Question: need all only otherwise don't touch it Case Study: Target Costing Aparajitha Limited is a leading Refrigerator Company and sells its products across the World.

need all only otherwise don't touch it

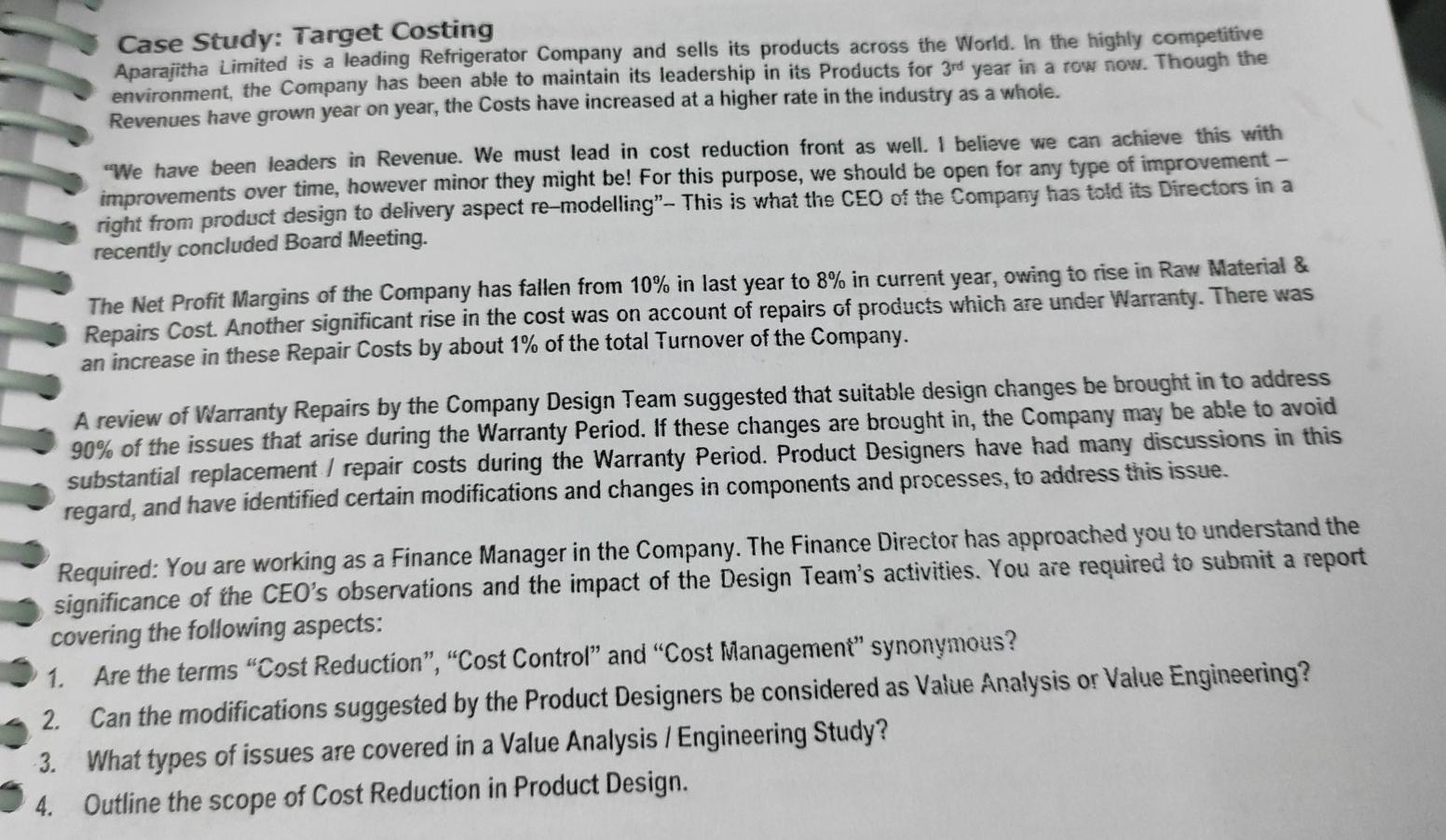

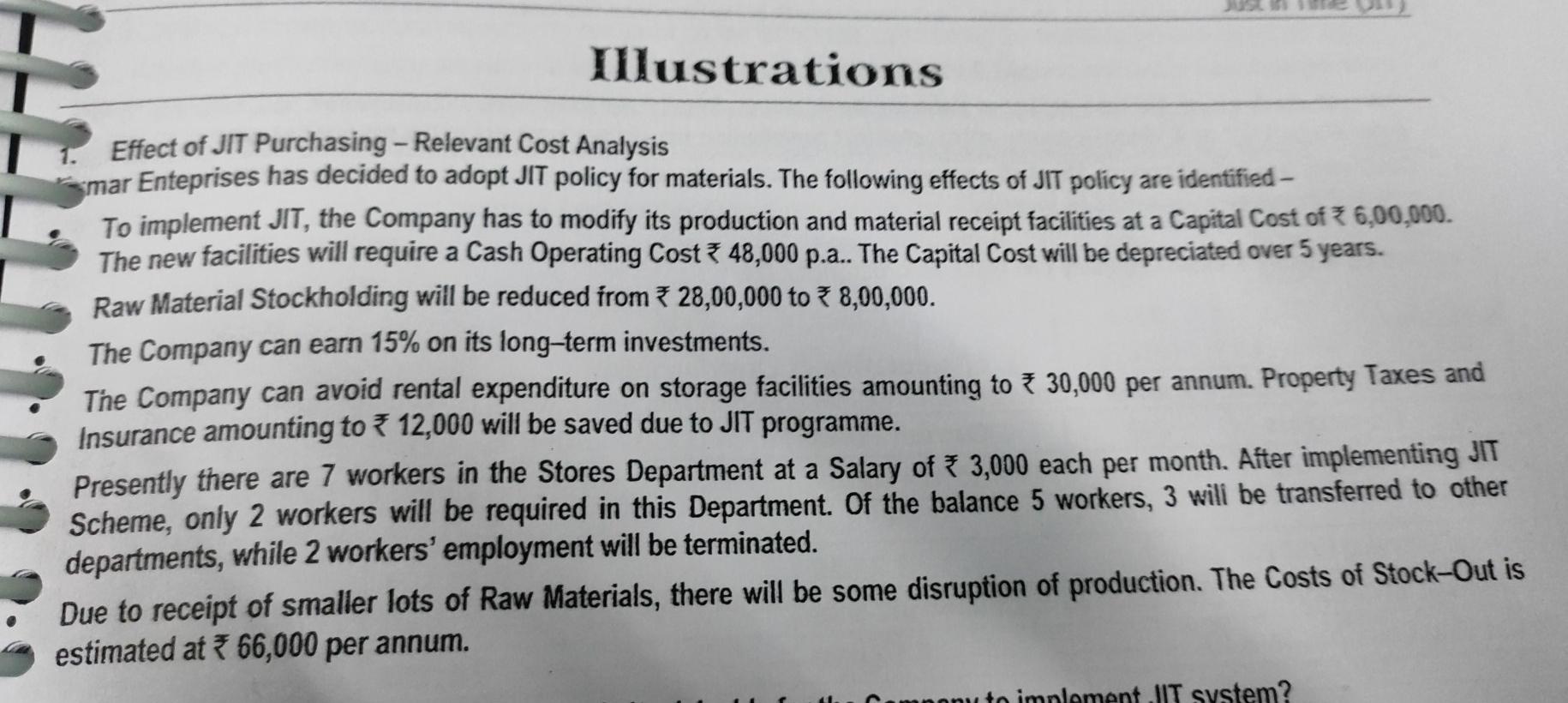

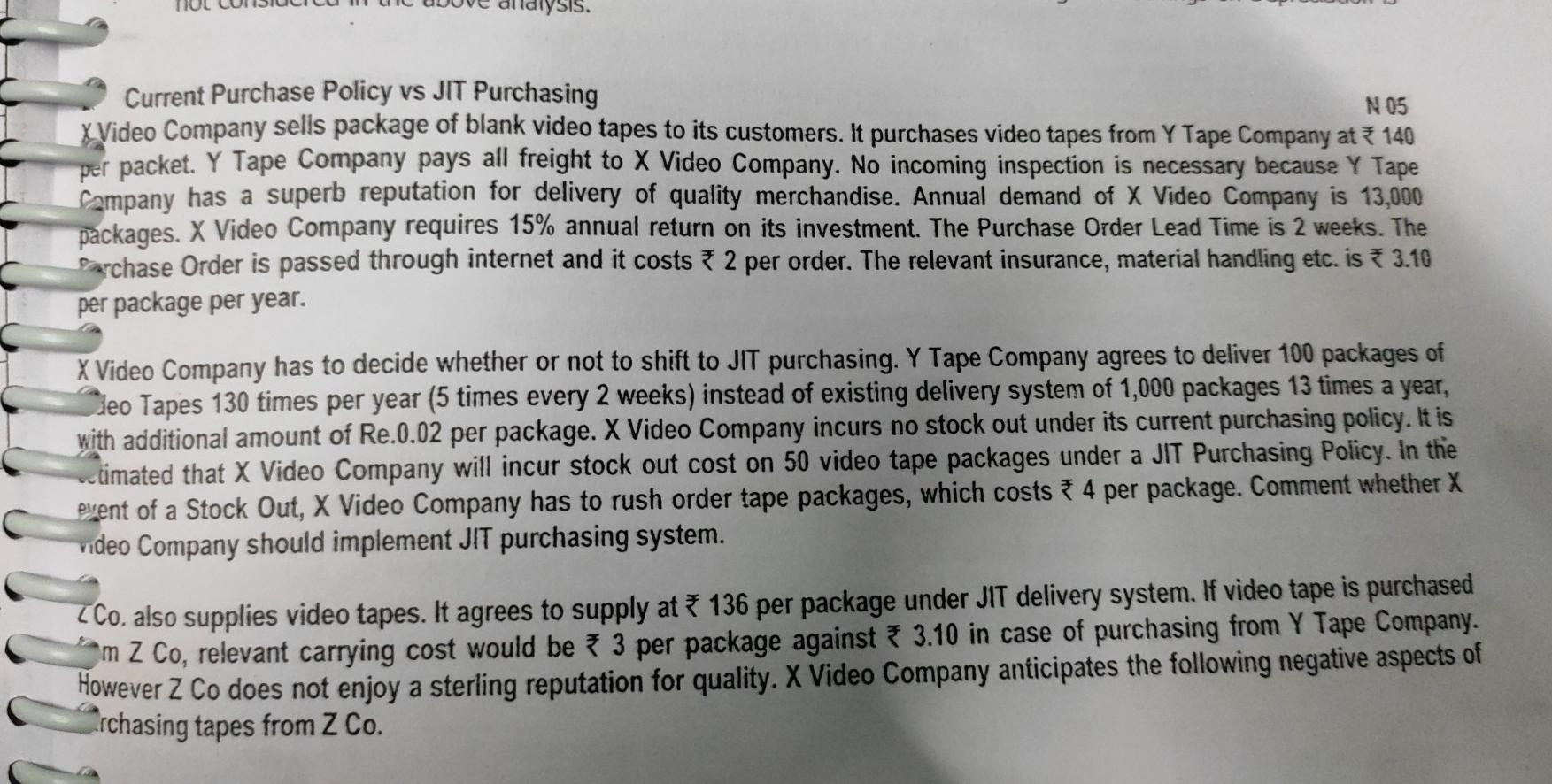

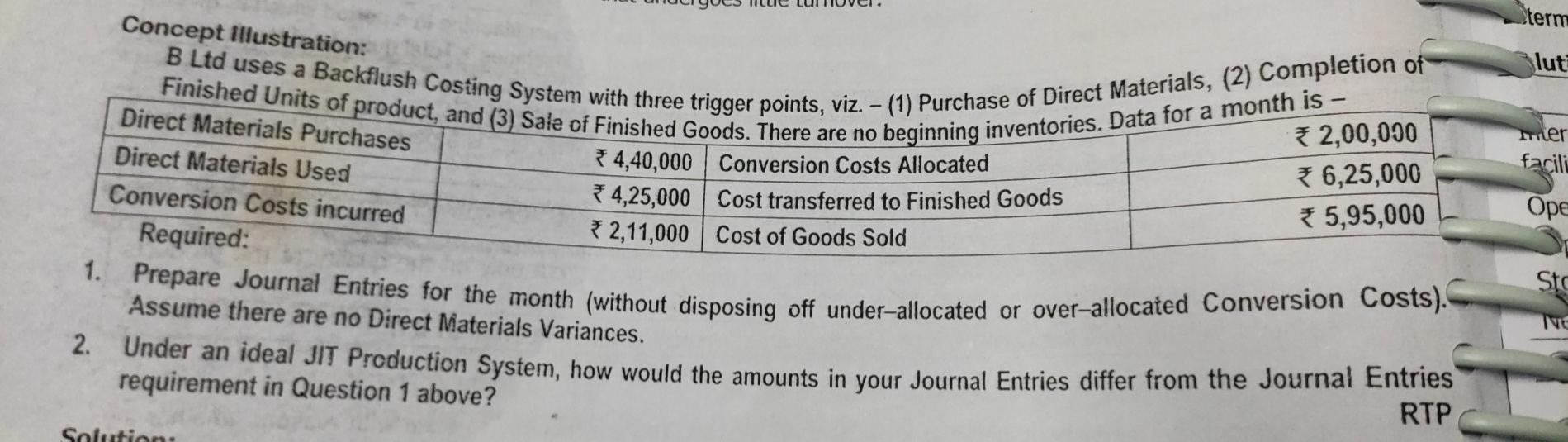

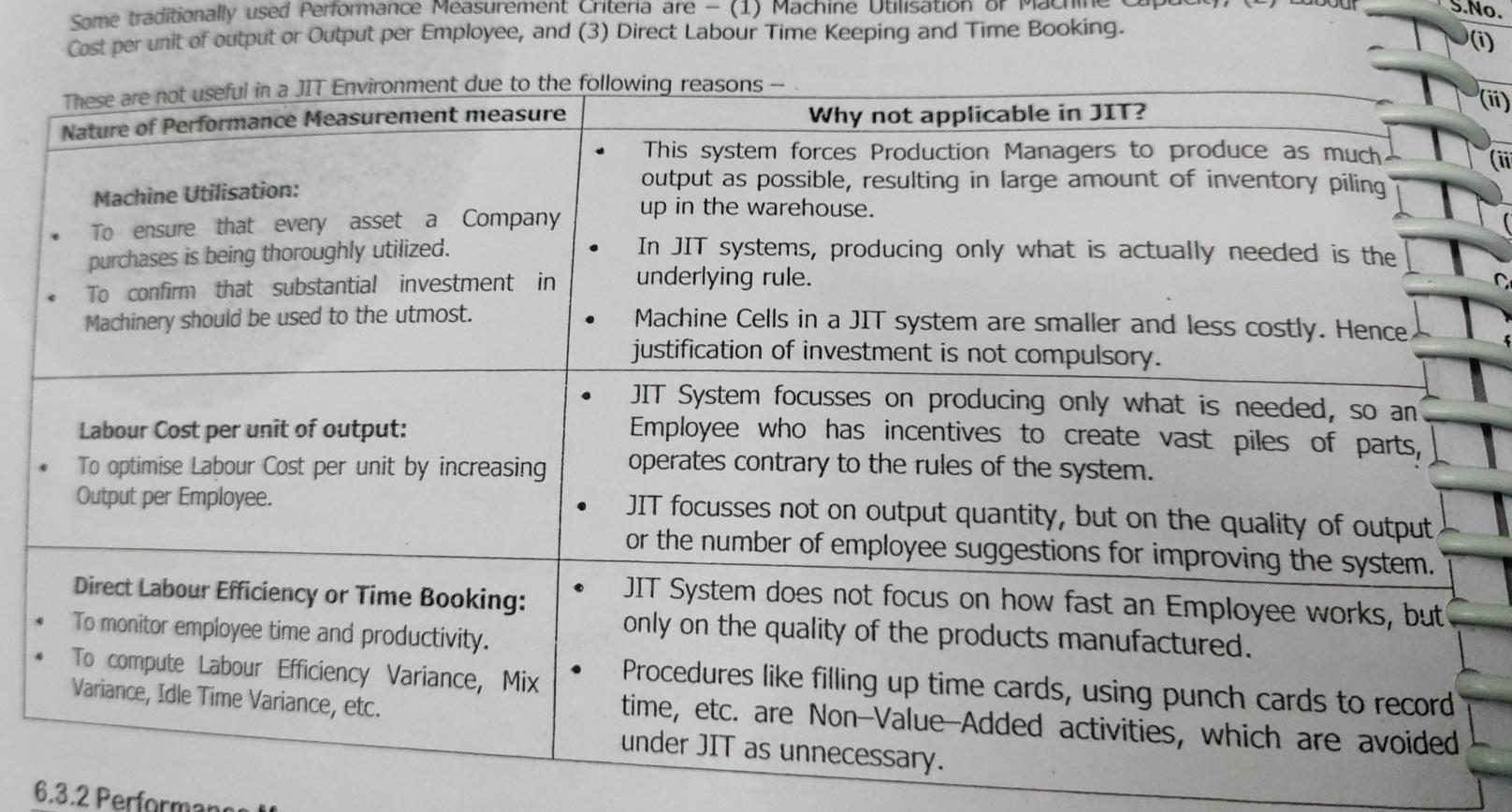

Case Study: Target Costing Aparajitha Limited is a leading Refrigerator Company and sells its products across the World. In the highly competitive environment, the Company has been able to maintain its leadership in its Products for 3rd year in a row now. Though the Revenues have grown year on year, the Costs have increased at a higher rate in the industry as a whole. We have been leaders in Revenue. We must lead in cost reduction front as well. 1 believe we can achieve this with improvements over time, however minor they might be! For this purpose, we should be open for any type of improvement - right from product design to delivery aspect re-modelling- This is what the CEO of the Company has told its Directors in a recently concluded Board Meeting. The Net Profit Margins of the Company has fallen from 10% in last year to 8% in current year, owing to rise in Raw Material & Repairs Cost. Another significant rise in the cost was on account of repairs of products which are under Warranty. There was an increase in these Repair Costs by about 1% of the total Turnover of the Company. A review of Warranty Repairs by the Company Design Team suggested that suitable design changes be brought in to address 90% of the issues that arise during the Warranty Period. If these changes are brought in, the Company may be able to avoid substantial replacement / repair costs during the Warranty period. Product Designers have had many discussions in this regard, and have identified certain modifications and changes in components and processes, to address this issue. Required: You are working as a Finance Manager in the Company. The Finance Director has approached you to understand the significance of the CEO's observations and the impact of the Design Team's activities. You are required to submit a report covering the following aspects: 1. Are the terms Cost Reduction", "Cost Control" and "Cost Management" synonymous? 2. Can the modifications suggested by the Product Designers be considered as Value Analysis or Value Engineering? 3. What types of issues are covered in a Value Analysis / Engineering Study? 4. Outline the scope of Cost Reduction in Product Design. Illustrations Effect of JIT Purchasing - Relevant Cost Analysis smar Enteprises has decided to adopt JIT policy for materials. The following effects of JIT policy are identified - To implement JIT, the Company has to modify its production and material receipt facilities at a Capital Cost of 7 6,00,000. The new facilities will require a Cash Operating Cost 3 48,000 p... The Capital Cost will be depreciated over 5 years. Raw Material Stockholding will be reduced from 328,00,000 to 8,00,000. The Company can earn 15% on its long-term investments. The Company can avoid rental expenditure on storage facilities amounting to 7 30,000 per annum. Property Taxes and Insurance amounting to 12,000 will be saved due to JIT programme. Presently there are 7 workers in the Stores Department at a Salary of * 3,000 each per month. After implementing JIT Scheme, only 2 workers will be required in this Department. Of the balance 5 workers, 3 will be transferred to other departments, while 2 workers' employment will be terminated. Due to receipt of smaller lots of Raw Materials, there will be some disruption of production. The Costs of Stock-Out is estimated at 66,000 per annum. umnonu to implement IT system? alysis. N 05 Current Purchase Policy vs JIT Purchasing X Video Company sells package of blank video tapes to its customers. It purchases video tapes from Y Tape Company at 7 140 per packet. Y Tape Company pays all freight to X Video Company. No incoming inspection is necessary because Y Tape Company has a superb reputation for delivery of quality merchandise. Annual demand of X Video Company is 13,000 packages. X Video Company requires 15% annual return on its investment. The Purchase Order Lead Time is 2 weeks. The Sarchase Order is passed through internet and it costs 2 per order. The relevant insurance, material handling etc. is * 3.10 per package per year. X Video Company has to decide whether or not to shift to JIT purchasing. Y Tape Company agrees to deliver 100 packages of leo Tapes 130 times per year (5 times every 2 weeks) instead of existing delivery system of 1,000 packages 13 times a year, with additional amount of Re.0.02 per package. X Video Company incurs no stock out under its current purchasing policy. It is stimated that X Video Company will incur stock out cost on 50 video tape packages under a JIT Purchasing Policy. In the event of a Stock Out, X Video Company has to rush order tape packages, which costs * 4 per package. Comment whether X video Company should implement JIT purchasing system. Z Co. also supplies video tapes. It agrees to supply at * 136 per package under JIT delivery system. If video tape is purchased am Z Co, relevant carrying cost would be * 3 per package against * 3.10 in case of purchasing from Y Tape Company. However Z Co does not enjoy a sterling reputation for quality. X Video Company anticipates the following negative aspects of rchasing tapes from Z Co. Concept illustration: term lut Direct Materials Purchases Direct Materials Used Conversion Costs incurred Required: Finished Units of product, and (3) Sale of Finished Goods. There are no beginning inventories. Data for a month is - B Ltd uses a Backflush Costing System with three trigger points, viz. - (1) Purchase of Direct Materials, (2) Completion of *2,00,000 *4,40,000 Conversion Costs Allocated 6,25,000 *4,25,000 Cost transferred to Finished Goods 2,11,000 Cost of Goods Sold *5,95,000 her facili Ope 1. Prepare Journal Entries for the month (without disposing off under-allocated or over-allocated Conversion Costs). Sto Assume there are no Direct Materials Variances. TV 2. Under an ideal JIT Production System, how would the amounts in your Journal Entries differ from the Journal Entries requirement in Question 1 above? RTP Solution: Concept Illustration: M Ltd, a Manufacturing Company, is going to implement JIT system. You are required to state with reasons whether the following recommendations are valid or invalid: MS U Introduction of Piece Rate System of payment of wages to workers. fil It has been decided to introduce Kanban Card and Machine Cells together in order to reduce the defective products. Use of highly automated and costly machines to the full capacity. con onorate and maintain single machine so that the work can be done effectively. S.No. Some traditionally used Performance Measurement Criteria are - (1) Machine Utilisation or Cost per unit of output or Output per Employee, and (3) Direct Labour Time Keeping and Time Booking. These are not useful in a JIT Environment due to the following reasons - Nature of Performance Measurement measure Why not applicable in JIT? This system forces Production Managers to produce as much Machine Utilisation: output as possible, resulting in large amount of inventory piling a Company up in the warehouse. To ensure that every asset purchases is being thoroughly utilized. In JIT systems, producing only what is actually needed is the To confirm that substantial investment in underlying rule. Machinery should be used to the utmost. Machine Cells in a JIT system are smaller and less costly. Hence, justification of investment is not compulsory. $ . . Labour Cost per unit of output: To optimise Labour Cost per unit by increasing Output per Employee. . Direct Labour Efficiency or Time Booking: To monitor employee time and productivity. To compute Labour Efficiency Variance, Mix Variance, Idle Time Variance, etc. JIT System focusses on producing only what is needed, so an Employee who has incentives to create vast piles of parts, operates contrary to the rules of the system. JIT focusses not on output quantity, but on the quality of output or the number of employee suggestions for improving the system. JIT System does not focus on how fast an Employee works, but only on the quality of the products manufactured. Procedures like filling up time cards, using punch cards to record time, etc. are Non-Value Added activities, which are avoided under JIT as unnecessary. 6.3.2 Performano 10

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts