Division A expects to sell 27,000 units of Material XP to external market this year at a price of P1 8.00 per unit. To fill the order from Division B. Division A would have to cut back its sales to outside customers. Division A makes Material XP at a variable cost of F9.00 per unit. The cost of shipping the parts for external market is F1.00 perunit. Given the data above we arrive at the following conclusion: P13.00 S Transfer price $ P17.50. Statement 2: In multi national transfer pricing, Import duties offset income tax effects , and low transfer prices will be used to lessen import duties. Statement 3: Management control refers to the evaluation by upper level managers of the performance of mid level managers , while operational control means evaluation of upper level managers of operating level employees. Statement 4: Strategic performance measure is also known as responsibility accounting. Statement 5: Allocated costs that cannot be assigned on the basis of use by the individual business segments must be allocated to responsibility centers based of some cost driver.Division Burgundy and Lime Green of Rubber Plant Company have the following data: Division Burgundy Division Lime Green Level of Riskiness LOW High Revenue P50,000 P40,000 Operating costs 20,500 18,000 Fixed cots 11,000 12,000 Capital employed 150,000 100,000 One - Half of the fixed costs for each division are allocated head office expenses. Rubber Plant Co. has a cost of capital of 15%. Which TWO statements are true? (1) The Return on capital or ROCE of each division is the same. [2) A higher imputed interest rate risk allowance will result in division Lime Green earning a higher residual income than they currently do. (3) The RI of Burgundy is P4,000. (4) Lime Green has a higher asset turnover than Burgundy.Fiddle Leaf has two profit centers, the manufacturing and selling divisions. The manufacturing division makes a computer parts. The variable and fixed manufacturing costs per computer part are P5 and P8, respectively and can be sold to give net revenue of P14 per unit. It is operating at capacity. Because of other production opportunities, the opportunity cost of producing this part is P9 per unit. The selling division programs the computer parts to meet the requirements of customers. The variable and fixed costs per chip in the selling division are P1.50 and P.25, respectively. On average, the programmed parts are sold to yield a net revenue of P16 per unit. Last year the manufacturing division transferred 750,000 chips to the selling division. All costs were 10% above standard in the manufacturing division and at standard in the selling division. Given these information the following conclusions are arrived at. Statement 1: The floor price will be P14 Statement 2: The ceiling price will be P14.50 Statement 3: Incremental Profit of the manufacturing division is (P975,000) if the transfer price is standard full manufacturing cost. Statement 4: Incremental Profit of the selling division is P187,500 if the transfer price is based on market price.Statement 1:Purchasing managers may be held accountable for total purchase costs, because of their ability to predict uncontrollable prices and explain uncontrollable price changes. Statement 2:Performance reports for responsibility centers also may include uncontrollable items which may change behavior in the direction top management desires Statement 3: | he best way to encourage managers to act in the firm's best interests is to measure their performance in relation to actual results. Statement 4:When fixed costs are considered and allocated to divisions, the resulting direct profit figure is more a measure of the divisional manager's performance rather than the division's performance. Statement 5: Two of the advantages of using Non financial indicators is that they directly measure an entity's performance in the activities that create shareholder wealth, such as producing and delivering quality goods and services to customers and that non financial measures may better predict the direction of future cash flows because they measure productive activity directly.Consider the data given below: Entire Company Division 1 Division 2 Variable manufacturing costs P400,000 P220,000 P180,000 Unallocated costs 100.000 Fixed costs controllable by division managers 90.000 50,000 40,000 Variable selling and administrative costs 130,000 70,000 60,000 Fixed costs controllable by others 120,000 70,000 50,000 Net revenue 1,000,000 600,000 400,000Choose the best answer Statement 1:Return on investment (KO)) encourages managers to accept all investment decisions that will benefit the company as a whole when it is used as a measure of performance. Statement 2: The selling division in a transfer pricing situation would want the transfer price to be set to cover at least the full cost per unit plus the lost contribution margin per unit on outside sales. Statement 3:All profit centers are responsibility centers, but not all responsibility centers are profit centers. Statement :A company has two divisions, each selling several product lines. If Segment reports are prepared at the product line level, the division managers' salaries would be considered as common fixed costs of the product lines. Statement 5: Transfer prices based on standard cost provide an incentive for the receiving division to control costs.(All amounts in Thousands) STATEMENT OF INCOME Net revenue 45,680 Cost of sales 32,540 Gross margin 13,140 Research and development 1,350 General and administrative expenses 2,730 Operating expenses 4,080 Operating income 9,060 Interest 1,610 Earnings before taxes 7,450 Provision for taxes 2,100 Net income 6,350 ASSETS LIABILITIES AND EQUITY Current assets: Current liabilities: Cash and cash equivalents 1,200 Short-term debt 4,630 Accounts Receivable 3,840 Accounts payable 5,680 Inventories 7,650 Accruals 1,890 Other current assets 410 Total current liabilities 12,200 Total current assets 13, 100 Long-term liabilities: Noncurrent assets: Long-term debt 7,000 Property, Plant & Equipment 23,250 Other long-term liabilities 550 Goodwill 7,100 Total long-term liabilities 7,550 Other long-term assets 3,500 Equity: Total noncurrent assets 33,850 Preferred stock 1,720 TOTAL ASSETS 46,950 Common stock 19,850 Retained earnings 5,630 Total equity 27,200 TOTAL LIABILITIES AND EQUITY 46,950 WACC is 14.35%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts