Question: mULTIPLE cHOICE. PRovide Solution Chapter Book Value per Share, and Earnings per Share 383 MC 9-6 The shareholders' equity section of GGG Corp. as of

mULTIPLE cHOICE. PRovide Solution

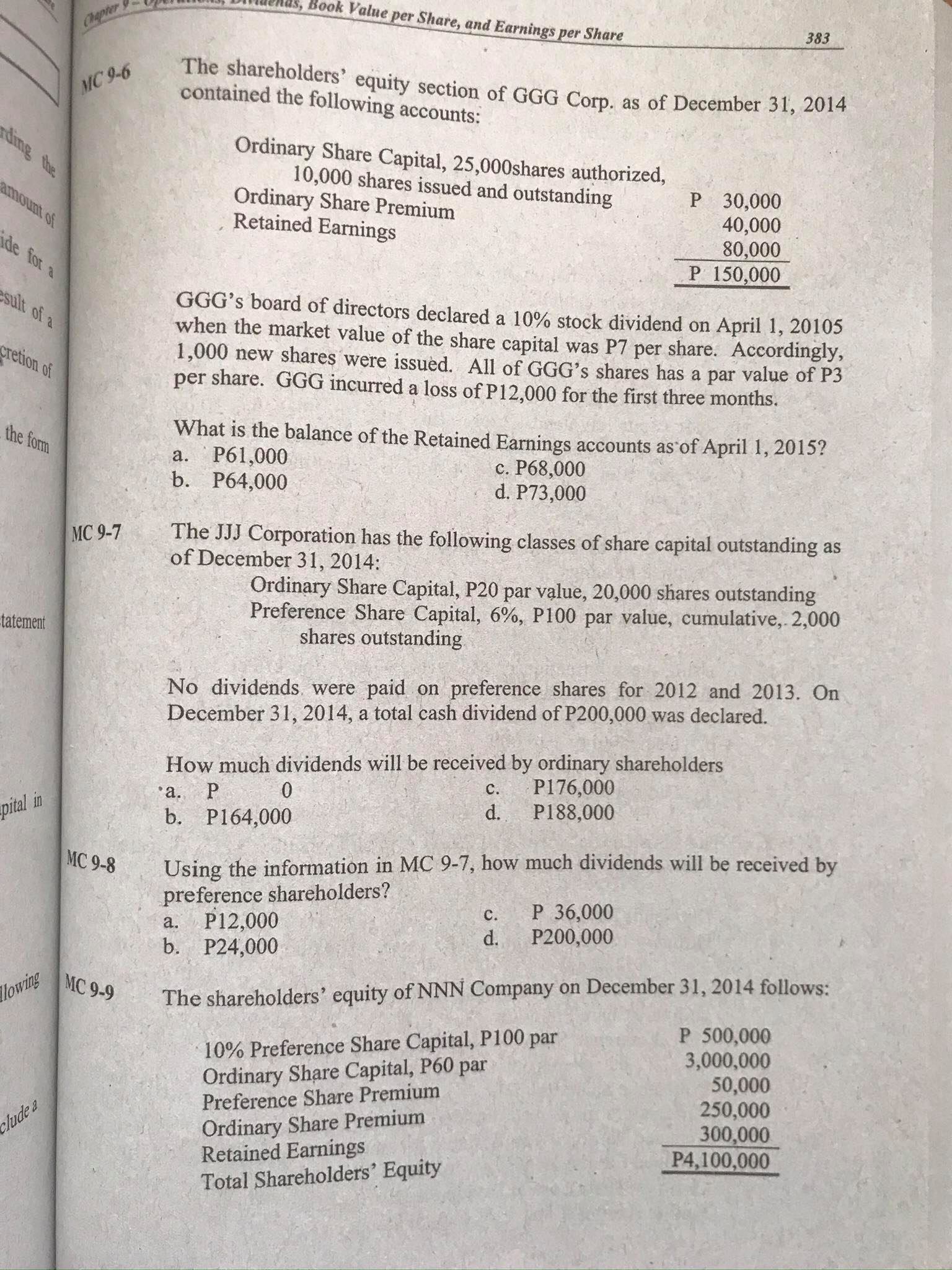

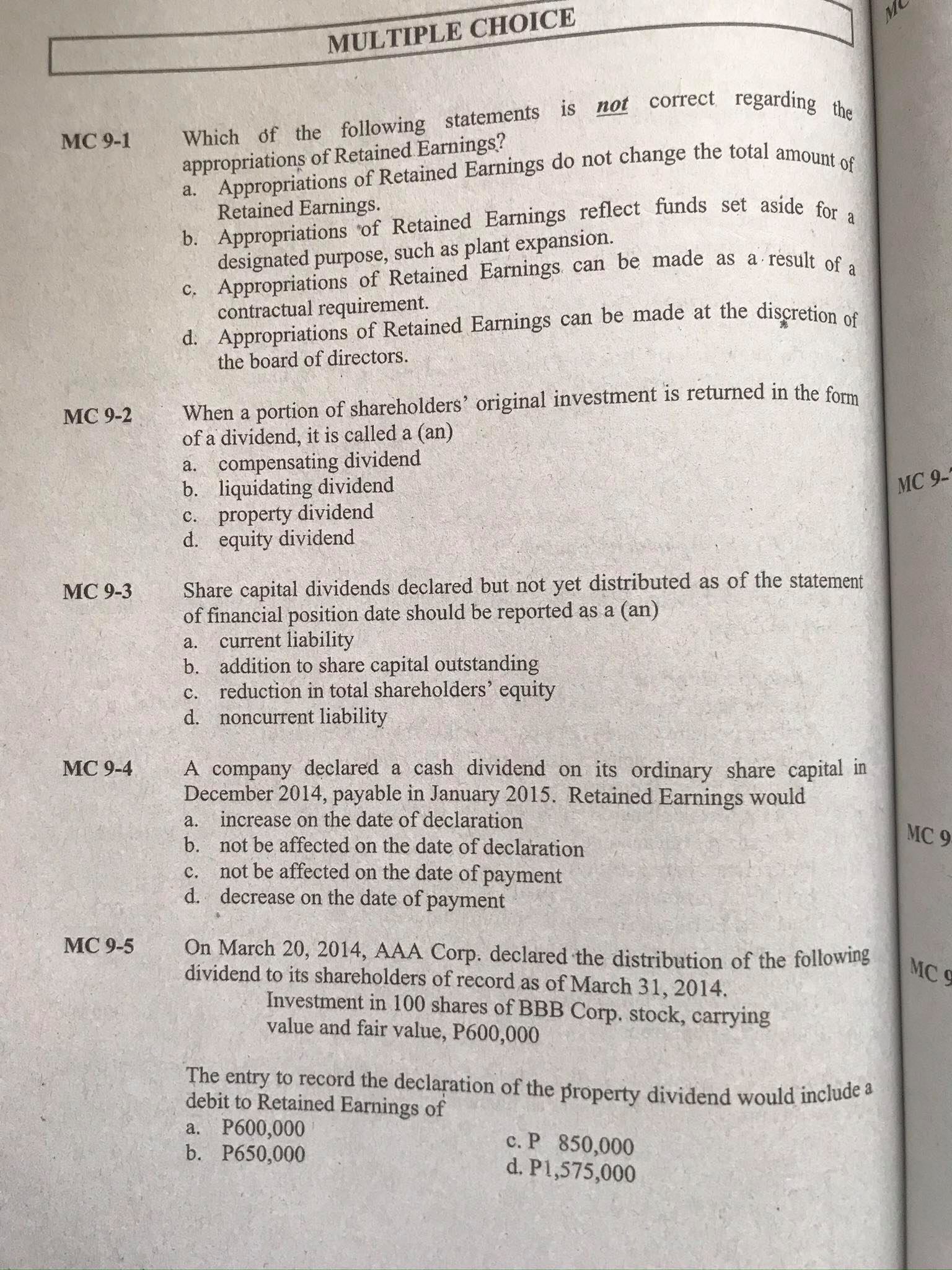

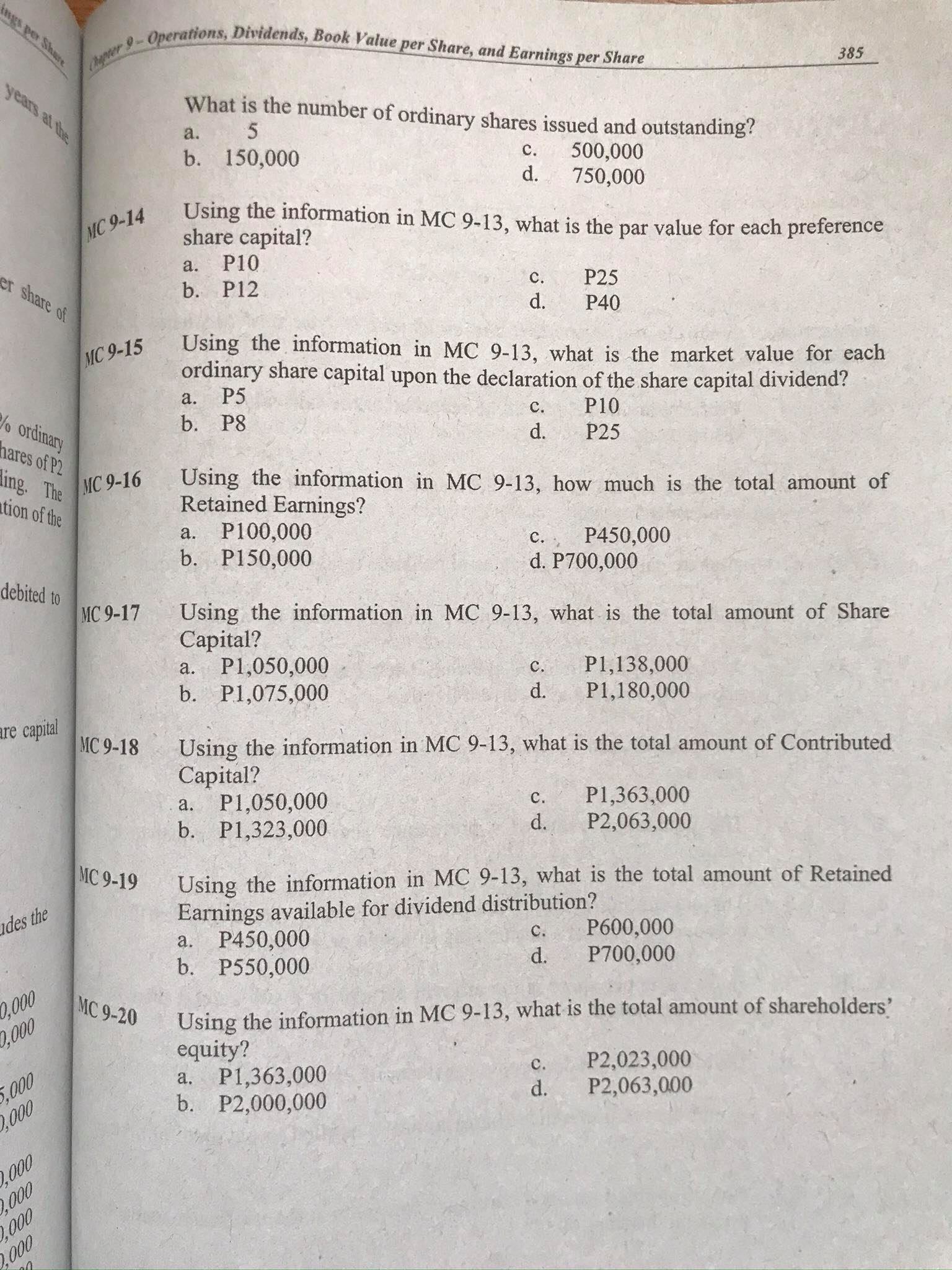

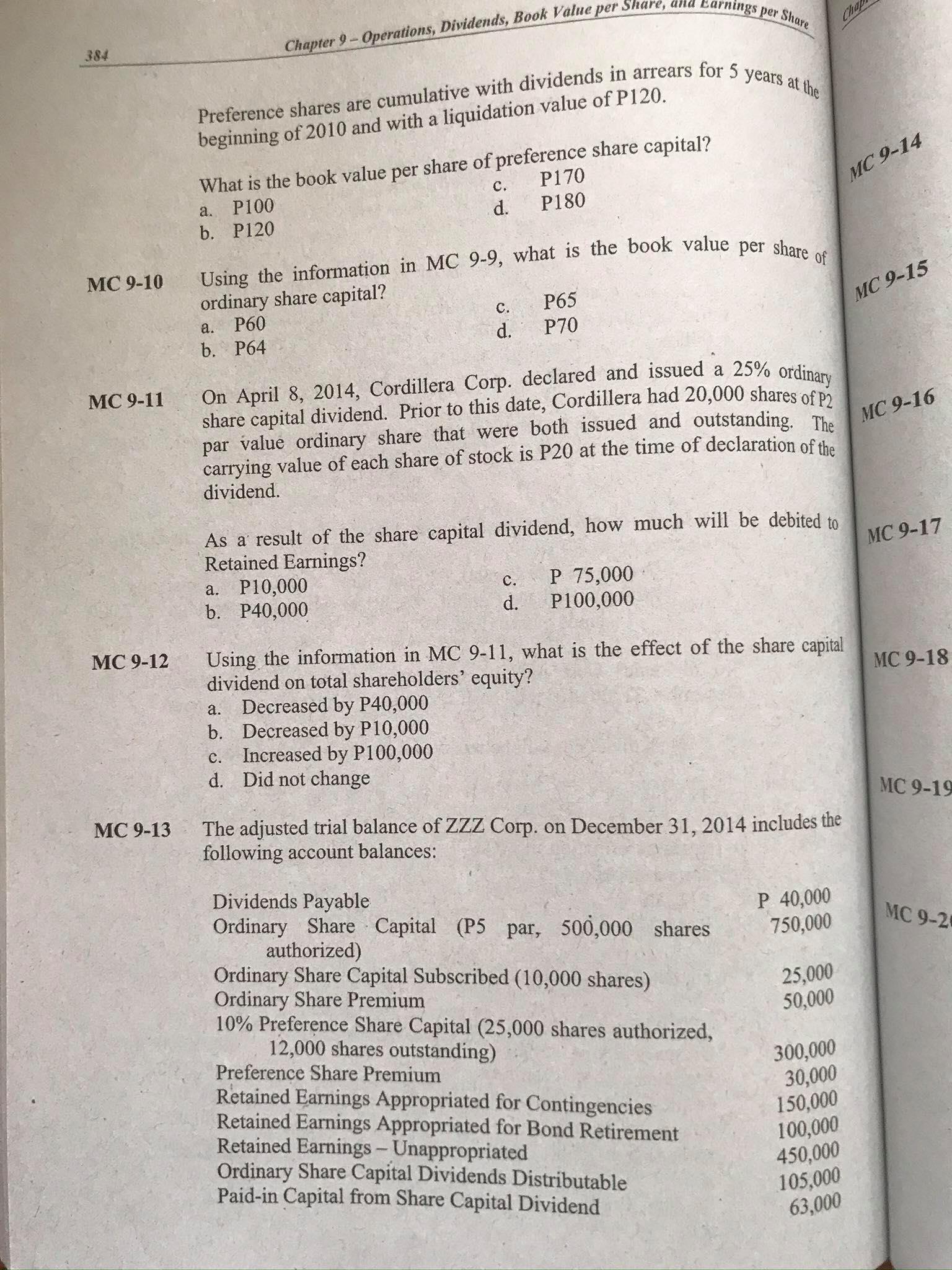

Chapter Book Value per Share, and Earnings per Share 383 MC 9-6 The shareholders' equity section of GGG Corp. as of December 31, 2014 contained the following accounts: ding the Ordinary Share Capital, 25,000shares authorized, 10,000 shares issued and outstanding amount of Ordinary Share Premium P 30,000 Retained Earnings 40,000 de for a 80,000 P 150,000 sult of a GGG's board of directors declared a 10% stock dividend on April 1, 20105 when the market value of the share capital was P7 per share. Accordingly, cretion of 1,000 new shares were issued. All of GGG's shares has a par value of P3 per share. GGG incurred a loss of P12,000 for the first three months. the form a. P61,000 What is the balance of the Retained Earnings accounts as of April 1, 2015? b. P64,000 c. P68,000 d. P73,000 MC 9-7 The JJJ Corporation has the following classes of share capital outstanding as of December 31, 2014: Ordinary Share Capital, P20 par value, 20,000 shares outstanding tatement Preference Share Capital, 6%, P100 par value, cumulative, 2,000 shares outstanding No dividends were paid on preference shares for 2012 and 2013. On December 31, 2014, a total cash dividend of P200,000 was declared. How much dividends will be received by ordinary shareholders a. P 0 C. P176,000 pital in b. P164,000 d. P188,000 MC 9-8 Using the information in MC 9-7, how much dividends will be received by preference shareholders? a. P12,000 C. P 36,000 b. P24,000 d. P200,000 lowing MC 9-9 The shareholders' equity of NNN Company on December 31, 2014 follows: 10% Preference Share Capital, P100 par P 500,000 Ordinary Share Capital, P60 par 3,000,000 clude a Preference Share Premium 50,000 Ordinary Share Premium 250,000 300,000 Retained Earnings Total Shareholders' Equity P4,100,000MULTIPLE CHOICE MC 9-1 Which of the following statements is not correct regarding the appropriations of Retained Earnings? a. Appropriations of Retained Earnings do not change the total amount of Retained Earnings. b. Appropriations of Retained Earnings reflect funds set aside for a designated purpose, such as plant expansion. C. Appropriations of Retained Earnings can be made as a result of a contractual requirement. d. Appropriations of Retained Earnings can be made at the discretion of the board of directors. MC 9-2 When a portion of shareholders' original investment is returned in the form of a dividend, it is called a (an) a. compensating dividend b. liquidating dividend MC 9- c. property dividend d. equity dividend MC 9-3 Share capital dividends declared but not yet distributed as of the statement of financial position date should be reported as a (an) a. current liability b. addition to share capital outstanding c. reduction in total shareholders' equity d. noncurrent liability MC 9-4 A company declared a cash dividend on its ordinary share capital in December 2014, payable in January 2015. Retained Earnings would a. increase on the date of declaration b. not be affected on the date of declaration MC 9 c. not be affected on the date of payment d. decrease on the date of payment MC 9-5 On March 20, 2014, AAA Corp. declared the distribution of the following dividend to its shareholders of record as of March 31, 2014. MC Investment in 100 shares of BBB Corp. stock, carrying value and fair value, P600,000 The entry to record the declaration of the property dividend would include a debit to Retained Earnings of 1. P600,000 b. P650,000 C. P 850,000 d. P1,575,000yes per Share 9- Operations, Dividends, Book Value per Share, and Earnings per Share 385 years at the a. What is the number of ordinary shares issued and outstanding? 5 b. 150,000 C. 500,000 d. 750,000 MC 9-14 Using the information in MC 9-13, what is the par value for each preference share capital? a. P10 er share of b. P12 C. d. P25 P40 MC 9-15 Using the information in MC 9-13, what is the market value for each a. P5 ordinary share capital upon the declaration of the share capital dividend? b. P8 P10 o ordinary d. P25 ares of P2 ling. The MC 9-16 Using the information in MC 9-13, how much is the total amount of tion of the Retained Earnings? a. P100,000 b. P150,000 C . . P450,000 d. P700,000 debited to MC 9-17 Using the information in MC 9-13, what is the total amount of Share Capital? a. P1,050,000 P1, 138,000 b. P1,075,000 C. d. P1,180,000 re capital MC 9-18 Using the information in MC 9-13, what is the total amount of Contributed Capital? a. P1,050,000 C. P1,363,000 b. P1,323,000 d . P2,063,000 MC 9-19 Using the information in MC 9-13, what is the total amount of Retained ides the Earnings available for dividend distribution? a. P450,000 C. P600,000 b. P550,000 d. P700,000 0,000 0.000 MC 9-20 Using the information in MC 9-13, what is the total amount of shareholders' equity? P2,023,000 $,000 a. P1,363,000 C. d. ,000 b. P2,000,000 P2,063,000 000 000 2.000 000Chapter 9 - Operations, Dividends, Book Value per Share 384 nings per Share Preference shares are cumulative with dividends in arrears for 5 years at the beginning of 2010 and with a liquidation value of P120. What is the book value per share of preference share capital? MC 9-14 a. P100 C . P170 b. P120 d. P180 MC 9-10 Using the information in MC 9-9, what is the book value per share of ordinary share capital? a. P60 P65 MC 9-15 b. P64 d. P70 MC 9-11 On April 8, 2014, Cordillera Corp. declared and issued a 25% ordinary share capital dividend. Prior to this date, Cordillera had 20,000 shares of P2 par value ordinary share that were both issued and outstanding. The MC 9-16 carrying value of each share of stock is P20 at the time of declaration of the dividend. As a result of the share capital dividend, how much will be debited to Retained Earnings? MC 9-17 a. P10,000 b. P40,000 C. P 75,000 d. P100,000 MC 9-12 Using the information in MC 9-11, what is the effect of the share capital dividend on total shareholders' equity? MC 9-18 a. Decreased by P40,000 b. Decreased by P10,000 c. Increased by P100,000 d. Did not change MC 9-13 MC 9-19 The adjusted trial balance of ZZZ Corp. on December 31, 2014 includes the following account balances: Dividends Payable Ordinary Share Capital (P5 par, 500,000 shares P 40,000 authorized) 750,000 MC 9-2 Ordinary Share Capital Subscribed (10,000 shares) Ordinary Share Premium 25,000 10% Preference Share Capital (25,000 shares authorized, 50,000 12,000 shares outstanding) Preference Share Premium 300,000 Retained Earnings Appropriated for Contingencies 30,000 Retained Earnings Appropriated for Bond Retirement 150,000 Retained Earnings - Unappropriated 100,000 Ordinary Share Capital Dividends Distributable 450,000 Paid-in Capital from Share Capital Dividend 105,000 63,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts