Question: NAME PART II-PROBLEMS/QUESTIONS In this section, make sure to answer all sub-parts! Problem 1-Interest Rate Forecasting (8 pts) The following are the US Treasury rates

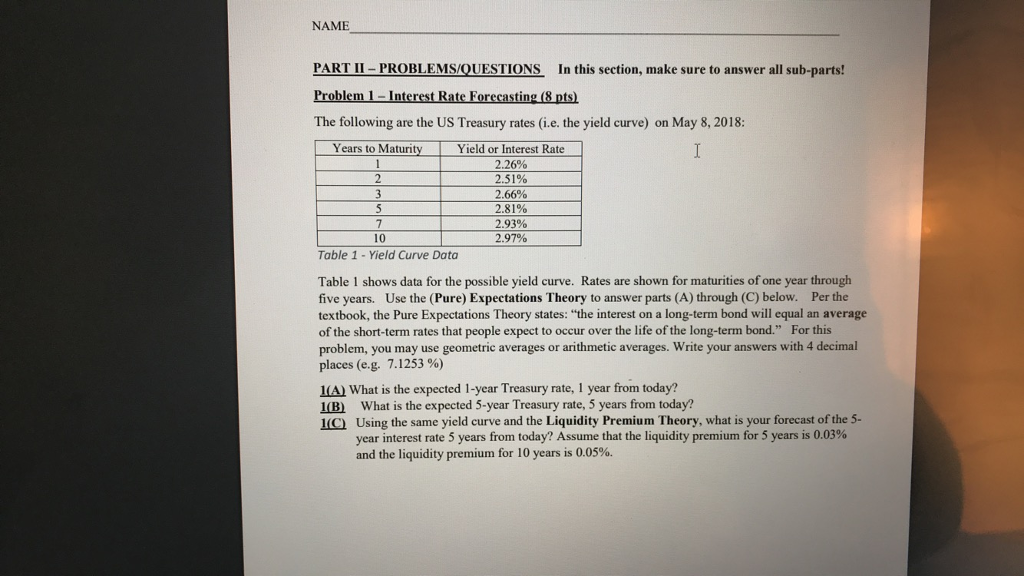

NAME PART II-PROBLEMS/QUESTIONS In this section, make sure to answer all sub-parts! Problem 1-Interest Rate Forecasting (8 pts) The following are the US Treasury rates (i.e. the yield curve) on May 8, 2018: Years to Maturity Yield or Interest Rate 2.26% 2.51% 2.66% 2.81% 2.93% 2.97% 10 Table 1 - Yield Curve Dato Table 1 shows data for the possible yield curve. Rates are shown for maturities of one year through five years. Use the (Pure) Expectations Theory to answer parts (A) through (C) below. Per the textbook, the Pure Expectations Theory states: "the interest on a long-term bond will equal an average of the short-term rates that people expect to occur over the life of the long-term bond." For this problem, you may use geometric averages or arithmetic averages. Write your answers with 4 decimal places (eg 7.1253%) what is the expected 1-year Treasury rate, 1 year from today? 1(B) What is the expected 5-year Treasury rate, 5 years from today? 1Qa Using the same yield curve and the Liquidity Premium Theory, what is your forecast of the 5- year interest rate 5 years from today? Assume that the liquidity premium for 5 years is 0.03% and the liquidity premunn for 10 years is 0.05%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts