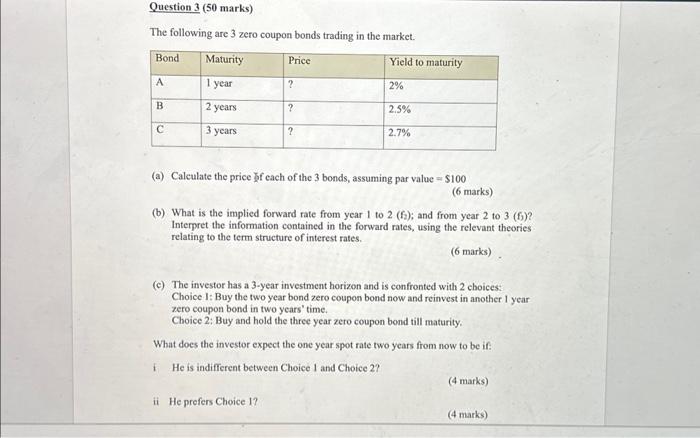

Question: need answer asap The following are 3 zero coupon bonds trading in the market. (a) Caleulate the price $f each of the 3 bonds, assuming

The following are 3 zero coupon bonds trading in the market. (a) Caleulate the price $f each of the 3 bonds, assuming par value =$100 (6 marks) (b) What is the implied forward rate from year 1 to 2 (f); and from year 2 to 3 (f) ? Interpret the information contained in the forward rates, using the relevant theories relating to the term structure of interest rates. (6 marks) (c) The investor has a 3-year investment horizon and is confronted with 2 choices: Choice I: Buy the two year bond zero coupon bond now and reinvest in another 1 year zero coupon bond in two years' time. Choice 2: Buy and hold the three year zero coupon bond till maturity. What does the investor expect the one year spot rate two years from now to be if: I He is indifferent between Choice 1 and Choice 2? (4 marks) ii He prefers Choice 1? (4 marks) (d) Calculate the price of a 2-year bond, Bond D, if the spot rates are as indicated in the table above, and coupon rate is 5% paid once a year. (5 marks) (e) Calculate the YTM of the Bond D. (5 marks) (f) What is the price one year later if interest rates remain unchanged? Suppose that he had bought the bond today. Show that at this price, his return is unchanged. (5 marks) (g) What is the Macaulay duration of Bond D? (5 marks) (h) Estimate what is the new price of Bond D if yield falls by 0.5%. Compare this with the actual price if the yield decline occurs and comment on your results. (5 marks) (i) Will the price change be larger if Bond D is now selling at par instead

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts