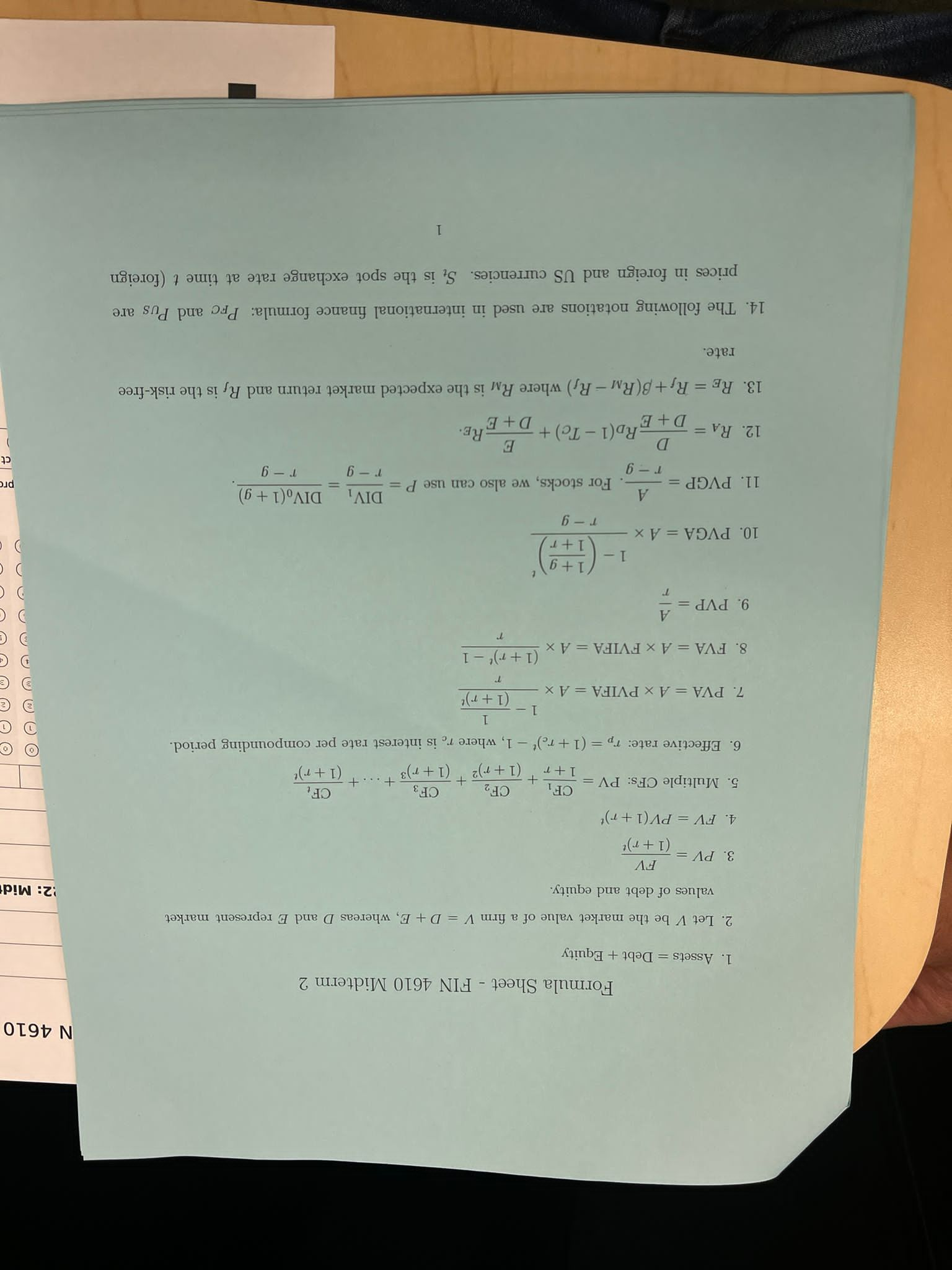

Question: N 4610 Formula Sheet - FIN 4610 Midterm 2 1. Assets = Debt + Equity 2. Let V be the market value of a firm

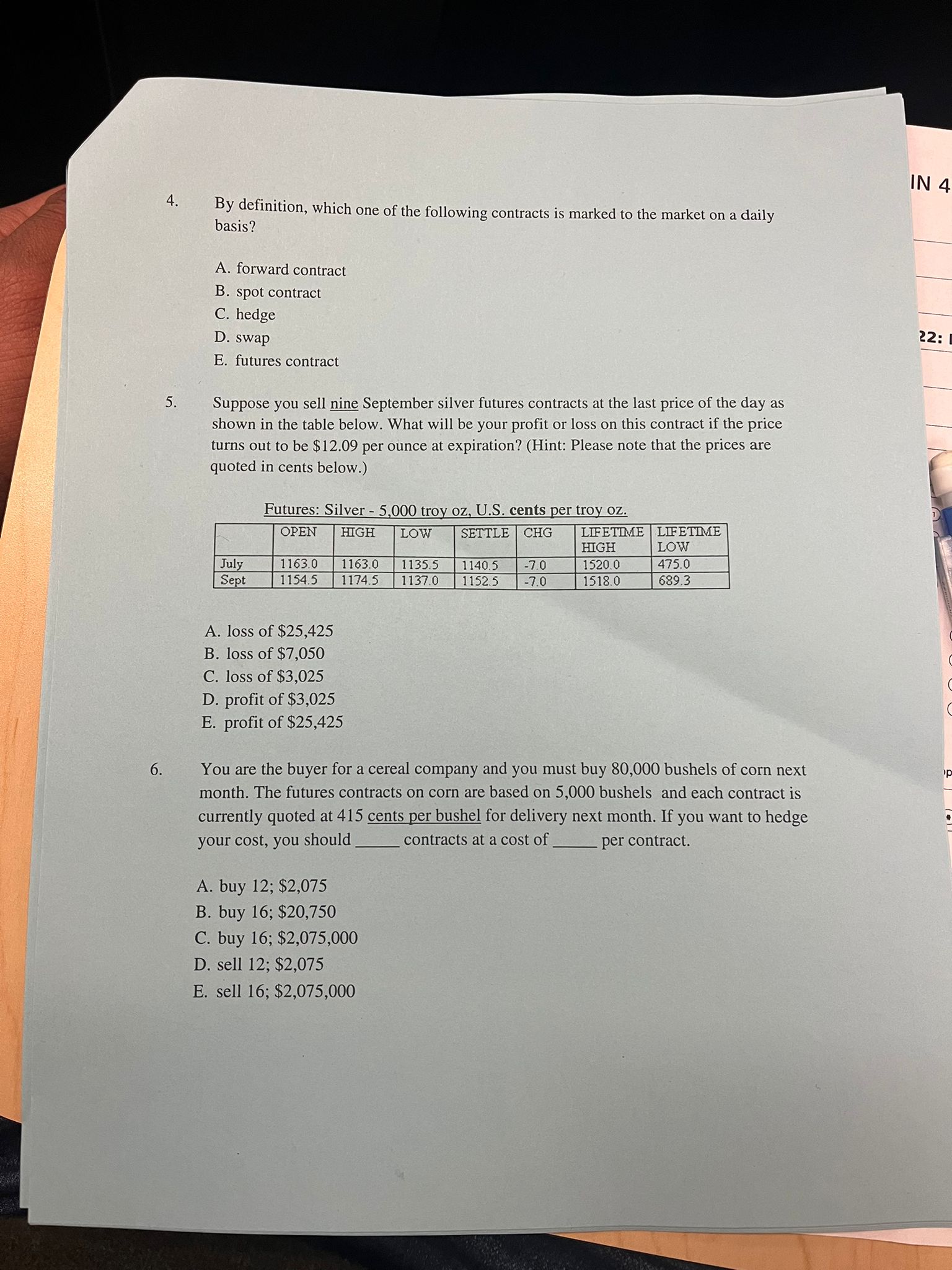

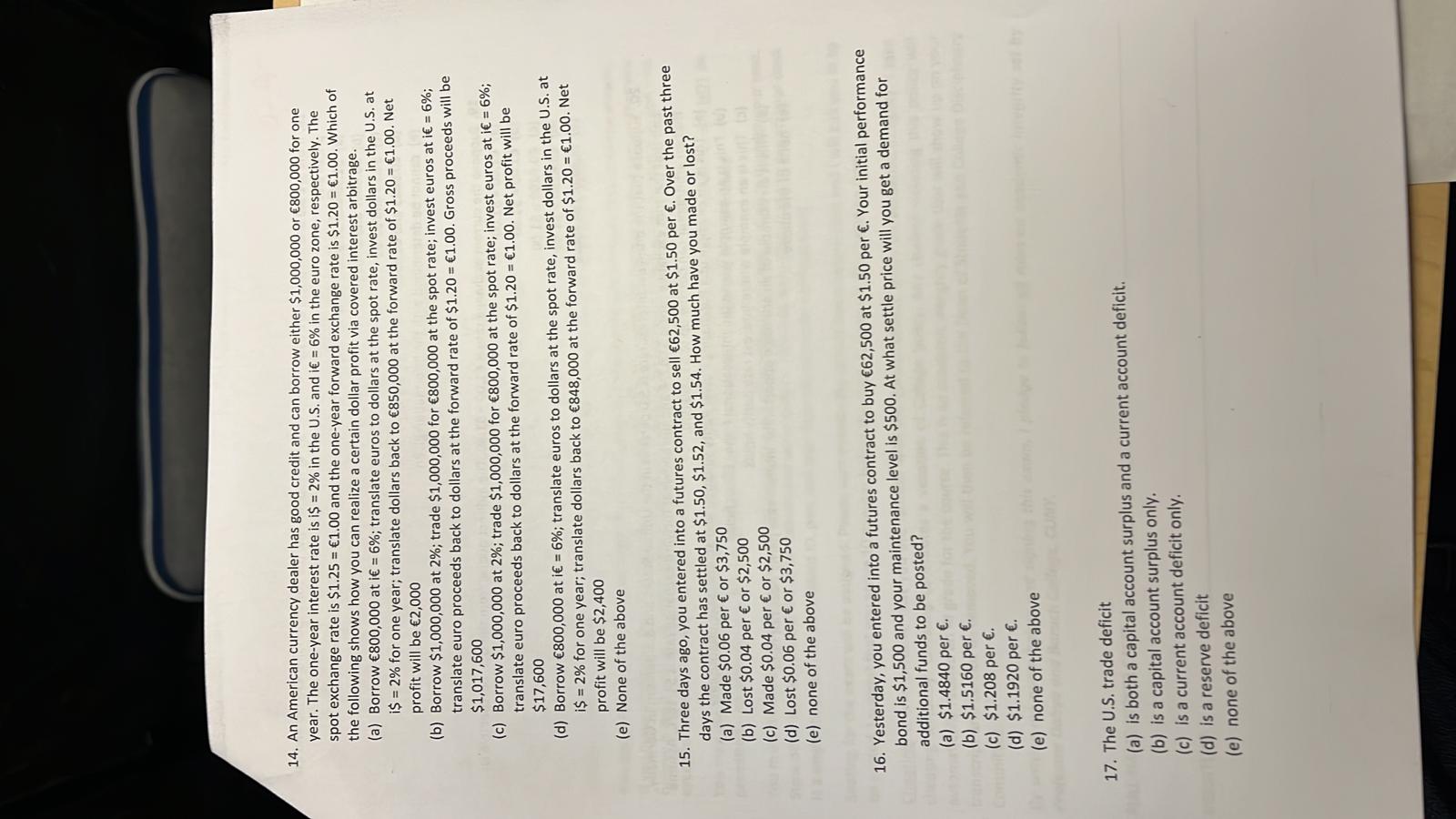

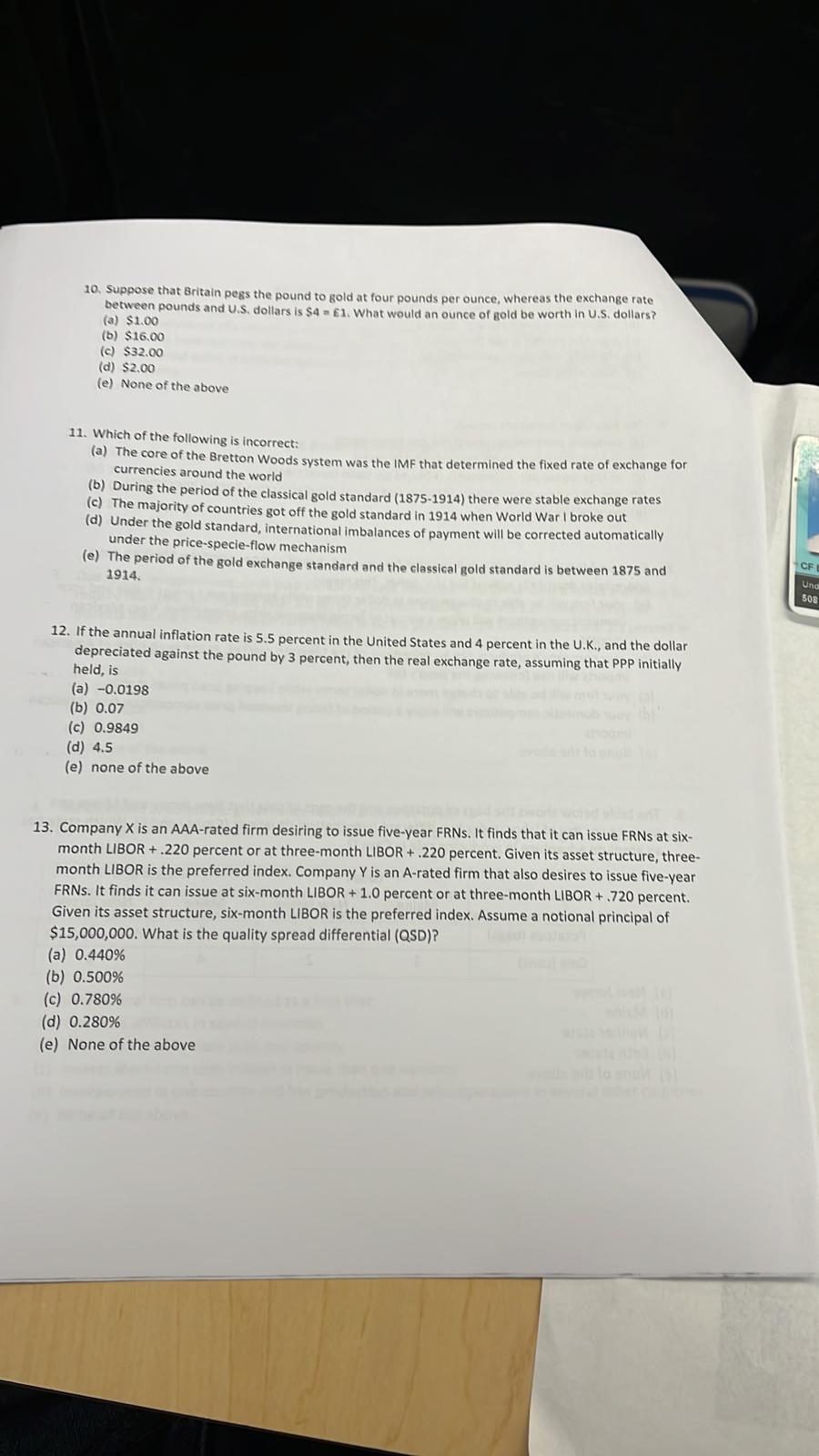

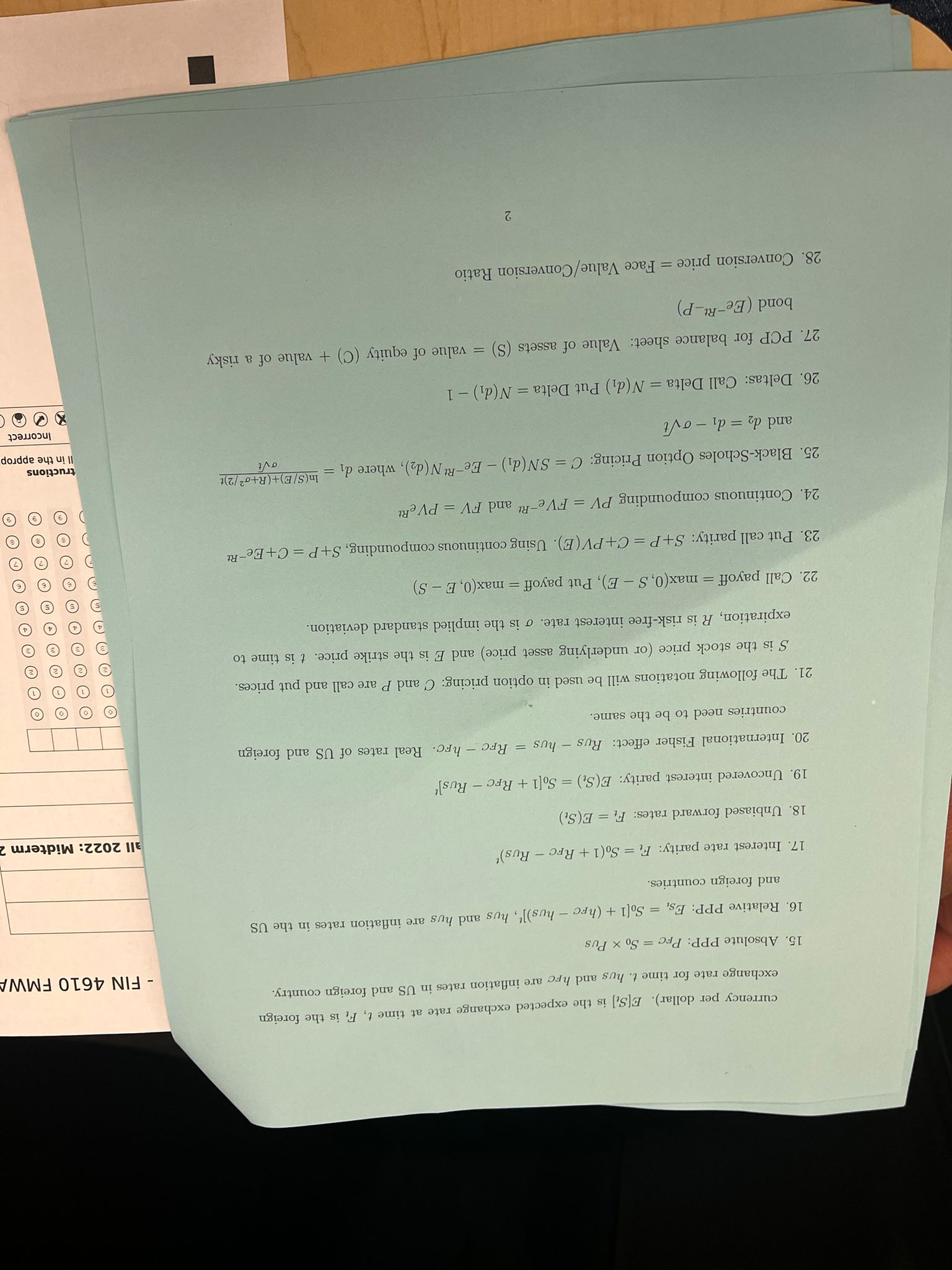

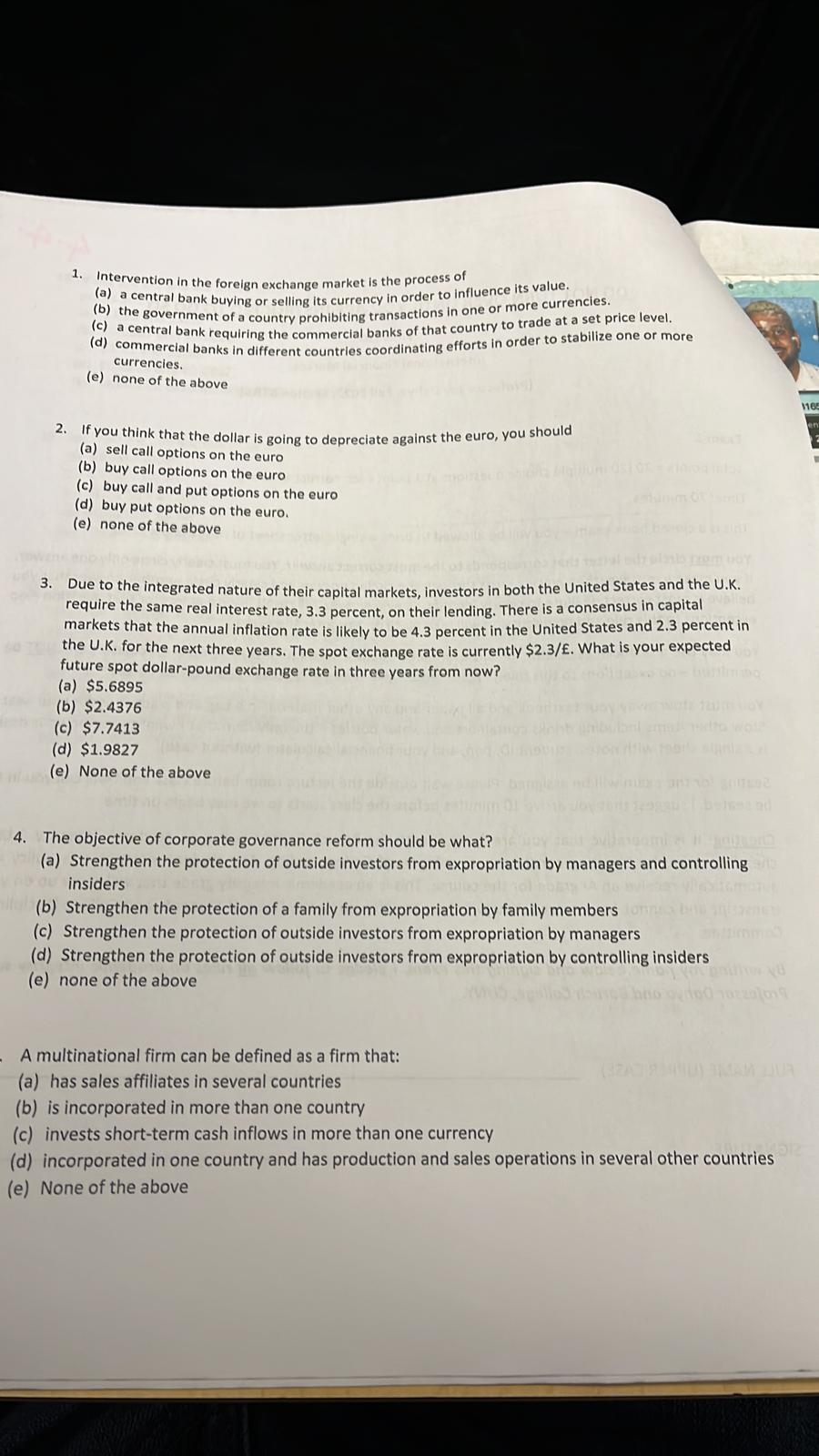

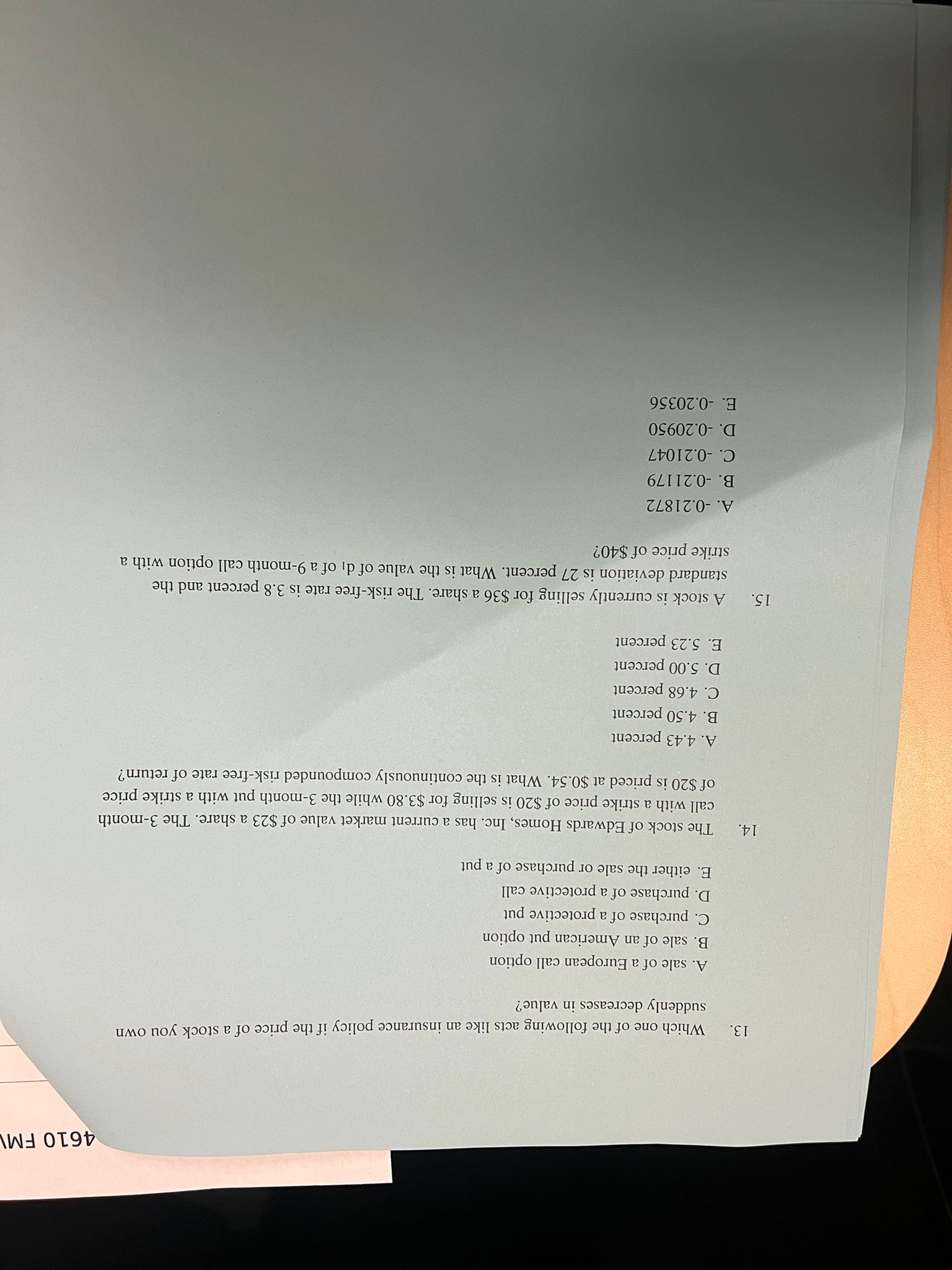

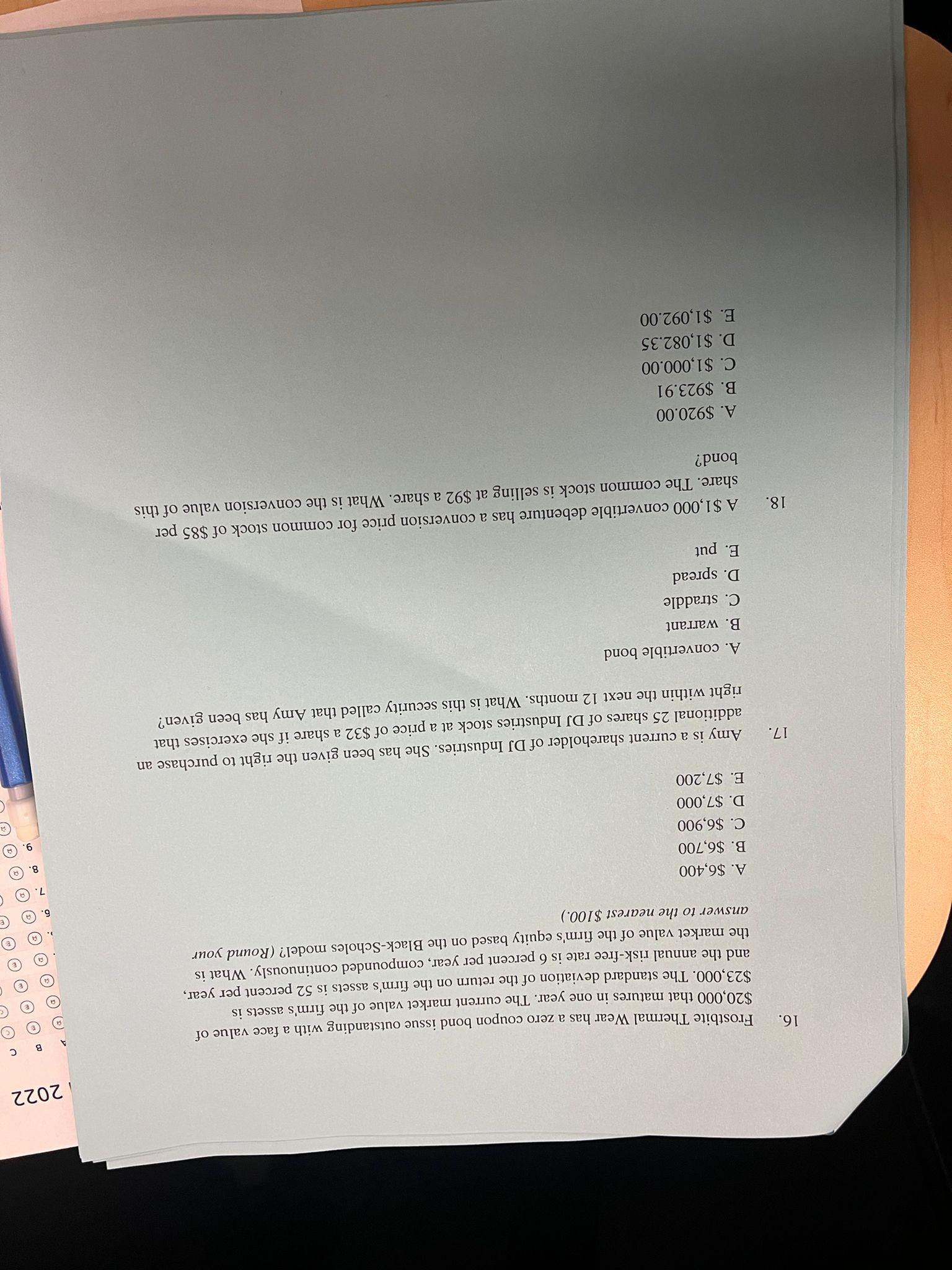

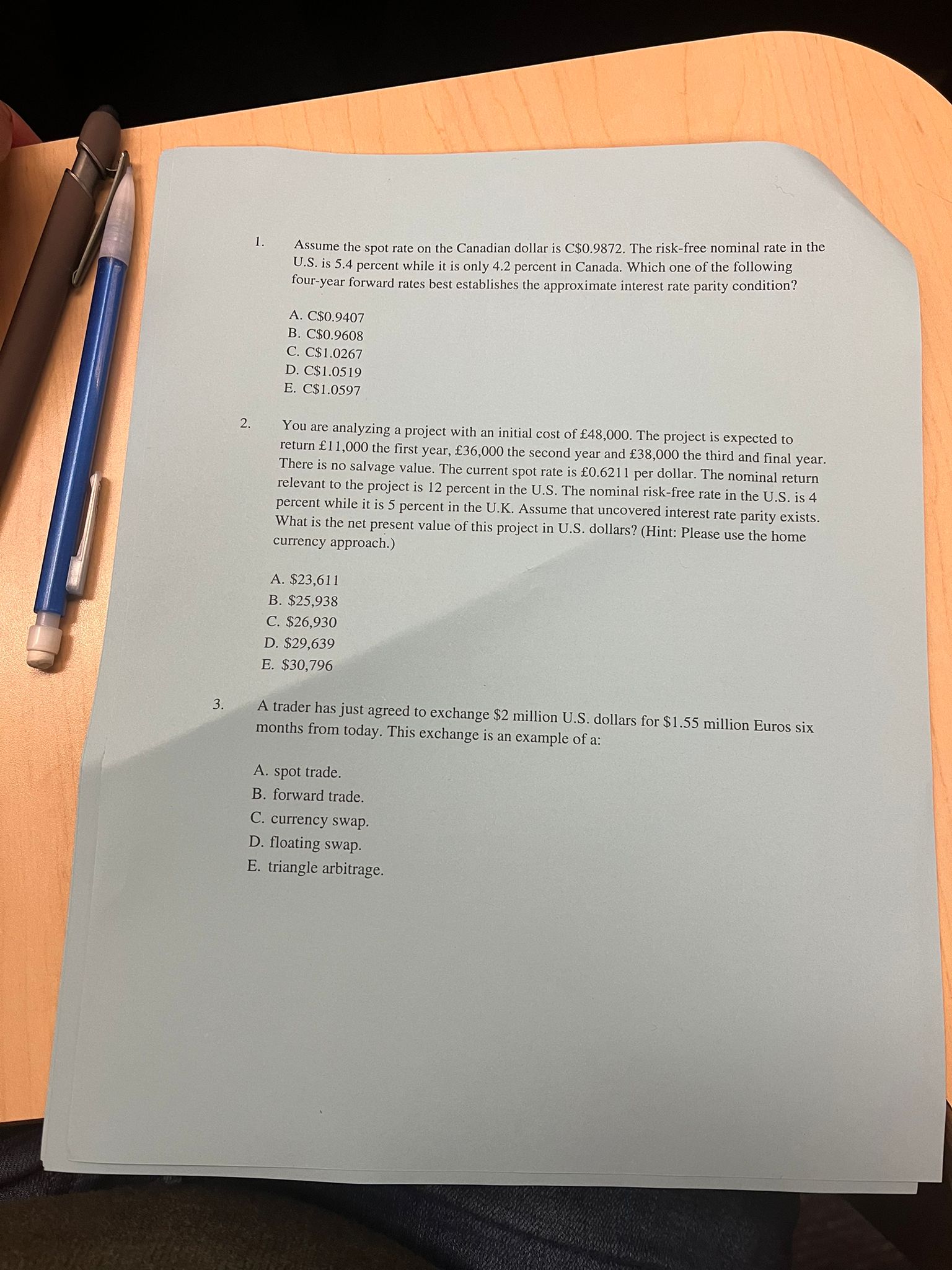

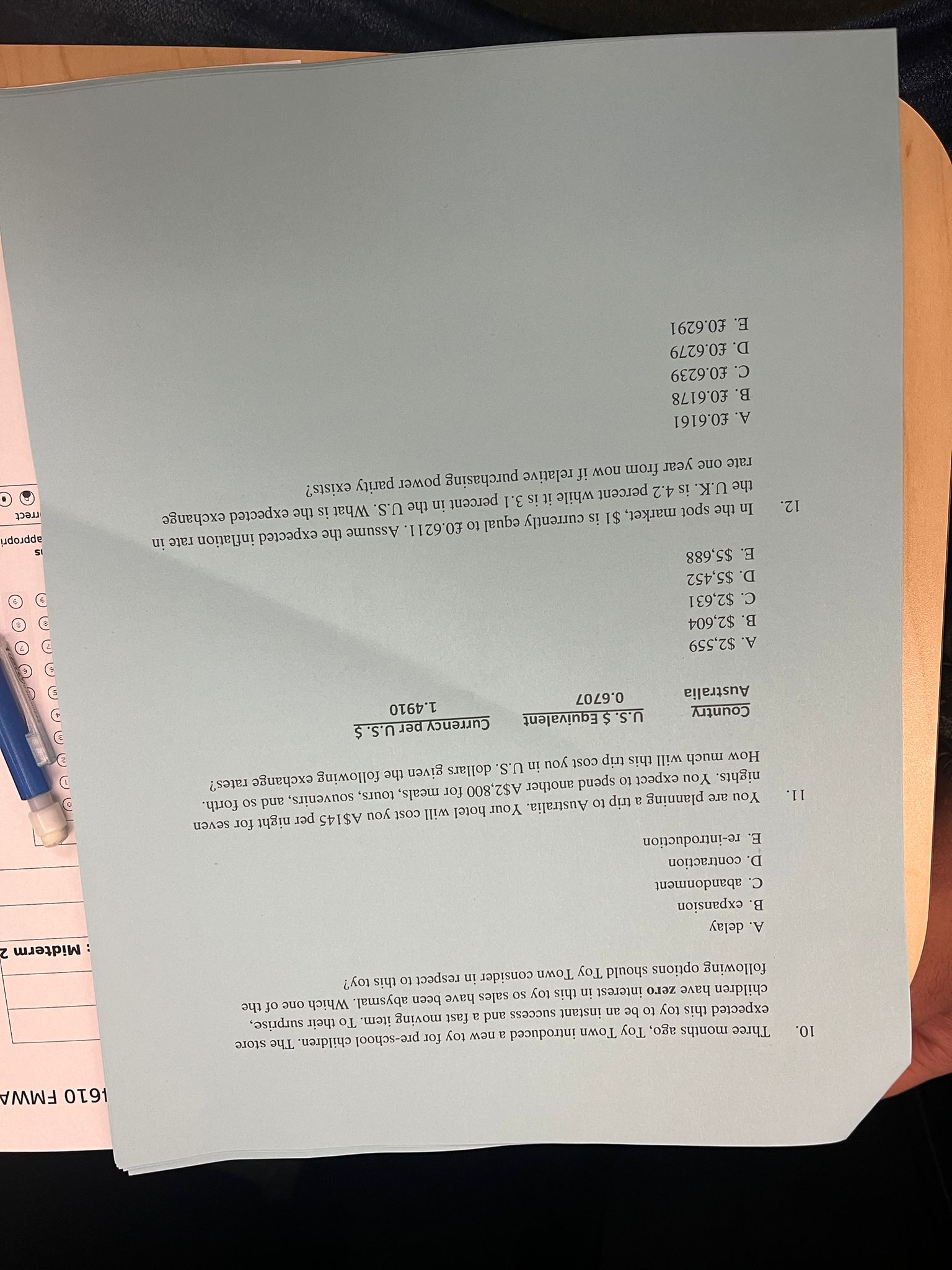

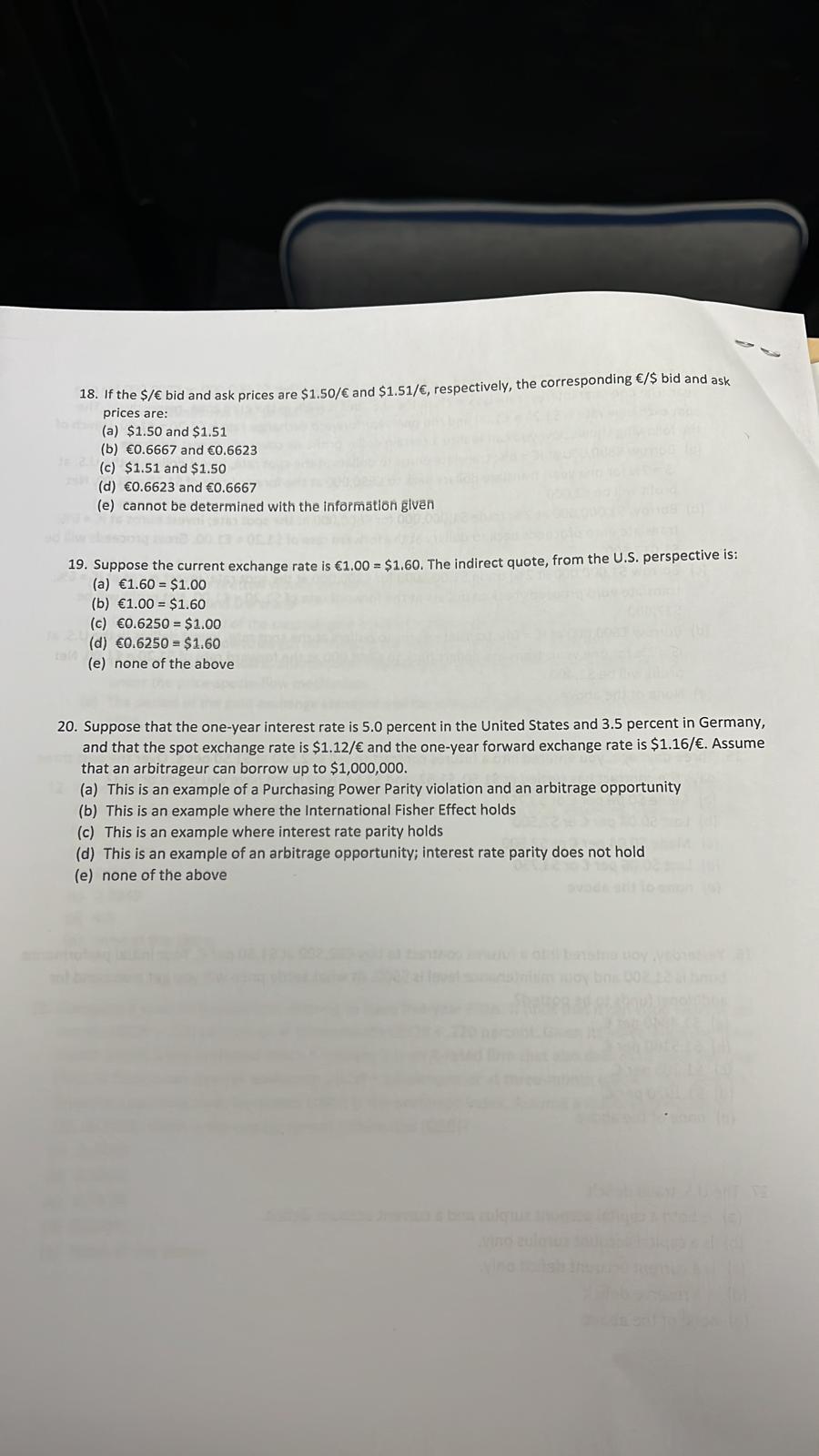

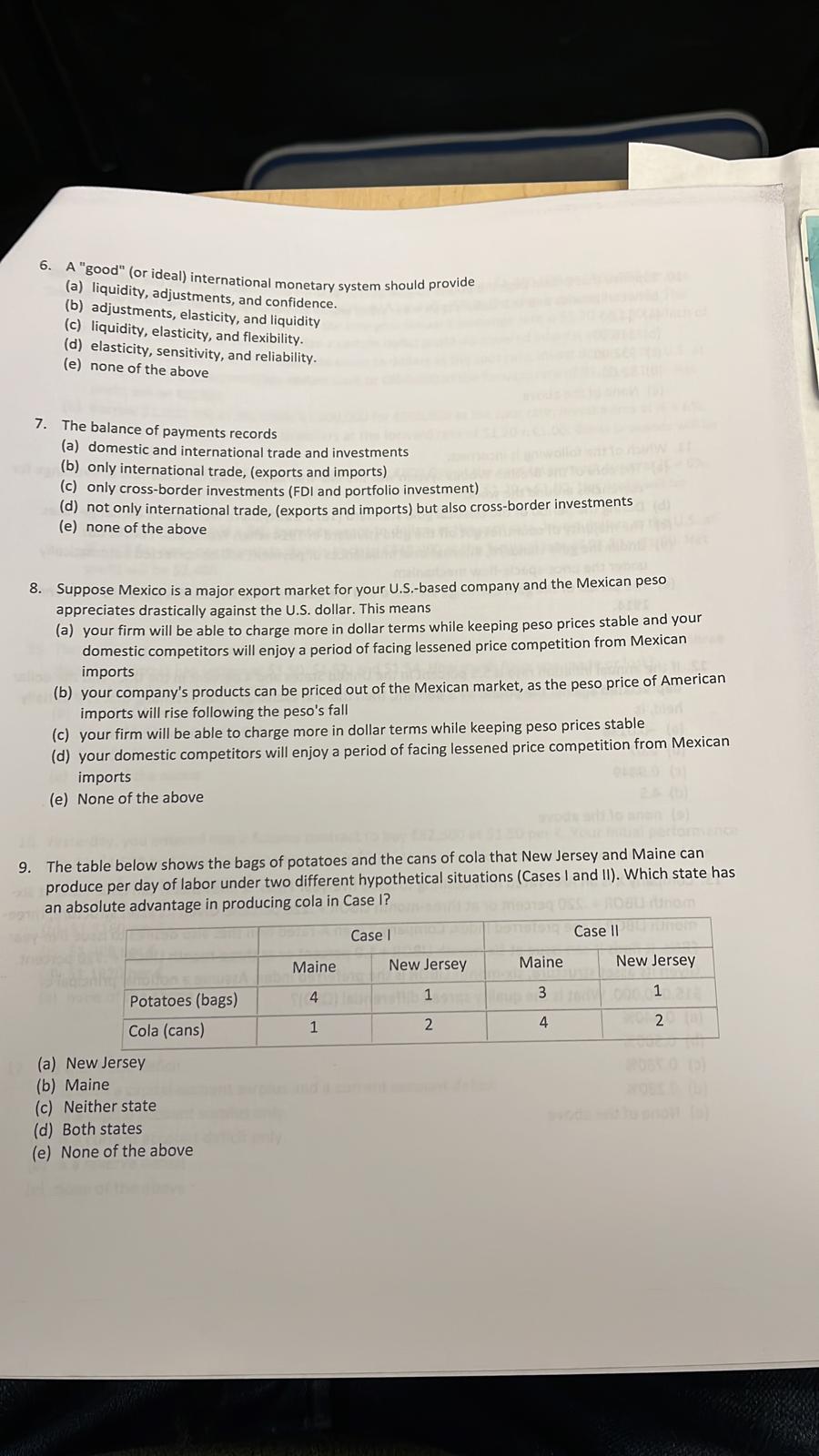

N 4610 Formula Sheet - FIN 4610 Midterm 2 1. Assets = Debt + Equity 2. Let V be the market value of a firm V = D + E, whereas D and E represent market values of debt and equity 12: Mid FV 3. PV = (1+7) 4. FV = PV(1+r) CF 5. Multiple CFs: PV = CF 1 CF 2 CF 3 Itr + ( 1+ r)2 + ( 1 + r)3 + ...+ ( 1 + r ) 6. Effective rate: Tp = (1 + rc) - 1, where re is interest rate per compounding period. 7. PVA = A x PVIFA = Ax (1 + r) 8. FVA = A x FVIFA = A x (1 + r) - 1 1 - 1+9 1 + r 10. PVGA = Ax r - g 11. PVGP = A DIV 1 For stocks, we also can use P = DIV o (1 + g) pro r - g r - g r - g D E 12. RA = D+ERD RD(1 - To) + D+ERE. 13. RE = Rf + B(RM - RJ) where RM is the expected market return and R is the risk-free rate. 14. The following notations are used in international finance formula: PFC and Pus are prices in foreign and US currencies. St is the spot exchange rate at time t (foreignIN 4 4. By definition, which one of the following contracts is marked to the market on a daily basis? A. forward contract B. spot contract C. hedge D. swap 22: E. futures contract 5. Suppose you sell nine September silver futures contracts at the last price of the day as shown in the table below. What will be your profit or loss on this contract if the price turns out to be $12.09 per ounce at expiration? (Hint: Please note that the prices are quoted in cents below.) Futures: Silver - 5,000 troy oz, U.S. cents per troy OZ. OPEN HIGH LOW SETTLE |CHG LIFETIME LIFETIME HIGH LOW July 1163.0 1163.0 1135.5 1140.5 -7.0 1520.0 475.0 Sept 1154.5 1174.5 1137.0 1152.5 -7.0 1518.0 689.3 A. loss of $25,425 B. loss of $7,050 C. loss of $3,025 D. profit of $3,025 E. profit of $25,425 6. You are the buyer for a cereal company and you must buy 80,000 bushels of corn next month. The futures contracts on corn are based on 5,000 bushels and each contract is currently quoted at 415 cents per bushel for delivery next month. If you want to hedge your cost, you should contracts at a cost of per contract. A. buy 12; $2,075 B. buy 16; $20,750 C. buy 16; $2,075,000 D. sell 12; $2,075 E. sell 16; $2,075,00014. An American currency dealer has good credit and can borrow either $1,000,000 or 6800,000 for one year. The one-year interest rate is i$ = 2% in the U.S. and it = 6% in the euro zone, respectively. The spot exchange rate is $1.25 = 1.00 and the one-year forward exchange rate is $1.20 = (1.00. Which of the following shows how you can realize a certain dollar profit via covered interest arbitrage. (a) Borrow E800,000 at it = 6%; translate euros to dollars at the spot rate, invest dollars in the U.S. at i$ = 2% for one year; translate dollars back to E850,000 at the forward rate of $1.20 = (1.00. Net profit will be E2,00 (b) Borrow $1,000,000 at 2%; trade $1,000,000 for E800,000 at the spot rate; invest euros at it = 6%; translate euro proceeds back to dollars at the forward rate of $1.20 = (1.00. Gross proceeds will be $1,017,600 (c) Borrow $1,000,000 at 2%; trade $1,000,000 for E800,000 at the spot rate; invest euros at it = 6%; translate euro proceeds back to dollars at the forward rate of $1.20 = (1.00. Net profit will be $17,600 (d) Borrow E800,000 at it = 6%; translate euros to dollars at the spot rate, invest dollars in the U.S. at i$ = 2% for one year; translate dollars back to E848,000 at the forward rate of $1.20 = (1.00. Net profit will be $2,400 (e) None of the above 15. Three days ago, you entered into a futures contract to sell (62,500 at $1.50 per E. Over the past three days the contract has settled at $1.50, $1.52, and $1.54. How much have you made or lost? (a) Made $0.06 per E or $3,750 (b) Lost $0.04 per E or $2,500 (c) Made $0.04 per E or $2,500 (d) Lost $0.06 per E or $3,750 (e) none of the above 16. Yesterday, you entered into a futures contract to buy (62,500 at $1.50 per E. Your initial performance bond is $1,500 and your maintenance level is $500. At what settle price will you get a demand for additional funds to be posted? (a) $1.4840 per E. (b) $1.5160 per E. (c) $1.208 per E. (d) $1.1920 per E. (e) none of the above 17. The U.S. trade deficit (a) is both a capital account surplus and a current account deficit. (b) is a capital account surplus only (c) is a current account deficit only. (d) is a reserve deficit (e) none of the above10. Suppose that Britain pegs the pound to gold at four pounds per ounce, whereas the exchange rate between pounds and U.S. dollars is $4 = E1. What would an ounce of gold be worth in U.S. dollars? (8) $1.00 (b) $16.00 (c) $32.00 (d) $2.00 (e) None of the above 11. Which of the following is incorrect: (a) The core of the Bretton Woods system was the IMF that determined the fixed rate of exchange for currencies around the world (b) During the period of the classical gold standard (1875-1914) there were stable exchange rates (c) The majority of countries got off the gold standard in 1914 when World War I broke out (d) Under the gold standard, international imbalances of payment will be corrected automatically under the price-specie-flow mechanism (e) The period of the gold exchange standard and the classical gold standard is between 1875 and CF 1914. Un 508 12. If the annual inflation rate is 5.5 percent in the United States and 4 percent in the U.K., and the dollar depreciated against the pound by 3 percent, then the real exchange rate, assuming that PPP initially held, is (a) -0.0198 (b) 0.07 (c) 0.9849 (d) 4.5 (e) none of the above 13. Company X is an AAA-rated firm desiring to issue five-year FRNs. It finds that it can issue FRNs at six- month LIBOR + .220 percent or at three-month LIBOR + .220 percent. Given its asset structure, three- month LIBOR is the preferred index. Company Y is an A-rated firm that also desires to issue five-year FRNs. It finds it can issue at six-month LIBOR + 1.0 percent or at three-month LIBOR + .720 percent. Given its asset structure, six-month LIBOR is the preferred index. Assume a notional principal of $15,000,000. What is the quality spread differential (QSD)? (a) 0.440% (b) 0.500% (c) 0.780% (d) 0.280% (e) None of the abovecurrency per dollar). E[S,] is the expected exchange rate at time t, F is the foreign exchange rate for time t. hus and hec are inflation rates in US and foreign country - FIN 4610 FMWA 15. Absolute PPP: PFC = So X Pus 16. Relative PPP: Es, = Soll + (hFc - hus)]', hus and hus are inflation rates in the US and foreign countries. 17. Interest rate parity: F = So(1 + RFC - Rus) all 2022: Midterm 2 18. Unbiased forward rates: Ft = E(S() 19. Uncovered interest parity: E(St) = So[1 + RFC - Rus] 20. International Fisher effect: Rus - hus = RFC - hpc. Real rates of US and foreign countries need to be the same. 21. The following notations will be used in option pricing: C and P are call and put prices S is the stock price (or underlying asset price) and E is the strike price. t is time to expiration, R is risk-free interest rate. o is the implied standard deviation. 22. Call payoff = max(0, S - E), Put payoff = max(0, E - S) 23. Put call parity: S+P = C+PV(E). Using continuous compounding, S+P = C+Ee-Rt 24. Continuous compounding PV = FVe-Rt and FV = PVeRt 25. Black-Scholes Option Pricing: C = SN(di) - Ee-Rt N(d2), where dj = In(S/ E)+ (R+2/2)t ovt tructions ll in the approp and d2 = d1 - ovt Incorrect 26. Deltas: Call Delta = N(di) Put Delta = N(d1) - 1 27. PCP for balance sheet: Value of assets (S) = value of equity (C) + value of a risky bond ( Ee-Rt-P) 28. Conversion price = Face Value/Conversion Ratio 21. Intervention in the foreign exchange market is the process of (a) a central bank buying or ving or selling its cu ling its currency in order to influence its value. (b) the government of a country prohibiting transactions in one or more currencies. (c) a central bank requiring the commercial banks of that country to trade at a set price level. d) commercial banks in different countries coordinating efforts in order to stabilize one or more currencies. (e) none of the above 2. If you think that the dollar is going to depreciate against the euro, you should (a) sell call options on the euro (b) buy call options on the euro (c) buy call and put options on the euro (d) buy put options on the euro. (e) none of the above 3. Due to the integrated nature of their capital markets, investors in both the United States and the U.K. require the same real interest rate, 3.3 percent, on their lending. There is a consensus in capital markets that the annual inflation rate is likely to be 4.3 percent in the United States and 2.3 percent in the U.K. for the next three years. The spot exchange rate is currently $2.3/E. What is your expected future spot dollar-pound exchange rate in three years from now? (a) $5.6895 (b) $2.4376 (c) $7.7413 Wore (d) $1.9827 (e) None of the above . The objective of corporate governance reform should be what? (a) Strengthen the protection of outside investors from expropriation by managers and controlling insiders (b) Strengthen the protection of a family from expropriation by family members Jones bill inthat (c) Strengthen the protection of outside investors from expropriation by managers (d) Strengthen the protection of outside investors from expropriation by controlling insiders (e) none of the above A multinational firm can be defined as a firm that: (a) has sales affiliates in several countries (b) is incorporated in more than one country (c) invests short-term cash inflows in more than one currency (d) incorporated in one country and has production and sales operations in several other countries (e) None of the above4610 FM\\ 13. Which one of the following acts like an insurance policy if the price of a stock you own suddenly decreases in value? A. sale of a European call option B. sale of an American put option C. purchase of a protective put D. purchase of a protective call E. either the sale or purchase of a put 14. The stock of Edwards Homes, Inc. has a current market value of $23 a share. The 3-month call with a strike price of $20 is selling for $3.80 while the 3-month put with a strike price of $20 is priced at $0.54. What is the continuously compounded risk-free rate of return? A. 4.43 percent B. 4.50 percent C. 4.68 percent D. 5.00 percent E. 5.23 percent 15. A stock is currently selling for $36 a share. The risk-free rate is 3.8 percent and the standard deviation is 27 percent. What is the value of di of a 9-month call option with a strike price of $40? A. -0.21872 B. -0.21179 C. -0.21047 D. -0.20950 E. -0.203562022 16. Frostbite Thermal Wear has a zero coupon bond issue outstanding with a face value of $20,000 that matures in one year. The current market value of the firm's assets is $23,000. The standard deviation of the return on the firm's assets is 52 percent per year. and the annual risk-free rate is 6 percent per year, compounded continuously. What is the market value of the firm's equity based on the Black-Scholes model? (Round your answer to the nearest $100.) A. $6,400 B. $6,700 C. $6,900 8. D. $7,000 E. $7,200 17. Amy is a current shareholder of DJ Industries. She has been given the right to purchase an additional 25 shares of DJ Industries stock at a price of $32 a share if she exercises that right within the next 12 months. What is this security called that Amy has been given? A. convertible bond B. warrant C. straddle D. spread E. put 18. A $1,000 convertible debenture has a conversion price for common stock of $85 per share. The common stock is selling at $92 a share. What is the conversion value of this bond? A. $920.00 B. $923.91 C. $1,000.00 D. $1,082.35 E. $1,092.001. Assume the spot rate on the Canadian dollar is C$0.9872. The risk-free nominal rate in the U.S. is 5.4 percent while it is only 4.2 percent in Canada. Which one of the following four-year forward rates best establishes the approximate interest rate parity condition? A. C$0.9407 B. C$0.9608 C. C$1.0267 D. C$1.0519 E. C$1.0597 2. You are analyzing a project with an initial cost of f48,000. The project is expected to return E1 1,000 the first year, $36,000 the second year and E38,000 the third and final year. There is no salvage value. The current spot rate is 10.6211 per dollar. The nominal return relevant to the project is 12 percent in the U.S. The nominal risk-free rate in the U.S. is 4 percent while it is 5 percent in the U.K. Assume that uncovered interest rate parity exists. What is the net present value of this project in U.S. dollars? (Hint: Please use the home currency approach.) A. $23,611 B. $25,938 C. $26,930 D. $29,639 E. $30,796 3. A trader has just agreed to exchange $2 million U.S. dollars for $1.55 million Euros six months from today. This exchange is an example of a: A. spot trade. B. forward trade C. currency swap. D. floating swap. E. triangle arbitrage.1610 FMWA 10. Three months ago, Toy Town introduced a new toy for pre-school children. The store expected this toy to be an instant success and a fast moving item. To their surprise, children have zero interest in this toy so sales have been abysmal. Which one of the following options should Toy Town consider in respect to this toy? A. delay : Midterm 2 B. expansion C. abandonment D. contraction E. re-introduction 1 1. You are planning a trip to Australia. Your hotel will cost you A$145 per night for seven nights. You expect to spend another A$2,800 for meals, tours, souvenirs, and so forth How much will this trip cost you in U.S. dollars given the following exchange rates? Country U.S. $ Equivalent Currency per U.S. $ Australia 0.6707 1.4910 A. $2,559 B. $2,604 C. $2,631 D. $5,452 E. $5,688 12. In the spot market, $1 is currently equal to f0.6211. Assume the expected inflation rate in IS appropri the U.K. is 4.2 percent while it is 3.1 percent in the U.S. What is the expected exchange rrect rate one year from now if relative purchasing power parity exists? A. 10.6161 B. E0.6178 C. t0.6239 D. 10.6279 E. t0.6291he corresponding {5 bid and 33k 18. lfthe SI bid and ask prices are SLEEVE and $1.51/, respectively, t prices are: is] $1.50 and 51,51 It!) {0.5657 and {0.6523 {c} $1.51 and $1.50 (d) {0.5623 and 0.655? {9} Cannot be determined with the information glven A . ' 's: 19' Suppose the current exchange rate is 1.00 = 51.60. The Indirect quote. from the U.S. perspeCIIVe I {a} 150 = $1.00 lb) 1.00 2 51.60 {C} #316250 = $1.00 [d] 06250 = $1.60 Ea} none cfthe above 20. Suppose that the oneyear interest rate is 5.0 percent in the United States and 3.5 percent in Germany, and that the spot exchange rate is $1.12f and the one-year forward exchange rate is $116,116 Assume that an arbitrageur can borrow up to 51,000,900. {a} This is an example of a Purchasing Power Parity violation and an arbitrage opportunity {b} This is an example where the international Fisher Effect holds (c) This is an example where interest rate parity holds {0'} This is an example of an arbitrage opportunity; interest rate parity does not hold [e] none ofthe above 6. A "good" (or ideal) international monetary system should provide (a) liquidity, adjustments, and confidence. (b) adjustments, elasticity, and liquidity (c) liquidity, elasticity, and flexibility. (d) elasticity, sensitivity, and reliability. (e) none of the above 7. The balance of payments records (a) domestic and international trade and investments (b) only international trade, (exports and imports) (c) only cross-border investments (FDI and portfolio investment) (d) not only international trade, (exports and imports) but also cross-border investments (d) (e) none of the above 8. Suppose Mexico is a major export market for your U.S.-based company and the Mexican peso appreciates drastically against the U.S. dollar. This means (a) your firm will be able to charge more in dollar terms while keeping peso prices stable and your domestic competitors will enjoy a period of facing lessened price competition from Mexican imports (b) your company's products can be priced out of the Mexican market, as the peso price of American imports will rise following the peso's fall (c) your firm will be able to charge more in dollar terms while keeping peso prices stable (d) your domestic competitors will enjoy a period of facing lessened price competition from Mexican imports (e) None of the above 9. The table below shows the bags of potatoes and the cans of cola that New Jersey and Maine can produce per day of labor under two different hypothetical situations (Cases | and II). Which state has an absolute advantage in producing cola in Case I? Road hom Case I Case I1 Maine New Jersey Maine New Jersey Potatoes (bags) 4 1 3 1 Cola (cans) 1 2 4 2 (a) New Jersey (b) Maine (c) Neither state (d) Both states (e) None of the above1610 F 7. Which one of the following is true regarding forward contracts? A. The upfront costs to enter a forward contract can be significant. B. If a buyer of a forward contract earns a $200 profit then the seller will also profit by $200. C. The buyer wins when market prices are less than the forward price. D. The payoff profile for the buyer of a forward contract is an upward sloping linear Midte function. E. If the seller of a forward contract earns a profit then the buyer has neither a profit nor a loss. 8. Murray's can borrow money at a fixed rate of 10.5 percent or a variable rate set at prime plus 2.25 percent. Fred's can borrow money at a variable rate of prime plus 1.5 percent or a fixed rate of 12 percent. Murray's prefers a variable rate and Fred's prefers a fixed rate. Given this information, which one of the following statements is correct? A. After swapping interest rates with Fred's, Murray's may be able to pay prime plus 2 percent. B. Both companies can profit in a swap which will allow Murray's to pay a (variable) prime rate. C. Fred's will end up with a fixed rate of 10 percent. D. Fred's has the best chance of profiting if it does an interest rate swap with Murray's. E. There are no terms under which Murray's and Fred's can swap interest rates. 9. The buyer of an option contract: A. receives the option premium in exchange for an obligation to either buy or sell an rop underlying asset. B. pays an option premium in exchange for a right to buy or sell an underlying asset during a specified period of time. C. pays the strike price at the time the option is purchased and in exchange receives the right to exercise the option at any time during the option period. D. receives the option premium in exchange for guaranteeing the purchase or sale of an underlying asset if called upon to do so. E. pays the option premium in exchange for receiving the strike price at a later date

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!