Question: nck Illustration 16. B Ltd. is considering whether to set up a division in order to manufacture a new Product A The following statement has

nck

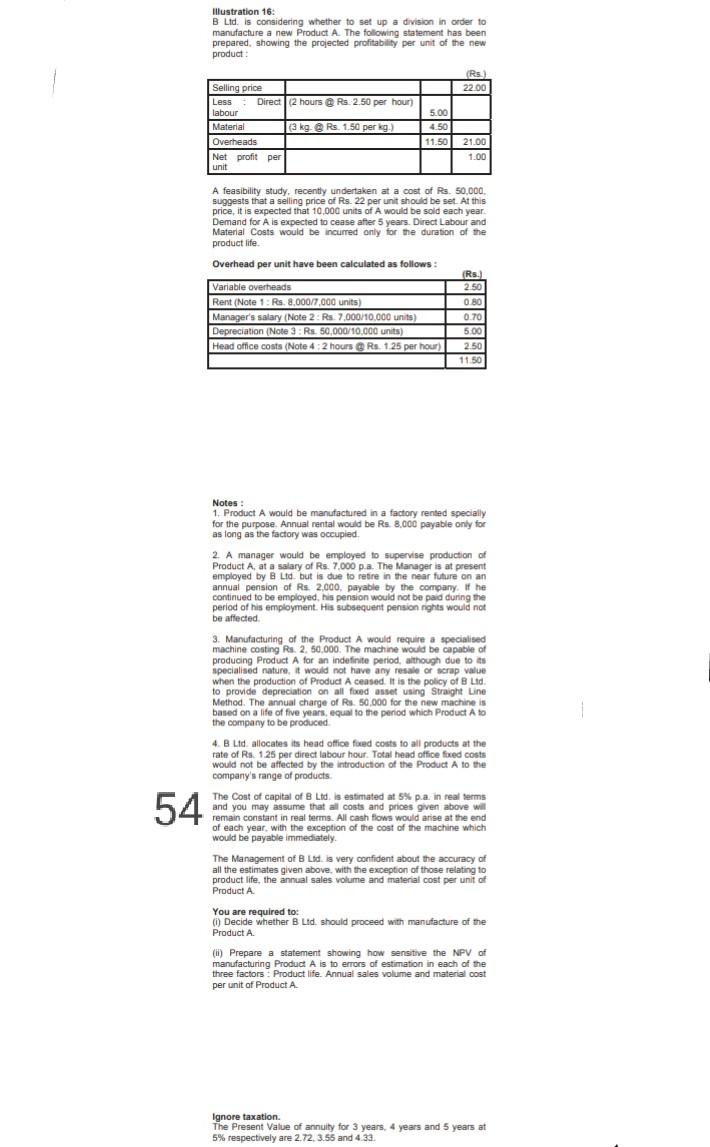

Illustration 16. B Ltd. is considering whether to set up a division in order to manufacture a new Product A The following statement has been prepared, showing the projected profitability per unit of the new product (Rs) 22.00 Selling price Less Direct 2 hours @ Rs. 2.50 per hour labour 5.00 4.50 (3 kg @ Rs. 1.50 per kg. 11.50 Material Overheads Net profit per unit 21.00 1.00 A feasibility study, recently undertaken at a cost of Rs. 50,000 suggests that a selling price of Rs. 22 per unit should be set. At this price, it is expected that 10,000 units of A would be sold each year Demand for A is expected to cease after 5 years. Direct Labour and Material Costs would be incurred only for the duration of the product life Overhead per unit have been calculated as follows: (Rs.) Variable overheads 2.50 Rent (Note 1 : Rs. 8.000/7,000 units) 0.80 Manager's salary (Note 2: Rs. 7,000/10,000 units) 0.70 Depreciation Note 3 : Rs. 50,000/10,000 units) 5.00 Head office costs (Note 4 : 2 hours @ Rs. 1.25 per hour) 250 11.50 Notes 1. Product A would be manufactured in a factory rented specially for the purpose. Annual rental would be Rs. 8.000 payable only for as long as the factory was occupied 2. A manager would be employed to supervise production of Product A, at a salary of Rs. 7,000 p.a. The Manager is at present employed by Ltd, but is due to retire in the near future on an annual pension of Rs. 2,000, payable by the company. It he continued to be employed his pension would not be paid during the period of his employment. His subsequent pension rights would not be affected 3. Manufacturing of the Product A would require a specialised machine costing Rs. 2. 50,000. The machine would be capable of producing Product A for an indefinite period, although due to its specialised nature. It would not have any resale or scrap value when the production of Product A ceased. It is the policy of B Lid. to provide depreciation on all fod asset using Straight Line Method. The annual charge of Rs. 50,000 for the new machine is based on a life of five years, equal to the period which Product A to the company to be produced 4. B Ltd. allocates its head office fixed costs to all products at the rate of Rs 1.25 per direct labour hour. Total head office forced costs would not be affected by the introduction of the Product A to the company's range of products 54 The cost of capital of B Ltd. is estimated at 5% p.a. in real terms and you may assume that all costs and prices given above will remain constant in real terms. All cash flows would arise at the end of each year, with the exception of the cost of the machine which would be payable immediately. The Management of Bad is very confident about the accuracy of all the estimates given above, with the exception of those relating to product life, the annual sales volume and material cost per unit of Product A You are required to: 0) Decide whether B Lid. should proceed with manufacture of the Product A (6) Prepare a statement showing how sensitive the NPV of manufacturing Product A is to errors of estimation in each of the three factors Product life. Annual sales volume and material cost per unit of Product A Ignore taxation. The Present Value of annuity for 3 years. 4 years and 5 years at 5% respectively are 2.72.3.55 and 4.32Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock