Question: Multiple choice question: A risk manager would like to simulate the price of a stock using the discretized GBN'I, where with and a denote, respectively,

Multiple choice question:

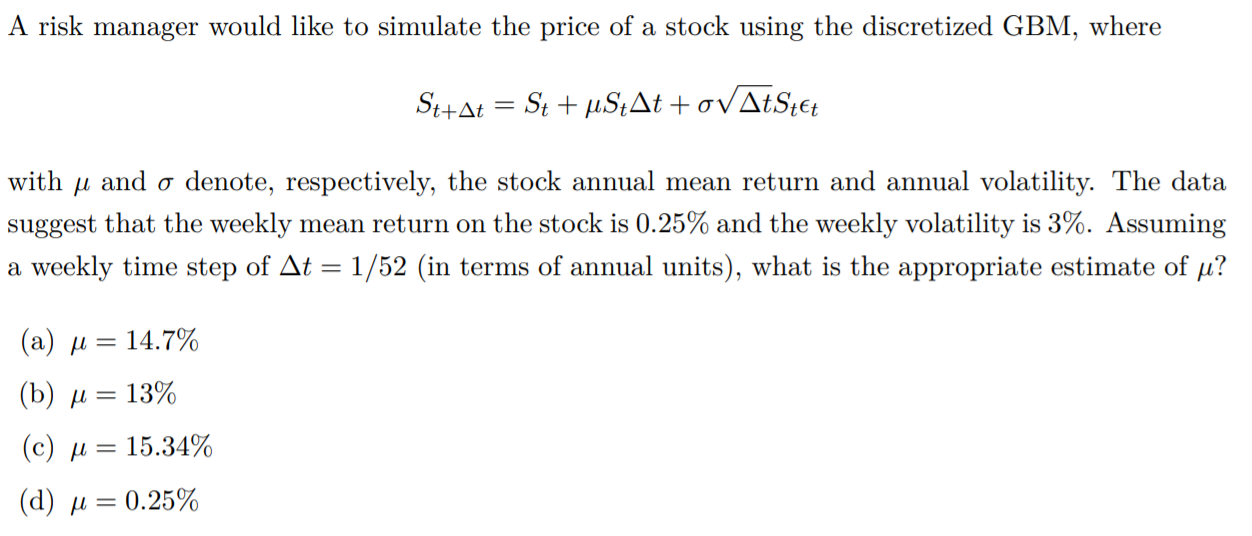

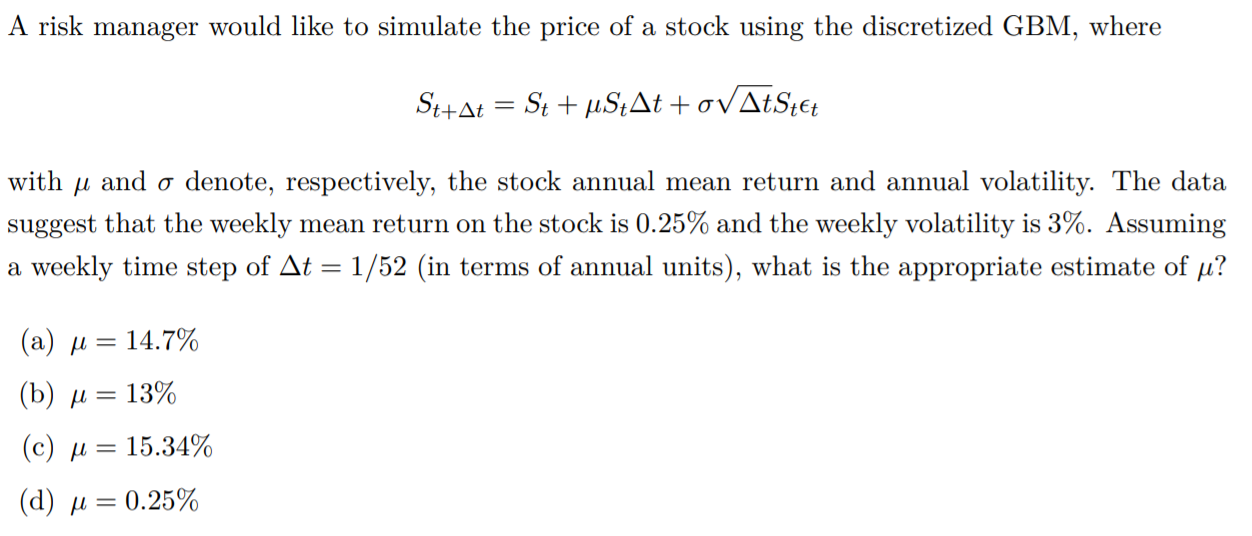

A risk manager would like to simulate the price of a stock using the discretized GBN'I, where with and a denote, respectively, the stock annual mean return and annual volatility. The data suggest that the weekly mean return on the stock is 0.25% and the weekly volatility is 3%. Assuming a weekly time step of At 1/52 (in terms of annual units), what is the appropriate estimate of p? (b) 13% (a) (c) (d) p = 14.7% 15.34% 0.25%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock