Question: My question is both C and D . do not answer A and B! I got the answer below, but have no idea how to

My question is both C and D. do not answer A and B!

I got the answer below, but have no idea how to solve them

Please show me the steps on how to solve them

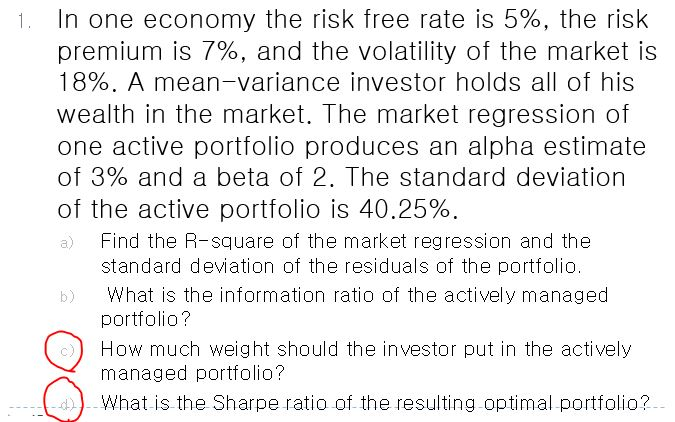

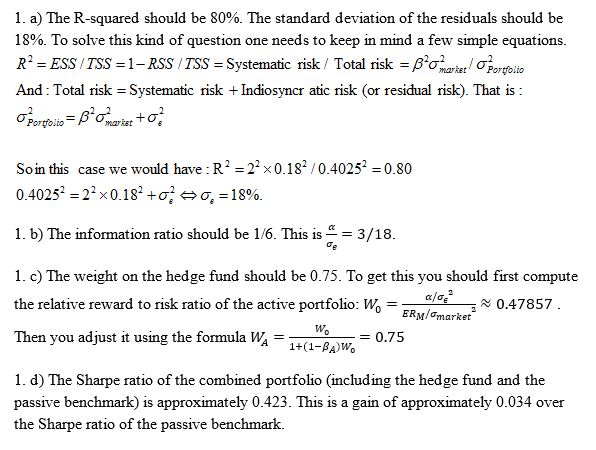

1. In one economy the risk free rate is 5%, the risk premium is 7%, and the volatility of the market is 18%. A mean-variance investor holds all of his wealth in the market. The market regression of one active portfolio produces an alpha estimate of 3% and a beta of 2. The standard deviation of the active portfolio is 40.25% a) Find the R-square of the market regression and the standard deviation of the residuals of the portfolio. b) What is the information ratio of the actively managed portfolio? How much weight should the investor put in the actively managed portfolio? d) What is the Sharpe ratio of the resulting optimal portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts