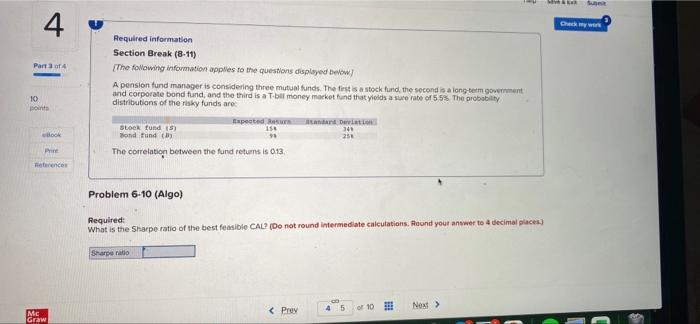

Question: MY & 4 Part 4 10 points Required information Section Break (8-11) The following information applies to the questions displayed below) A pension fund manager

MY & 4 Part 4 10 points Required information Section Break (8-11) The following information applies to the questions displayed below) A pension fund manager is considering three mutual funds. The first is a stock fund the second is a long term government and corporate bond fund, and the third is a T-bil money market and that yields a sure rate of 55% The probably distributions of the risky funds are Tapete Devo Stok fund 150 341 Mond und 91 25 The correlation between the fund returns is 013 Book Pre encos Problem 6-10 (Algo) Required: What is the Sharpe ratio of the best feasible CAL? (Do not round intermediate calculations. Round your answer to decimale) Sharpe ratio of 1081 Next >

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts